Each year the Bureau of Labor Statistics (BLS) updates consumer expenditure data on how Americans collectively spend and earn their money.

These numbers are averages so your personal household budget probably looks different in some ways. Your circumstances — where you live, your standard of living, how much you make, family situation, etc. — often dictate how you spend.

But it can be instructive to look at aggregate spending numbers to see where the most dollars go:

People pay a lot of attention to gas and grocery prices but housing and transportation costs make up 50% of all household spending, on average. Add in food and now we’re close to two-thirds of household spending on necessities.1

It’s the big things that matter when it comes to budgeting. Your daily Starbucks addiction isn’t going to move the needle nearly as much as getting your housing and transportation costs right.

Housing is the big one, of course, but it’s a tough one to pin down on the inflation front. If you locked in a 3% mortgage rate during the pandemic you’ve likely experienced deflation in your housing costs in recent years. Yes insurance and property taxes can rise but that’s a completely different situation than someone trying to buy a house today at much higher prices and mortgage rates.

Renters don’t pay the ancillary costs of home ownership but inflation for the renter class has been a bigger burden in recent years than for homeowners.

Right or wrong, much of the housing inflation this decade has boiled down to luck, both good and bad.

Transportation costs, on the other hand, are more about choice than luck. The all-in costs for transportation — vehicle cost, insurance, maintenance, gas, etc. — were up more than 7% in 2023 after rising more than 12% in 2022.

Much of this has to do with the general rise in prices during this time but some of the transportation costs over time feel like self-imposed inflation.

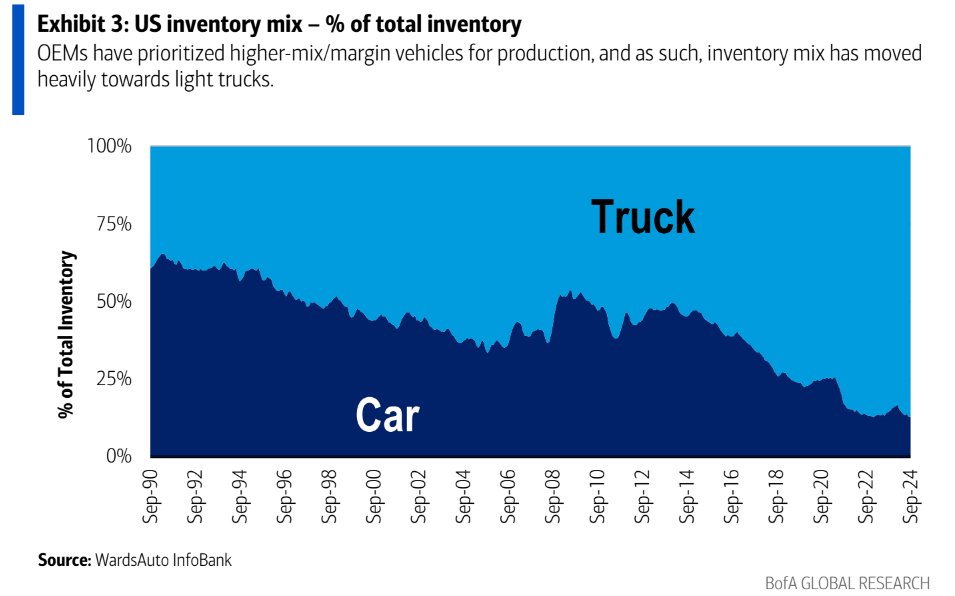

Look at this chart from Bank of America that shows the changing nature of vehicle consumption over time:

Two-thirds of all vehicles on the road in the early-1990s were cars. As recently as 2010, it was basically 50/50. Now we’re looking at 85% of the inventory mix in trucks and SUVs.

We love trucks and SUVs in this country but this shift has to have made a dent in household budgets over time.

Vehicles get better gas milage today than they did in the past but households could save money on gas, insurance premiums and monthly payments if they switched from a truck or SUV back to a sedan.

The crazy thing is our vehicles are getting bigger while our families are getting smaller. The average family size 100 years ago was roughly 4.5 while today it’s more like 2.5. I still don’t understand how people got around in the past when families often had 4-5 kids.

To be fair, I am a hypocrite on this topic. We are a two-SUV family (we also have 3 kids).2

If your budget is stretched, there are really only two places to look for the biggest savings — housing and transportation.

Transportation seems like the simplest fix for most people.

If you need more money, drive something smaller and cheaper.

Further Reading: Is Auto Insurance Becoming a Crisis?

1Not all food spending is out of necessity. Nearly 40% of food spending is classified as “away from home” meaning eating out. Inflation is much higher for eating out than eating at home. Over the past 10 years, food away from home inflation is nearly 50% versus 35% for food at home prices.

2When we’re empty-nesters in ~10 years I can’t wait to drive a sedan again. I miss it.

