“Jackalope is an easy process. This is definitely something that I will be using. It links directly to Bigfoot’s online work comp application so I will no longer need to complete Acord forms. This process is awesome. Filling out paper applications can take up so much time, I have to sit down and force myself to fill them out. Agents sometimes just want an estimation and this process does exactly that. ” – Insurance Agent.

“This is fantastic. Very quick. I can search many different industries and class codes all at the same time. This is very impressive, it outlines everything nicely. I like it and I will be using it. I am looking forward to getting an indication before I request a formal quote. It is great to compare different carriers and their potential prices. This will help me shop in one place. How soon can I access it?!? ” – Insurance Agent.

For frequently asked questions, click HERE.

To learn more about the Jackalope Program, check out our past blog for updates HERE.

Contact Sara Bullock for a demo and join these agents in getting multiple carrier indications instantly.

By Andrew Paulson, CSLP, Lead Student Loan Consultant and Co-Founder of our partner site StudentLoanAdvice.com

On July 18, 2024, the Saving On a Valuable Education (SAVE) plan was temporarily blocked by a legal injunction. This move, driven by Republican lawmakers from several states, is being reviewed by the conservative-leaning Eighth Circuit Court of Appeals. This court previously played a critical role in halting President Biden’s initial attempt at student loan forgiveness, and many anticipate a similar fate for the SAVE plan.

Here’s what we know about a timeline on SAVE.

July 18, 2024: Legal injunction halts SAVE, placing borrowers in forbearance. Loan servicers stop processing applications for Income Driven Repayment (IDR) plans, temporarily pausing progress toward loan forgiveness.

October 24, 2024: Oral arguments to be heard in the Eighth Circuit Court.

November 2024: A ruling from the Eighth Circuit Court is expected, with a likely appeal to the Supreme Court, regardless of the decision.

Spring 2025: Oral arguments at the Supreme Court.

Summer 2025: The Supreme Court’s final ruling on SAVE, deciding its fate.

Given the current 6-3 conservative majority on the Supreme Court, it’s very difficult to envision SAVE surviving. The result of our upcoming election could also play a role. Under a Kamala Harris presidency, we might see more proposals for loan forgiveness and more generous repayment options. Under another Donald Trump presidency, I’d anticipate efforts to end loan forgiveness and upend pro-borrower initiatives.

Immediate Impact on SAVE Borrowers

While this legal case ensues, borrowers currently in the SAVE plan are placed into forbearance, similar to the COVID-era pause. No payments are due, and interest is frozen. Not a bad deal while the legal case shakes out, right? Well, here’s another other piece about this type of forbearance: it does NOT COUNT toward PSLF or IDR forgiveness. That means your clock for either forgiveness track is temporarily halted.

Moreover, if you want to enroll in another IDR plan, loan servicers aren’t even processing applications to switch plans now. It’s an administrative mess leaving millions of borrowers in limbo. Hopefully, IDR application processing will resume soon and prior to the legal resolution.

One more thing regarding the legal forbearance. You may have the chance to get PSLF credit for all of these months in forbearance using the PSLF Buyback Program.

3 Backup Plans If SAVE Is Eliminated

If SAVE is blocked, here are three alternative strategies to consider.

#1 Income Based Repayment to Public Service Loan Forgiveness

Currently, there is only one income driven repayment plan available to borrowers: the Income Based Repayment (IBR) Plan. IBR has two versions, each with specific criteria:

Old IBR (borrowed before July 1, 2014) requires 15% of discretionary income.

New IBR (began borrowing after July 1, 2014) requires 10% of discretionary income (similar to PAYE and SAVE).

However, IBR has an income qualification called a Partial Financial Hardship (PFH). If your income exceeds what you owe, you may not qualify for PFH, making it impossible to enroll in IBR. Many will need to apply for IBR while in training (usually physicians) to meet the PFH requirement. This is a key consideration you should look at, particularly if you’ve recently graduated training or your income is on the rise. I suspect there will be many docs who try to switch into IBR who make too much.

Suppose you’re a doctor who is pursuing PSLF with $325,000 in federal student loans. You have six more years to go with PSLF and make $275,000. Here’s an idea of your monthly payments in SAVE, Old IBR, and New IBR.