This content, which contains security-related opinions and/or information, is provided for informational purposes only and should not be relied upon in any manner as professional advice, or an endorsement of any practices, products or services. There can be no guarantees or assurances that the views expressed here will be applicable for any particular facts or circumstances, and should not be relied upon in any manner. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment.

The commentary in this “post” (including any related blog, podcasts, videos, and social media) reflects the personal opinions, viewpoints, and analyses of the Ritholtz Wealth Management employees providing such comments, and should not be regarded the views of Ritholtz Wealth Management LLC. or its respective affiliates or as a description of advisory services provided by Ritholtz Wealth Management or performance returns of any Ritholtz Wealth Management Investments client.

References to any securities or digital assets, or performance data, are for illustrative purposes only and do not constitute an investment recommendation or offer to provide investment advisory services. Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.

The Compound Media, Inc., an affiliate of Ritholtz Wealth Management, receives payment from various entities for advertisements in affiliated podcasts, blogs and emails. Inclusion of such advertisements does not constitute or imply endorsement, sponsorship or recommendation thereof, or any affiliation therewith, by the Content Creator or by Ritholtz Wealth Management or any of its employees. Investments in securities involve the risk of loss. For additional advertisement disclaimers see here: https://www.ritholtzwealth.com/advertising-disclaimers

Interview with: Prof. John Coates, Harvard Professor

As a Professor of Law and Economics at Harvard Law School, as well as former Acting Director for the Division of Corporation Finance for the US Securities and Exchange Commission (SEC), John Coates doesn’t mince his words when it comes to regulating the wildest beasts of modern capitalism. In his latest book, The Problem of 12: When a Few Financial Institutions Control Everything, he explores the origins of a quiet revolution in American finance. ‘Big Four’ index funds such as Vanguard and BlackRock control more than 20 percent of the votes of S&P 500 companies. Private equity firms, the likes of Carlyle and KKR, have amassed trillions of assets while removing from public markets and scrutiny an increasing number of firms. This is the titular ‘problem of 12’: a few financial institutions hold dangerously outsized sway over US politics and finance.

Professor Coates sat with World Finance’s Alex Katsomitros to discuss how we arrived at this crucial juncture and what regulators and policymakers can do about it.

How did index funds and private equity grow so big? Index funds are growing faster than the economy, the stock market and even the companies they own, because they offer a remarkably good product: a low-cost way to achieve diversified investment in the equity, debt and alternative markets. They have a track record of 50 years of outperforming most active managers, even before fees.

Index funds are growing faster than the economy, the stock market and even the companies they own

It is not simply retail investors who benefit from the product, but most large institutional investors, including pension funds and endowments. They also enjoy enormous economies of scale. That allows them to lower fees even more. Today, you can get close to zero costs.

The combination of growth and concentration coming from economies of scale means that the top index funds now own 25 percent or more of all US-listed companies. Private equity funds are also growing faster than the economy and public capital markets and enjoy enormous economies of scale and access to information. They are constantly buying and selling companies, raising funds, exchanging ownership stakes with other investors.

They also run credit funds. So they are responsible for an excess of 25 percent or more of all fee-generating activity for Wall Street. They are the biggest players positioned to harvest information across the entire capital market, and they use that information to time exits, entries and fundraising.

You argue in the book that index funds and private equity have practically become ‘political organisations.’ How did that happen? The politics arises because of concentration. If the industry only consisted of many dispersed firms, like the mutual fund industry 30 years ago, I don’t think they would be significant political players. But the index funds have grown at the largest scale, especially the top three or four. So the problem is that 12 people largely control the outcomes of votes at shareholder meetings for public companies.

When Exxon had a proxy fight a few years ago, the dissident was able to elect directors to the board over the objection of Exxon. They had a very different political agenda, but they were able to do that because the index funds supported them. Currently there is a debate going on over labour policy at Starbucks and other companies. Again, index fund votes are largely determining how those struggles are playing out. So it is the concentration of voting power in a small number of funds that gives them enormous power through the shareholder control process, and with a different result than 20 years ago.

Private equity is different. Their power comes from controlling about 15–20 percent of the entire US economy. About eight or nine percent of US workers work for private equity, even if they don’t know it, because part of the structure of private equity is to make no disclosure. It is difficult to find out who owns what. But they make important choices about how the companies they operate are run, and they have political effects.

Currently in Boston there is a hospital chain that private equity bought out a few years ago. They took on financial risk, and it is probably going to go bankrupt in the next few weeks. That is going to shut down major hospitals in Boston, depriving people of basic healthcare. That is putting a spotlight on the role of private equity not just in that sector, but other parts of the economy too.

You also claim that private equity is not really private anymore. Why is that? Private equity was originally private in the sense that most of the capital that early buyout funds were raising was from a few wealthy individuals. The SEC limited the number of investors, preventing funds from raising money from lots of institutions. They also had ‘look-through’ rules, which meant that if a fund raised money from other funds, it could be a problem. That changed in the 1990s. Now SEC reports show that their principal investors are institutional investors: pension funds, endowments, other funds. So the ultimate economic beneficiaries whose money is being managed are millions of people. A typical private equity fund is no longer managing money just for a few people, but for the public.

It is effectively the same type of capital formation process that goes into a public company, but through a different set of channels, which don’t trigger a requirement to register with the SEC. In fairness, they don’t list the shares of their portfolio companies. So in that sense they are still private, but the ultimate economics are more public.

Should they be regulated like public companies then? I don’t think their structure lends itself to taking public companies’ disclosures and dropping them onto private equity. However, there is a public interest in how they are being run, what risks they are taking, and whether that generates returns that compensate investors. The reason is that US pension funds, especially public pension funds, face relatively light oversight. So if private equity is doing a large part of the investing for those pensions, ultimately US taxpayers are on the hook if the pension funds’ money is not well invested.

Private equity occasionally goes through periods when the risks they take don’t generate returns. When they buy a company, they borrow money and that debt creates financial risk. Some private equity funds generate other kinds of harm through the way they run the kinds of companies they increasingly own. Today, they are active in professional services, healthcare, service businesses regulated in ways that make some disclosure a good idea for the industry.

Control the outcomes of votes at shareholder meetings for public companies

I wish it was as simple as doing the same thing as with public companies, but I don’t think that would be a good model. Most of their operations are portfolio companies that don’t have the capacity to produce quarterly reports or engage with investors. It would be odd to require that kind of detailed reporting when the only exit would happen several years later. So a reporting regime is a good idea, but not the public company regime.

If this is a problem of market concentration, isn’t breaking them up the standard regulatory response? If we are talking about an excessively concentrated product market or service market, antitrust or competition policy has often been the way we respond. But it is not the only way. Take early dominant players in sectors that at the time were high-tech, like electricity and water. Companies that provided what we now call utilities enjoyed massive concentration. We didn’t try to break those up. Sometimes we did, and sometimes there were limits on size.

Another path is to regulate them and allow them to provide benefits because they enjoy economies of scale. This is ultimately the problem. If you break up companies that enjoy efficiencies at great scale, and therefore concentration, you are imposing greater costs on the people who benefit from their services. It will be more costly for 12 index funds to function than four, so they won’t be able to do the same job at the same price.

Isn’t it worth paying that price? Maybe, but another way to go would be to say: ‘okay, we don’t mind that they are so big and concentrated, but we don’t want them to use their power in ways other than their basic utility, which is to invest in a low-cost, diversified way.’ On the regulation side, they have already started to take the first step themselves by being more transparent about how they go about making voting decisions on behalf of other people. They now report quarterly, although they are only required to report annually. I don’t know why they can’t report in real time; the technology is available for that. I would encourage them to go even further.

A typical private equity fund is no longer managing money just for a few people, but for the public

More importantly, they have started, at least in principle, to give their investors the option to pick different policies for them to follow about how to vote. So far, the policies are very similar to each other. Over time for this to work, policies will have to become more varied. There is also a question of whether they will follow the instructions, but this is a work in progress.

The closest analogy is thinking of them as quasi-government agencies. We don’t want to have multiple central banks, that is a contradiction: two central banks are not better than one. What we want is more accountability and transparency.

Would you pin your hopes on a Biden or a Trump administration to address this issue? Any government that doesn’t obey the law, I don’t have any faith in. I may not love the Biden administration all the time on every issue, but they follow the rules. With normal Republican and Democrat candidates, I might have a different view, but Trump has zero commitment to the rule of law. Once you say that, there’s nothing else to say.

We use cookies on our website so it can function correctly. The cookies we use do not store any specific information about you personally and they won’t harm your computer. See our privacy policy for more information. Accept Reject

We did a surprise Thanksgiving podcast drop and had our friend Morgan Housel on the show to talk about the big idea behind his new book, ‘Same As Ever‘. We get into some stuff on the responsibility of a board director, the way investors overweight bad news versus good news, the not-so-aligned incentives of the financial media and so much more. It’s not a long episode but it is as nutritionally dense as anything we’ve ever put out.

Get Morgan’s new book at Amazon here – great holiday gift idea, accessible for literally everyone, whether they invest or just want to have better understanding of the world we live in.

I hope you love it. Have an awesome holiday weekend.

You can listen to the show also, Apple Podcast link here:

Spotify here:

Make sure you’re subscribed to the YouTube channel so you never miss a drop or a live event:

The Compound on YouTube

You can become a Compound Insider – free registration – and be the first to know what’s going on. Get on the list here:

One of the themes of the musical Wicked is brains, heart, and courage. Day 2 of Fortune‘s Most Powerful Women Summit featured all three.

The day wrapped with a stirring performance by Lauren Samuels, an actor and singer playing the role of “Elphaba” in Wicked‘s North American Tour. MPW attendees followed the musical performance with sumptuous fare prepared by all-women chefs.