Monthly payments in SAVE and New IBR are comparable. But Old IBR is quite a bit more.

Here are the total payments over six more years.

Switching into IBR is not usually a deal breaker for PSLF. In a lot of cases, it still makes sense. This doc is still saving over $100,000 to do PSLF over private refinancing. New IBR vs. SAVE is quite similar in overall payments. But you’d end up paying quite a bit more if you only qualify for Old IBR as an alternative to SAVE.

If you’re contemplating the move into IBR, it’s best to run the numbers to ensure you can qualify and if it’s still going to save you money.

More information here:

The Role of Student Loan Refinancing in 2024

#2 REPAYE to Public Service Loan Forgiveness

If SAVE is struck down, there’s a chance its predecessor, Revised Pay As You Earn (REPAYE), could be reinstated. REPAYE was a great option for many borrowers and was generally more affordable than Old IBR. Payments in REPAYE were 10% of discretionary income. REPAYE had no PFH, so borrowers could enroll in it even with incomes greater than their student loan balance.

However, there are two key pitfalls to REPAYE.

Spousal Income: REPAYE does not allow you to exclude spousal income if you file separately

No Payment Cap: Unlike IBR and PAYE, REPAYE does not cap payments at the 10-year standard repayment

Generally, docs liked REPAYE while in training or early career because payments were affordable and there was an interest subsidy to help keep the loan balance from spiraling out of control.

Say you’re a doctor who is married to an attorney. You make $250,000, and your spouse makes $225,000. Your student loan balance is $250,000, and you’re four years out from PSLF.

If you file jointly, here’s an idea of your payments:

Monthly payments are not too different across the IDR spectrum. Payments in IBR would be lower, though, because of the payment cap.

Over a four-year period of time, you can see the difference grows larger.

Suppose the doc is looking to file taxes separately to keep their high-earning spouse’s income out of the picture.

Payments in REPAYE still take into account spousal income, whereas both IBRs and SAVE exclude it. Over a four-year period of time, this has massive ramifications for future payments.

New IBR vs. REPAYE payment difference is almost $100,000 over four years! It’s very important you get into the right repayment plan for your unique situation. Otherwise, you could be throwing away tens to hundreds of thousands of dollars.

Once the dust settles on SAVE, you should run the numbers on the existing IDR options to ensure you’re on the optimal path forward to being debt-free.

#3 Private Refinancing

The private refinancing of student loans has taken a backseat in recent years—largely due to rising interest rates, which increased by roughly 5% over the past 2-3 years. During the COVID-19 pandemic, federal student loan payments were paused and interest was frozen, making refinancing less appealing. Most borrowers opted to keep their loans federal to benefit from zero interest and potential forgiveness options. Generous repayment plans, like SAVE and REPAYE, helped subsidize interest for borrowers. And the effective interest rate (after the interest subsidy was applied) was often lower than what they could receive from private lenders while in their early careers. All of these factors made refinancing federal student loans a much harder sell. One private refinancer even left the business altogether.

However, the refinancing landscape may be changing. For the first time in over four years, the Federal Reserve cut interest rates in September 2024. It lowered the rate by 0.5% with another cut expected in November and more reductions anticipated in 2025. This is fantastic news for those who were planning to refinance their loans and not do PSLF.

Say a cardiologist owes $250,000 in federal student loans at 7% and works in private practice. They are contemplating exiting the federal 10-year standard repayment plan for private refinancing. In recent years, they hadn’t applied because their rate was zero during COVID and they knew interest rates weren’t great. They receive quotes from private lenders, and they are pleasantly surprised with the lower rates. They pull the trigger and refinance their loans to a 5% interest rate on a 10-year term.

They pay their loans down over a 10-year term. As a result of privately refinancing their student loans, they save $30,129 in interest.

Refinancing your loans is always a no-brainer on your private student loans whenever you can lower the interest rate. However, refinancing your federal loans is a harder decision. It converts your federal loans into private, and those loans would no longer be eligible for any federal programs, such as IDR or PSLF. But if you’re positive you’re not going for PSLF, it’s a surefire way to save you money and reduce the hassle. Plus, you’ll no longer have to be on the federal student loan rollercoaster.