One of the main themes that emerged from the day is the courage and hard work women have to sustain as they advance into their 50s and all the joy—and unspoken disappointment—that can go with it when age discrimination comes into sharper relief.

Women of all ages are a core part of the workforce, with more older people working than ever before, said Debra Whitman, executive vice president and chief public policy officer at AARP and author of The Second Fifty: Answers to the 7 Big Questions of Midlife and Beyond, at the MPW Summit.

Yet these women face ageism that pushes them out of jobs—income they need as they age due to gender and race-based pay gaps that leave them with less money in the long run, Whitman said.

“So many women have to work longer,” Whitman told Fortune‘s Ani Freedman. “Age discrimination is pretty real and it affects women more. Ageism times sexism equals loss.”

National Women’s Law Center President and CEO Fatima Goss Graves with Midi Health Founder and CEO Joanna Strober and AARP Executive VP and Chief Public Policy Officer at day 2 of MPW 2024.

Kristy Walker for Fortune

That’s why women have a gimlet eye trained on the potential use cases for AI in advancements in areas that have lagged, which are often areas women face.

As Fortune‘s Beth Greenfield reports, Arianna Huffington said, “Sometimes CEOs say, ‘oh, wellbeing is so soft. We need to focus on productivity and business metrics.’ Wellbeing is a productivity multiplier. If your employees are sick or stressed or depleted, do you think they’re going to perform at their best?”

Instacart CEO Fidji Simo and Thrive Global Founder and CEO Arianna Huffington.

Stuart Isett for Fortune

Women are also focused on raising digital-native children and the seductive lure of social media and apps that no generation had as easily accessible.

As Fortune‘s Chloe Berger wrote, Emmy Award-winning documentarian Lauren Greenfield observed the vast difference between how her two sons, ages 14 and 20 grew up and recognized that there was an addiction at play. The apps are meant to be addictive, Greenfield said. Part of the key change that must happen is in the hands of tech and the government monitoring these inventions. In the meantime, it’s about how we treat the children.

“The first thing we go to is kind of blaming the victims,” said Greenfield, noting that this type of outlook “does not work” and “we don’t treat opiate addiction this way.”

Emmy award-winning filmmaker and photographer Lauren Greenfield speaks about her new documentary series, Social Studies, at Fortune’s MPW 2024.

Stuart Isett for Fortune

Just as Greenfield took on her concerns about children and social media, Guild founder Rachel Romer had the courage to keep innovating even after she suffered sudden stroke at age 34, reported Fortune‘s Paolo Confino.

“Every nurse that would come into my room, I would drill them about their career path and ask them lots of questions,” Romer said during her first public appearance since her stroke. “Some nurses started to get weary when they would come in and they would say, ‘I heard you interview every nurse.’ And I would say, ‘yes, I do.’”

Rachel Romer, Co-founder and Executive Chair on Leave, Guild and Bijal Shah, Chief Executive Officer, Guild.

Kristy Walker for Fortune

And sometimes, you need all three—brains, heart, and courage. Trailblazing Ellevest founder Sallie Krawcheck said she has always had a growth mindset—if there is something that she doesn’t know, she’ll learn it, Confino wrote for Fortune. “In fact, I’m having my most fun when I’m a little bit out over my skis,” she said at the summit.

Yet another sentiment that she chooses to remember in her everyday life is that “nobody boos a nobody.” Throughout her career and various leadership roles, Krawcheck says she has continuously received criticism and dealt with haters. But she wears the negativity like a badge of honor, saying you have to succeed despite the hatred because “pressure is a privilege.”

Priscilla Almodovar and Sallie Krawcheck on mainstage at MPW 2024.

Kristy Walker for Fortune

Recommended newsletter The Broadsheet: Covers the trends and issues impacting women in and out of the workplace and the women transforming the future of business.

Sign up here.

TD Bank CEO Bharat Masrani to Retire After $3 Billion Money Laundering Fine

TD Bank hit with $3 billion penalties for anti-money laundering (AML) compliance violations, the largest ever for this type of infraction. As a result, TD bank’s longtime CEO, Bharat Masrani, has announced plans to retire by April 2025. So what went wrong? Well TD let drug cartels launder more than $670 million through the bank between 2018 and 2024. Masrani’s exit reflects the bank’s bigger issues with reputation, compliance, and any hopes at further U.S. expansion.

Bharat Masrani, TD Bank’s CEO for 10+ years, has accepted full responsibility for the bank’s AML failures that happened under his direction. “I accept full responsibility for the anti-money laundering issues we face, which occurred during my tenure as CEO,” Masrani said in a statement. He’s set to retire from his role in April 2025 and is transitioning.

$3 billion historic fine for money laundering failure is the highest in U.S. banking history, and is broken down into $1.3 billion to The Treasury Department’s Financial Crimes Enforcement Network, and another $1.8 billion to the U.S. Department of Justice.

See: TD Bank’s Money-Laundering and Bribery Scandal

As part of a planned leadership transfer, Masrani will be replaced by Raymond Chun, a former senior executive in TD Bank’s Canadian personal banking sector who hasn’t been directly involved in TD’s U.S. business nor connected with any AML concerns . In November 2024, he will assume the role of Chief Operating Officer, and by April 2025, he will assume the role of CEO.

The money laundering investigation has forced TD bank to stall its U.S. expansion plans and cancel its agreement to acquire Tennessee-based First Horizon Corp. TD also now faces restrictions in the U.S. that limit its business growth.

OSFI Statement on TD Bank

The Superintendent of Financial Institutions, Peter Routledge, issued a statement recognizing the seriousness of TD Bank’s anti-money laundering infractions as exposed by U.S. authorities. He underlined the substantial risks posed by TD Bank’s shortcomings and urged prompt action to resolve them while emphasizing the need for good management and compliance procedures.

Why It Matters

TD Bank will need to rebuilt trust with both regulators and consumers which will slow if not hamper it’s growth and reputation while competing in the highly competitive U.S. markets, under new leadership.

The National Crowdfunding & Fintech Association (NCFA Canada) is a financial innovation ecosystem that provides education, market intelligence, industry stewardship, networking and funding opportunities and services to thousands of community members and works closely with industry, government, partners and affiliates to create a vibrant and innovative fintech and funding industry in Canada. Decentralized and distributed, NCFA is engaged with global stakeholders and helps incubate projects and investment in fintech, alternative finance, crowdfunding, peer-to-peer finance, payments, digital assets and tokens, artificial intelligence, blockchain, cryptocurrency, regtech, and insurtech sectors. Join Canada’s Fintech & Funding Community today FREE! Or become a contributing member and get perks. For more information, please visit: www.ncfacanada.org

EPS of $1.49 beats by $0.08 | Revenue of $3.07B (-3.02% Y/Y) beats by $55.40M

This article was written by

Seeking Alpha’s transcripts team is responsible for the development of all of our transcript-related projects. We currently publish thousands of quarterly earnings calls per quarter on our site and are continuing to grow and expand our coverage. The purpose of this profile is to allow us to share with our readers new transcript-related developments. Thanks, SA Transcripts Team

You might be considering an apartment in Seattle or a house in San Francisco, as both cities share many similarities, from thriving tech industries to a love for outdoor recreation. San Francisco offers a more fast-paced, cosmopolitan lifestyle with its iconic landmarks, while Seattle provides a more laid-back atmosphere, surrounded by stunning natural beauty. Whether you’re drawn to the scenic hills of San Francisco or the waterfront views of Seattle, choosing the right city is an important decision.

From real estate prices and job prospects to cost of living and cultural experiences, there’s much to evaluate. In this Redfin article, we’ll break down the key differences to help you decide which city is the best fit for your lifestyle and career goals.

Housing in San Francisco vs Seattle

Housing in San Francisco

San Francisco’s housing market is known for its high prices and competitive market. From luxury condos in SoMa to historic Victorian homes in the Mission, the city offers a range of urban living options. Space is limited, especially in central areas, and prices reflect the high demand for real estate. San Francisco’s iconic neighborhoods are highly sought after, making it one of the most expensive cities in the U.S. for both buyers and renters.

Housing in Seattle

Seattle’s housing market, while still expensive, offers more affordability compared to San Francisco. Buyers can choose from waterfront condos in neighborhoods like Belltown to charming single-family homes in areas like Queen Anne or Ballard. Seattle’s real estate market is competitive, particularly in tech-driven Seattle neighborhoods, but still provides more space and slightly lower prices than San Francisco.

Median home cost: The median home sale price in Seattle is around $845,000, offering more value compared to San Francisco, especially in suburban areas.

Average rental cost: Renting an apartment in Seattle averages around $2,311 per month, with higher prices in neighborhoods like Capitol Hill and lower prices in surrounding areas.

Cost of living in San Francisco vs Seattle

The overall cost of living in San Francisco is about 14% higher than in Seattle, with differences in housing, utilities, and lifestyle costs contributing to the gap.

1. Utilities

Utilities in San Francisco are around 31% higher than in Seattle. San Francisco’s older infrastructure and its hilly terrain lead to increased energy costs, especially for heating and cooling. Meanwhile, Seattle’s temperate climate and more energy-efficient infrastructure help keep utility bills lower.

2. Groceries

Groceries in San Francisco are roughly 7% more expensive than in Seattle. Both cities rely heavily on imported goods, but Seattle’s proximity to local agricultural regions in Washington helps to keep grocery prices more affordable, while San Francisco’s distance from agricultural hubs contributes to slightly higher costs.