More information here:

Refinancing Medical Student Loans in Residency – A Step-by-Step Guide

The Bottom Line

With the fate of SAVE tied up in the courts, having a backup plan is essential. Whether it’s switching to IBR or REPAYE or considering private refinancing, the path forward requires careful planning. Stay informed and run the numbers with a student loan pro to ensure you’re making the best decision for your financial future.

If you’re thinking about refinancing your student loans, there’s no better place to do it than through one of our partners.

** White Coat Investor accepts advertising compensation from these companies. Page order does not guarantee best possible rate and terms. † Bonus includes cash rebates and value of free course. Borrowers who refinance more than $60,000 in student loans using the WCI links will be enrolled in The White Coat Investor’s flagship course, Fire Your Financial Advisor: ATTENDING for free ($799 value). Borrowers will still receive the amazing cash rebates that WCI has negotiated with each lender. Offer valid for loan applications submitted from May 1, 2021 through October 31, 2024. Free course must be claimed within 90 days of loan disbursement. To claim free course enrollment, visit https://www.whitecoatinvestor.com/RefiBonus.

What do you think? What actions will you take if you have student loans? What is your backup plan during the SAVE legal proceedings? Comment below!

Musk, who is worth $241 billion, has only made modest donations to federal candidates until this election season | (Photo: Reuters)

3 min read Last Updated : Oct 16 2024 | 9:10 AM IST

By Bill Allison and Dana Hull

Elon Musk poured $75 million into the super political action committee he created earlier this year, launching the Tesla Inc. and SpaceX chief executive officer into the top tier of political donors as he pays for much of the ground game for Donald Trump’s campaign.

Click here to connect with us on WhatsApp

Musk’s super PAC is paying for Trump’s get-out-the-vote operations in battleground states in an effort to bolster turnout for the former president and Republicans in swing districts that could help the GOP win a House majority. The group, America PAC, is also spending on digital ad campaigns, some of which target young men, trying to get them to the polls to offset Harris’ advantage among women voters.

Musk was America PAC’s only donor, making seven separate contributions between July 3 and Sept. 5, according to its latest filing with the Federal Election Commission. The group spent $72 million and started October with $4 million cash on hand. The bulk of its spending, $68.5 million, supported Trump.

The PAC, which advertises on X — the social media platform that Musk owns — for canvassers offering to pay up to $30 an hour, says it was created to support candidates who favor a range of issues including securing borders, public safety and free speech.

The moves are the latest demonstration of how Musk, whose companies boast billions of dollars worth of federal contracts and who has personally bristled at government regulations, is expanding his political influence network to include a potential future president and members of Congress.

Musk, who is worth $241 billion, has only made modest donations to federal candidates until this election season.

Musk has become an increasingly vocal backer of Trump, using his social media platform X, formerly known as Twitter, to promote the former president as well as amplify claims he’s made blaming immigrants for increased violence. Musk’s account on X includes a link to America PAC while his X profile says platform users should read his posts “to understand by I’m supporting Trump for President.”

Trump invited Musk to share the stage with him at a rally on Oct. 5, calling him “a truly incredible guy.” The event was held at the same venue in Butler, Pennsylvania, where Trump was wounded in a failed assassination attempt in July. Musk publicly endorsed Trump on X that evening.

The former president has said he would ask Musk to join his administration should he win a second term, heading up an effort to cut government waste nicknamed the Department of Government Efficiency, or DOGE, a reference to a cryptocurrency Musk has embraced.

Deep-pocketed donors are playing a critical role in supporting Trump, who lags far behind Vice President Kamala Harris in fundraising. She’s been outspending his campaign in all seven of the battleground states that will decide the election in the final stretch since Labour Day according to data from AdImpact. Her media buys total $314 million compared to $173 million for Trump.

Harris’ financial advantage has also allowed her to open more then 330 field offices staffed with more than 2,000 paid employees to help conduct its voter mobilisation operations. With polling margins razor thin — Trump’s lead in the Real Clear Politics average of battleground state polls is 0.7 per cent — how much campaigns have to spend can be decisive.

In the third quarter of 2024, Bank of America (BofA) saw a decline in mortgage production, despite a drop in interest rates that benefited competitors like Wells Fargo, JPMorgan Chase and Citi.