3. Transportation

Transportation costs in San Francisco are about 7% higher than in Seattle. San Francisco’s BART and Muni systems, while extensive, can be expensive, and the cost of parking is notably higher. Seattle, although still expanding its public transit system, offers more affordable options, making commuting less costly.

4. Healthcare

Healthcare costs in San Francisco are approximately 8% lower than in Seattle. While San Francisco has a larger population and higher demand for specialized medical services, Seattle’s healthcare system tends to be more expensive, likely due to higher service costs and a different pricing structure.

5. Lifestyle

Lifestyle expenses in San Francisco are around 2% higher than in Seattle. San Francisco’s global status and high living costs drive up prices for dining, entertainment, and cultural experiences, while Seattle offers similar amenities at a more accessible price point.

San Francisco vs Seattle in size and population: A tale of two West Coast cities

San Francisco and Seattle are iconic West Coast cities, but they differ greatly in how they utilize space. San Francisco covers just 47 square miles with a population of about 874,000, resulting in a highly dense, fast-paced environment defined by steep hills and vertical living. In contrast, Seattle spans 142 square miles with a population of over 737,000, offering a more spread-out feel while maintaining an urban atmosphere, especially around its waterfront and downtown areas. San Francisco’s compact layout drives its vibrant, bustling pace, while Seattle’s larger area and integration of parks and nature create a more balanced blend of urban living and open space.

Weather and climate in San Francisco vs Seattle

San Francisco’s climate and Seattle’s climate both benefit from mild, temperate seasons, though San Francisco enjoys more sunshine and drier summers due to its Mediterranean climate. San Francisco experiences cool, foggy mornings in the summer and wet winters, while Seattle is known for its frequent rainfall throughout the year, especially in the fall and winter. Seattle’s summers are pleasant and dry, offering ideal conditions for outdoor activities. Both cities avoid extreme weather, but San Francisco faces earthquake risks due to the San Andreas Fault, while Seattle experiences occasional windstorms and heavy rain.

The job market in San Francisco vs Seattle

San Francisco: A global leader in tech and innovation

San Francisco’s job market is dominated by the tech industry, with Silicon Valley driving the city’s robust economy. With an employment rate of around 66% and a median household income of $127,000, San Francisco offers high earning potential, particularly in tech. The average hourly wage is $46.86, reflecting the city’s expensive cost of living. Major companies like Salesforce, Uber, and Google lead the way in job creation, making San Francisco a global hub for innovation and startups. Other industries, such as healthcare, finance, and education, also offer solid job prospects in the Bay Area.

Seattle: A thriving tech and aerospace hub

Seattle’s economy is also tech-driven, with major employers like Amazon and Microsoft anchoring the job market. The employment rate in Seattle is around 72%, with a median household income of $121,000. The average hourly wage is $41.60, which, while lower than San Francisco, is competitive given Seattle’s lower cost of living. In addition to tech, Seattle is a major player in the aerospace industry, with Boeing as a key employer. The healthcare and biotech sectors are also expanding, with companies like Providence Health and Fred Hutchinson Cancer Research Center contributing to job growth.

Transportation in San Francisco vs Seattle

San Francisco: Dense and transit-oriented

San Francisco boasts an extensive public transportation network, including Muni buses, light rail, and the BART system, which connects the city to the broader Bay Area. The city’s compact layout makes it highly walkable, though steep hills present challenges for some. Biking is popular, with numerous bike lanes and the Ford GoBike program making cycling easier. Driving in San Francisco is difficult due to congestion and limited parking, which makes public transit a favored option for many residents.

Seattle: Expanding transit with bike-friendly routes

Seattle’s transportation system is centered around buses, light rail (Link), and ferries, providing residents with multiple ways to navigate the city and surrounding areas. The city’s bike-friendly infrastructure is growing, with more protected bike lanes and the LimeBike program. Driving is more feasible in Seattle compared to San Francisco, though traffic congestion can be significant during rush hours. The city’s walkability is highest in downtown areas, but the spread-out nature of some neighborhoods makes cars or public transit necessary.

Travel in and out of San Francisco vs Seattle

Both cities are major West Coast travel hubs, with Seattle offering more connections to Alaska and Canada, while San Francisco has stronger international links.

San Francisco: San Francisco International Airport (SFO), BART, Caltrain, Amtrak, ferries, Greyhound, and Megabus.

Seattle: Seattle-Tacoma International Airport (SEA), Link light rail, Amtrak, ferries, Greyhound, and Megabus.

Lifestyle and things to do in San Francisco vs Seattle

A day in the life of a San Franciscan

Life in San Francisco is fast-paced and dynamic, with each neighborhood offering a unique experience. A typical day might begin with a coffee from a local café in the Mission District, followed by a walk to work or a commute via BART. Weekends are for exploring the city’s iconic landmarks, enjoying the vibrant food scene, or hiking in nearby areas like Marin Headlands. For outdoor enthusiasts, a bike ride across the Golden Gate Bridge or a stroll through Golden Gate Park is a favorite pastime.

Top things to do in San Francisco:

Google Street View of Alcatraz Island

San Francisco parks and green gems:

Google Street View of Lands End Trail

San Francisco tourist attractions:

Golden Gate Bridge

Alcatraz Island

Fisherman’s Wharf

Coit Tower

Chinatown

A day in the life of a Seattleite

Living in Seattle offers a mix of urban living and access to nature. A day might start with a cup of coffee from a local roastery before hopping on the Link light rail or biking to work. Weekends are spent exploring the city’s diverse neighborhoods, hiking in nearby mountains, or taking a ferry to the San Juan Islands. Seattle’s music scene, fresh seafood, and outdoor lifestyle draw residents and visitors alike, making it a city for both culture and nature lovers.

Top things to do in Seattle:

Google Street View of the Space Needle

Seattle parks and green gems:

Google Street View of Discovery Park

Seattle tourist attractions:

Space Needle

Chihuly Garden and Glass

Seattle Art Museum

Pike Place Market

Ballard Locks

Food and culture in San Francisco vs Seattle

San Francisco: A foodie’s paradise with global flavors

San Francisco’s food scene is legendary for its innovation and diverse offerings, from fresh seafood at Fisherman’s Wharf to fusion cuisine in the Mission District. The city’s access to fresh, local ingredients from nearby farms makes it a haven for farm-to-table dining. Signature dishes like sourdough bread, Dungeness crab, and Mission-style burritos are a must-try, while the city’s Michelin-starred restaurants continue to push culinary boundaries. San Francisco’s cultural landscape is equally vibrant, with renowned institutions like the San Francisco Symphony and the de Young Museum contributing to its rich arts scene. Annual events such as the Folsom Street Fair and Outside Lands Music Festival showcase the city’s eclectic spirit.

Seattle: Coffee, seafood, and a thriving arts scene

Seattle’s food culture is a reflection of its Pacific Northwest roots, with a focus on fresh seafood, coffee, and innovative cuisine. Pike Place Market remains the heart of the city’s culinary scene, offering everything from fresh fish to artisanal cheeses and local produce. Signature dishes include salmon, oysters, and Dungeness crab, while Seattle’s coffee culture, anchored by iconic brands like Starbucks and an array of independent roasters, is world-famous. Beyond food, Seattle is a cultural hub, home to a thriving music scene, particularly grunge, and notable institutions like the Seattle Art Museum and the Museum of Pop Culture (MoPOP). Events like Bumbershoot and the Seattle International Film Festival highlight the city’s artistic diversity.

Sports scene in San Francisco vs Seattle

San Francisco: A city of champions

San Francisco’s sports scene is home to several championship-winning teams across major professional leagues. The San Francisco Giants have a loyal following in baseball, with Oracle Park offering picturesque views of the Bay during games. The Golden State Warriors, playing just across the Bay, have brought numerous NBA titles home in recent years, making basketball a central part of the city’s sports culture. The San Francisco 49ers, one of the NFL’s most successful franchises, play just outside the city in Santa Clara, continuing to draw huge crowds.

Seattle: Passionate fans and iconic teams

Seattle’s sports scene thrives on the passion of its fans. The Seattle Seahawks enjoy one of the loudest fan bases in the NFL, with games at Lumen Field known for their electric atmosphere. Soccer also has a strong presence, with the Seattle Sounders FC drawing large crowds to the same venue. Baseball fans flock to T-Mobile Park to watch the Seattle Mariners, while the Seattle Kraken have quickly established a devoted following in the NHL. With its mix of professional teams and die-hard fans, Seattle’s sports culture is a central part of the city’s identity.

Conference organized by University of Antwerp, Harvard Law School and ECGI on 30 May

Short-termist behavior by corporations is often seen as a large societal problem. For example, Joe Biden wrote in a 2016 op-ed for the Wall Street Journal: “Short-termism […] is one of the greatest threats to America’s enduring prosperity”.

However, the debate on short-termism has so far largely focused on possible short-termism in the US and the UK). Short-termism in European corporate governance has received much less attention. A notable exception is the 2020 EY study for the European Commission on “directors’ duties and sustainable corporate governance. This study is generally regarded as heavily flawed, however.

For this reason, the University of Antwerp, Harvard Law School and the European Corporate Governance Institute (ECGI) have decided to organize a conference on “short-termism in European corporate governance” on 30 May in Antwerp. We believe that it is important to study short-termism in (continental) Europe, because corporate governance in continental Europe differs in important respects from corporate governance in the US and the UK, with potentially profound implications for the short-termism debate.

Controlling shareholders in Europe

A first important difference is that corporations in continental European countries more often have a controlling shareholder than corporations in the US and the UK. For example, according to one paper, the percentage of shares held by the largest shareholder in the corporation is much higher in France (46.4%), Germany (45.3%), Belgium (38.6%) and the Netherlands (34.6%), than in the US (21.4%) and the UK (19.5%).