BofA announced on Tuesday that it posted $5.3 billion in first-lien mortgage volume from July to September, a 7% decline from the $5.7 billion recorded in the previous quarter and a 4% decrease compared to its $5.5 billion total in Q3 2023. In second-quarter 2024, the bank’s mortgage origination volume jumped 66%.

Chief financial officer Alastair Borthwick explained that consumer banking loan growth was largely driven by credit cards, small-business loans and auto loans. But this overall growth was muted by a decline in mortgage balances as paydowns exceeded originations in a higher rate environment.

Citi, which also announced its earnings on Tuesday, reported a more positive performance with $3.9 billion in originations, up 7% from the prior quarter and up 18% year over year.

Last week, JPMorgan maintained its top position among depository mortgage producers with $11.4 billion in Q3 volume, followed by Wells Fargo at $5.5 billion. Combined, the four largest depository mortgage lenders produced roughly $26 billion in mortgages from July through September.

Nonbank mortgage lenders such as Rocket Mortgage, United Wholesale Mortgage, loanDepot, Pennymac, Newrez and Mr. Cooper, among others, are expected to release their quarterly earnings in the coming weeks.

Home equity

BofA’s home equity loan production also dropped. In Q3 2024, the bank originated $2.28 billion in home equity loans, a 4.3% decline from the $2.39 billion reported in Q2 and a 5.4% decrease from $2.42 billion in Q3 2023.

The bank’s total outstanding residential mortgages stood at $227.8 billion as of Sept. 30, compared to $227.5 billion in Q2 and $229 billion in Q3 2023. Its home equity portfolio was valued at $25.48 billion at the end of the third quarter, compared to $25.44 billion in Q2 2024 and $25.49 billion in the same period last year.

Bank of America’s total mortgage-backed securities had a fair market value of $70.3 billion as of Sept. 30, up from $57.1 billion on June 30.

Despite the declines in its first mortgage and home equity sectors, BofA reported a steady net income of $6.9 billion in Q3 2024, mirroring last year’s figures. The consumer banking division contributed $2.7 billion to this total. Credit loss provisions remained at $1.5 billion, according to filings with the Securities and Exchange Commission (SEC).

BofA chairman and CEO Brian Moynihan said in a statement that the bank’s team produced another “solid earnings result.”

Company executives told analysts that despite planned revisions to the proposed Basel III Endgame capital rules, which were announced by Federal Reserve officials, the company’s capital strategy has not changed.

The best news is that you don’t need any coding or design skills to get professional results from this premium WordPress theme – you can leave that to us.

A wonderful serenity has taken possession of my entire soul, like these sweet mornings of spring which I enjoy with my whole heart. I am alone, and feel the charm of existence in this spot, which was created for the bliss of souls like mine. I am so happy, my dear friend, so absorbed in the exquisite sense of mere tranquil existence, that I neglect my talents. I should be incapable of drawing a single stroke at the present moment; and yet I feel that I never was a greater artist than now.

With impeka, your website will be fast.

When, while the lovely valley teems with vapour around me, and the meridian sun strikes the upper surface of the impenetrable foliage of my trees, and but a few stray gleams steal into the inner sanctuary, I throw myself down among the tall grass by the trickling stream; and, as I lie close to the earth, a thousand unknown plants are noticed by me: when I hear the buzz of the little world among the stalks, and grow familiar with the countless.

I am so happy, my dear friend, so absorbed in the exquisite sense of mere tranquil existence, that I neglect my talents. I should be incapable of drawing a single stroke at the present moment; and yet I feel that I never was a greater artist than now.

Web Design

User experience

Multipurpose WordPress theme

Handcrafted elements

A wonderful serenity has taken possession of my entire soul, like these sweet mornings of spring which I enjoy with my whole heart. I am alone, and feel the charm of existence in this spot, which was created for the bliss of souls like mine. I am so happy, my dear friend, so absorbed in the exquisite sense of mere tranquil existence, that I neglect my talents. I should be incapable of drawing a single stroke at the present moment; and yet I feel that I never was a greater artist than now.

The post About inbound marketing first appeared on Optima.

Get the hottest Fintech Singapore News once a month in your Inbox

OKX, a global cryptocurrency exchange and onchain technology company, has named Yuri Mushkin as its Global Chief Risk Officer.