This is relevant, because controlling can have an important impact on short-termism, as I argue in a recent working paper. If corporate short-termism is caused by short-termist institutional investors pressuring managers for short-term results, controlling shareholders will block the transmission of this short-termism. In addition, if short-termist managers are causing corporate short-termism, controlling shareholders have the incentives and the power to monitor these short-termist managers, and cause them to be more long-term oriented.

Whether controlling shareholders have a positive or negative impact on a corporation’s long-term orientation will depend on the circumstances, and particularly on the type of controlling shareholders. On the one hand, controlling shareholders have stronger incentives to think in the long term than other shareholders, due to the size and illiquidity of their participation, which exposes them to a larger extent to the long-term cash flows of the corporation. On the other hand, controlling shareholders may also enjoy private benefits of control. Because some private benefits of control are not easily transferred, controlling shareholders may be “locked in” and forced to think of the long-term future of the corporation. However, private benefits of control may also incentivize controlling shareholders to act in a short-termist manner. For example, a family controlling shareholder may prioritize its short-term liquidity needs over the long-term investments needed by the corporation.

Executive compensation structure in Europe

A second notable difference of European corporate governance is the structure of executive compensation. Share grants and stock options make up a smaller portion of executive compensation in continental Europe than in the US and the UK, and a higher portion of total pay is fixed instead of variable in Europe, according to research.

What executive compensation structure is optimal can be debated. However, variable pay can incentivize short-termism if it is based on short-term targets, and even targets in long-term incentive plans become short-term targets over time. In addition, if executives can sell the shares and stock options that they have been awarded as part of their compensation, they can benefit from short-term bumps to the stock price, while avoiding the long-term stock price reversal. There is some empirical evidence in the US that short-term incentives in executive compensation, in particular in the form of shares and stock options that can be sold in the short-term, indeed leads to short-term focused corporate behavior, such as cuts to investment (Edmans, Fang and Lewellen, 2017; Ladika and Sautner, 2020; Edmans, Fang and Huang, 2021).

Because executive compensation is generally structured differently in Europe than in the US and the UK, it is important to study short-termism as well from a European perspective.

Shareholder activism and engagement in Europe

Third, continental European corporate governance is also different from the UK and the US because shareholder activism and shareholder engagement play a much smaller role. Studies report that the number of activist engagements per the number of listed firms is smaller in European countries like Belgium and France than the US and the UK.

While several authors have argued that shareholder activists are excessively focused on the short term and pressure the management of a corporation to take short-termist actions, others have argued that shareholder activism boosts long-term firm performance. However, because shareholder activism is much less common in Europe, the argument that short-termism is caused by shareholder activists carries much less weight in Europe. In addition, shareholder engagement in Europe is often less confrontational than in the US.

These differences justify studying the impact of shareholder activism on short-termism in the European context as well.

Loyalty voting rights in Europe

European legislators have also adopted governance reforms with the goal of combatting short-termism. The most popular reform has been to allow corporations to grant “loyalty voting rights” to shareholders: multiple voting rights for “loyal” shareholders who have held their shares for more than a specified time period. Such loyalty voting rights are allowed in Belgium, France, the Netherlands, Italy and Spain (among other jurisdictions).

The idea behind allowing loyalty voting rights is that it encourages shareholders (and therefore indirectly corporations) to think in the long term. However, in practice loyalty voting rights seem to be mostly used by controlling shareholders to strengthen their control (or retain their control when selling shares or not participating in new share issuances). Practical barriers make loyalty voting rights de facto unavailable for long-term institutional investors. Whether loyalty voting rights are helpful or not for combatting short-termism therefore depends on whether you believe controlling shareholders generally are more long-term oriented or not.

This debate on loyalty voting rights in Europe also justifies studying short-termism in the European context.

Conclusion

These topics, and many others, will be addressed more comprehensively by our speakers and discussants during the conference on “short-termism in European corporate governance” on 30 May in Antwerp. Registration is still possible and is free for academics and students (€100 for practitioners). Participants can attend online or in person in Antwerp. The program and more information can be found here.

Tom Vos Visiting professor at the Jean-Pierre Blumberg Chair at the University of Antwerp Associate at Linklaters Belgium Voluntary scientific collaborator at the KU Leuven

Schrijf nu in voor de ‘disputatio‘ op donderdag 1 juni 2023 te Leuven

Author: Tom Vos

Tom Vos is an assistant professor at the Department of Private Law of Maastricht University. In his research, he focusses on corporate law, corporate governance, law and economics, and empirical studies. In addition to that, Tom is a visiting professor (10%) at the Jean-Pierre Blumberg Chair at the University of Antwerp, where he teaches a course on international corporate governance. Finally, Tom is a (part-time) Associate at the Corporate and Finance Practice at Linklaters Belgium, where he advises clients on corporate governance and securities laws.

View all posts by Tom Vos

")