Yuri Mushkin

Based in Singapore, Mushkin will oversee the company’s global risk strategy and lead its independent enterprise risk function, reporting to the CEO and Board of Directors.

Mushkin previously worked at McKinsey Investment Office Partners, where he managed over US$20 billion across public and private markets.

With over 20 years of experience in capital markets and risk management across traditional and digital assets, he has held senior positions at firms such as Goldman Sachs and McKinsey & Co.

This appointment comes as OKX expands its global presence. OKX recently launched operations in the UAE and its Singapore entity obtained a Major Payment Institution license in September.

Earlier this year, OKX established its European base in Malta to comply with Markets in Crypto-Assets (MiCA) regulations.

OKX publishes its Proof of Reserves on a monthly basis to provide transparency.

Star Xu

Star Xu, Founder and CEO, OKX said,

“Strong risk management has always been a top priority for us and part of our DNA. We’ve demonstrated our resilience over more than 10 years navigating multiple crypto market cycles and our global stakeholders now include the leading regulatory agencies, financial institutions and corporate partners.

I’m thrilled to welcome Yuri as our Global Chief Risk Officer. His appointment is part of our continued investment in building products that meet the high expectations of our customers and global stakeholders.”

The first step in determining whether a car is totaled (or, in insurance terms, a total loss) is to calculate its actual cash value (ACV) at the time of the loss. The ACV is how much your vehicle is worth after factoring in depreciation. On average, vehicles depreciate more than 20 percent in the first year and approximately 10 percent each additional year for the first five years, according to Carfax data.

How is total loss value calculated?

At our agency, a claims adjuster assesses your vehicle’s condition. Then, they run the make, model, and year of your vehicle through an industry-leading vendor database. The database generates an accurate estimate of your vehicle’s market value based on its mileage, condition, options, and other comparative factors. The database also considers the demand for a particular vehicle in your local market. For example, a pickup truck could fetch a higher price in a rural area than in a heavily populated city.

Another factor is the resale value of the parts and the metal. This factor, known as the “salvage value,” is considered along with the cost of repair.

If a vehicle’s cost of repair plus its salvage value exceeds the vehicle’s ACV, it is typically declared a total loss. (One exception is certain state laws that require insurance companies to declare a vehicle a total loss even if the cost of repair and salvage value are less than the ACV.)

How much does insurance pay for a totaled car?

If your vehicle is a total loss, you have two choices: You can take the cash settlement for the ACV of your vehicle, or, if your state allows, you can “retain the salvage” and request the title and damaged vehicle be returned to you.

Most customers choose to take the settlement value, which is the figure generated by the industry-leading vehicle valuation database. Payment goes to the customer if the vehicle is owned outright. If there’s a lienholder, such as a bank or a credit union, payment goes to that lienholder. (Anything left over after paying the lienholder, however, goes back to the customer.) All payments are made after subtracting the customer’s deductible.

What insurance can help pay for a totaled car?

The two most common are collision coverage and comprehensive coverage. If you have these optional coverages on your auto policy, you have protection up to the actual cash value amount if your vehicle is declared a total loss. Collision coverage protects you if you hit another car or overturn. Comprehensive coverage protects against events like fire, vandalism, or hitting a deer.

What happens when your car is totaled, and you still owe money on it?

It’s true: A new car depreciates when you drive it off the lot. Since the cash payout for a totaled car is based on actual cash value – not the amount you have left on your car loan – you could be in a tough spot if your car is totaled and you still owe money.

Good news: There’s a way to protect your investment. Consider adding the Auto Security Coverage Endorsement1 to your auto policy for a few extra dollars per month. If you have a lease or loan on your vehicle, the endorsement will help if you owe more on the vehicle than what it’s worth. Talk to your agent about how this coverage works.

ERIE® insurance products and services are provided by one or more of the following insurers: Erie Insurance Exchange, Erie Insurance Company, Erie Insurance Property & Casualty Company, Flagship City Insurance Company and Erie Family Life Insurance Company (home offices: Erie, Pennsylvania) or Erie Insurance Company of New York (home office: Rochester, New York). The companies within the Erie Insurance Group are not licensed to operate in all states. Refer to the company licensure and states of operation information.

The insurance products and rates, if applicable, described in this blog are in effect as of January 2024 and may be changed at any time.

Insurance products are subject to terms, conditions and exclusions not described in this blog. The policy contains the specific details of the coverages, terms, conditions and exclusions.

The insurance products and services described in this blog are not offered in all states. ERIE life insurance and annuity products are not available in New York. ERIE Medicare supplement products are not available in the District of Columbia or New York. ERIE long term care products are not available in the District of Columbia and New York.

Eligibility will be determined at the time of application based upon applicable underwriting guidelines and rules in effect at that time.

Your ERIE agent can offer you practical guidance and answer questions you may have before you buy.

Some facts surrounding the history of the stock market are really astonishing. I would like to invite you into the world of Wall Street. Let us dive into my list of interesting stock market fun facts you should know about the global and US markets.

Around 54% of US households own stocks directly or indirectly through mutual funds, index funds, retirement accounts, etc. That’s a lot of money invested in the markets, so knowing more about the Stock Market only makes sense.

The NYSE Is The Largest Stock Exchange In The Entire World

Did you know that the New York Stock Exchange is the largest stock exchange in the entire world? With a market cap of $22.649 trillion (Jan 2023), it beats all of them. But, over the years, the growth of the NASDAQ was bigger.

Take a look at the comparison of the two stock exchanges of the U.S. Stock Market in comparison:

Source: statista.com

The title of the oldest exchange does not go to the NYSE. That is the Amsterdam Stock Exchange.

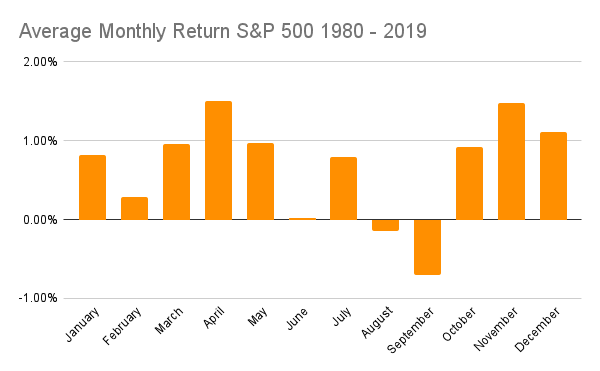

September Is The Worst Month To Invest

This phenomenon is also called the “September Effect.” Some analysts attribute this odd market behavior to seasonal effects in the markets. At the end of summer, some investors change their portfolios and cash out on some positions.

September is also the time most people have come back from their summer vacations and start doing more active trading again.

Whatever it may be, statistically, it is the worst month to invest with -0.7%, as you can see in the chart below:

The best month to invest, according to this statistic, is April and November, with 1.51% and 1.48%, respectively.

The Bull And Bear Analogy In The U.S. Stock Market

Have you ever thought about what the hell a bull and a bear have to do with the stock market?

On Wall Street, you speak of a Bull Market if everyone is in a buying mood. A Bear Market is the exact opposite. Nobody wants to buy. But what is the analogy to these scary mammals?

Apparently, the bear came before the bull. It originates in a proverb that cautions against “sell[ing] the bear’s skin before one has caught the bear.”

By the 18th century, the phrase “bear-skin jobber” was widely used as a synonym for a seller.

The bear was chosen around 1720 as a symbolic opposite to the bear. One of the first mentions of it can be found in the writings of poet Alexander Pope:

“Come fill the South Sea goblet full; The gods shall of our stock take care: Europa pleased accepts the Bull, And Jove with joy puts off the Bear.”

Another explanation that you might already have heard is the nature of how these animals attack. A bull attacks with an upward motion, while a bear attacks by slashing downward. It is certainly a more visual explanation.

There Is No 20 Year Period That Would Have Lost You Money In The S&P 500

Yes, it’s true! Take a look at the historic performance of the S&P 500 in the last 100 years.

Source: themeasureofaplan.com

Your odds of keeping your money and gaining more increase the longer you invest. When you invest for 20 years, it is pretty certain that you will at least keep the money you invested. In most instances, you will have positive annual returns!

Many Mutual Funds or ETFs allow you to invest in the S&P 500 index fund.

We all know that you would have made a fortune if you would have invested in Amazon early on. But did you know that a 90% decline would have also been in your cards on that massive gain until today? It happened in the stock market crash we now know as the Dot-Com Crash.

This shows the extreme mental challenge that you might have to go through as a long-term investor. Would you have held on to your investment if it lost 90%, or would you have lost your hope and sold?

This 90% decline would also not be the only significant one over the entire holding period. Take a look at the table below showing three more declines you would have to endure.

Just think about the emotional ride you would have to endure during these negative events.

Time Period

High

Low

Decline

April 1999-Aug. 1999

$105.06

$44.78

-57%

Dec. 1999-Sept. 2001

$106.69

$5.97

-94%

Oct. 2003-Aug. 2006

$59.69

$26.07

-56%

Dec. 2007-Nov. 2008

$94.45

$37.87

-60%

Amazon Stock Price Declines, source: Google Finance

It’s always easy to see the opportunity in hindsight, but at the time, it was much harder to see. The only way for you to gain that edge in the market is by understanding company financials. If you learn how to read financial documents (Income Statement, Balance Sheet, Cash Flow Statement), you can put yourself in a much better position. You enable yourself to see if a company has a good foundation or not.

Ronald Wayne Co-Founded Apple And Sold His 10% Shares For $800

Besides the well-known Steve Jobs and Steve Wozniak, Apple has a third Co-Founder: Ronald Wayne. Only 12 days after founding the Apple Computer Company, he sold all his shares to Steve Jobs and Steve Wozniak, amounting to 10% ownership. One year later, he accepted a final $1,500 to forfeit any future claims against the company.

It’s easy to see that this was his biggest mistake in life. He has stated multiple times that he doesn’t regret his decision, though. He just made “the best decision based on the information available at the time” (source).

COVID Recession was the shortest on record, only lasting 2 months

A recession, on average, lasts 11 months. When COVID hit, we all witnessed the shortest recession on record, with just 2 months to amount to a full recovery. It was one of the most volatile markets in history.

Take a look at the recessions from 1929 to 2022:

US Recessions from 1929 to 2022

The stark difference becomes very clear if you look at the chart showing their lengths:

Statistically, The Market Goes Up 2 Years Out Of 3

This stock market fun fact is a great one to keep in mind if you are a long term investor. David Gardner, Co-Founder of The Motley Fool talked about that in his Rulebreaker Investing podcast.

If you look at the data, the market goes up 2 years and down 1 year out of every 3 years. Of course, these are just averages. Individual 3-year periods can look dramatically different. When a bear market happens, it usually lasts for 12 to 18 months until the market goes up again.

Apple Was The First Company To Breach $1 Trillion

What do I mean by $1 Trillion? I’m speaking of the market capitalization. This is complex for the size of the company.

Every company has a finite number of shares in the market – even if it doesn’t feel that way when you buy stocks in your brokerage account. They are called shares outstanding, and you can look up that number in portals such as Yahoo Finance. If you multiply that number by the price of one share, you get the market capitalization or size of that company at that time.

Apple was the first company in the history of the stock market to ever reach $1 trillion. By the end of July 2017, Apple breached that sentimental value of $1 trillion.

What’s interesting is that if you look globally, Apple was actually not the first company to breach $1 trillion. It only holds that title in the US stock market. Dutch East India Company was a company transporting spices and luxury goods via ships to Europe in the 16th century. The company’s overall market cap reached 78 million Dutch guilders in the early 1600s. That amounts to ~$8.2 trillion today.

Microsoft’s Market Cap Is Higher Than The GDP Of Italy, Brazil, And Canada

At the time of writing, Microsoft’s market cap sits at $3.009 trillion! That is a huge number just by itself. It has a clear spot in the list of the largest companies in the world.

If you compare this to the GDP of well-known countries in the world, you can get a better sense of just how big Microsoft is:

Italy, Brazil, and Canada all lose in size compared to Microsoft. And I believe more countries are going to lose that same comparison in the future.

Right now, Microsoft and Apple are fighting for the title of the biggest company in the US stock market. It will be interesting to see how the picture develops a few years from now.

Berkshire Class A Stock Is The Most Expensive Share

The Class A stock of Berkshire Hathaway comes in at $574,515.81 a piece at the time of writing. That is an astonishing number to acquire just one stock!

Warren Buffett never performed a stock split for his Class A stock. He thinks that the disadvantages of a stock split outweigh the advantages. The high price of the stock attracts more investors with a long-term view of their investment.

Instead, he introduced a less expensive Class B stock in 1996. The goal was to allow more individual investors to invest in Berkshire Hathaway directly. At the time, fractional shares were not traded.

The Class B shares did go through a huge split of 50 to 1 in 2010. That lowered the price of one share to ~$70 at the time. Now, that same stock is trading at $380.32.

The NYSE Was Originally Named Differently

Every stock investor knows the NYSE (New York Stock Exchange) and the NASDAQ (National Association of Securities Dealers Automated Quotations). Bud, did you know that the NYSE was not always named like that?

“The exchange evolved from a meeting of 24 stockbrokers under a buttonwood tree in 1792 on what is now Wall Street in New York City.” writes one of the Encyclopaedia Britannica’s editors (source). The document that emerged from that meeting is called the Buttonwood Agreement. They formally adopted the name New York Stock and Exchange Board in 1817. The name was changed in 1863 to New York Stock Exchange – the name we know today.

US Stock Market is 54% Of The Entire Global Stock Market

Probably everybody knows that the stock market in the United States is big. But did you know that it represents almost half of all global financial markets? Sometimes, it is hard to wrap your head around how big it really is!

Take a look at how the different markets compare in Q4 of 2023:

The dominance of the US Stock Market is undeniable.

The S&P 500 Goes Up 55% And Down 45% Of The Time

This Stock Market fun fact might come as a surprise to you if you are not an investor. On a day-to-day basis, one might think that the odds are 50:50 for the market to go up or down – basically a coin flip. But that is not the case.

Andrew Sather has analyzed the historical data of the S&P 500 from 1996 to 2021. He found that from 1996 to 2016, there were 53.29% of up-days and 46.71% of down-days. From 2016 to 2021, there were 54.86% of up-days and 45.14% of down-days.

So, the odds are indeed a tiny bit better than a coin flip. And this is part of the reason why long-term investors have an edge in the market. This is true, despite the existence of stock market corrections and crashes.

Most Trades Are Made By Robots

Robots are invading all areas of our lives. And the stock market is no exception to that.

In 2017, JPMorgan estimated that 60% of trades are done by robots or automated stock investment programs. Estimates for 2023 come in at 60-73%.

I expect the number of stock trading done by algorithms to climb even more in the coming years, especially with AI-powered tools gaining much more momentum. Tools that invest based on technical analysis of the stock prices are available in all shapes and forms now. They often focus on a short term trading strategy.

Final Thoughts – 15 Interesting Stock Market Fun Facts You Should Know

And this is my list of interesting stock market fun facts. I love diving into the world of stock market statistics and interesting facts. It is a fun exercise for me! It can teach you a lot about how these global markets are really working.

Whether you are a first time investor, or a seasoned veteran in the field, I hope you have learned something new today.

Open market purchases would help but generally this spread should fall on its own as the market prices in less interest rate volatility pic.twitter.com/iNEjhs6SAc

OEMs have prioritized higher-mix/margin vehicles for production, and as such, inventory mix has moved heavily towards light trucks. pic.twitter.com/Wh9t0VSxt0

Over easy egg hack – tent the pan with a lid. Easiest with a small pan. That way, you don’t actually need to flip it, and it’s the easiest way to cook eggs.

Check out our t-shirts, coffee mugs, and other swag here.

Subscribe here:

Nothing in this blog constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Any opinions expressed herein do not constitute or imply endorsement, sponsorship, or recommendation by Ritholtz Wealth Management or its employees.

The Compound, Inc., an affiliate of Ritholtz Wealth Management, received compensation from the sponsor of this advertisement. Inclusion of such advertisements does not constitute or imply endorsement, sponsorship or recommendation thereof, or any affiliation therewith, by the Content Creator or by Ritholtz Wealth Management or any of its employees. Investing in speculative securities involves the risk of loss. Nothing on this website should be construed as, and may not be used in connection with, an offer to sell, or a solicitation of an offer to buy or hold, an interest in any security or investment product.

This content, which contains security-related opinions and/or information, is provided for informational purposes only and should not be relied upon in any manner as professional advice, or an endorsement of any practices, products or services. There can be no guarantees or assurances that the views expressed here will be applicable for any particular facts or circumstances, and should not be relied upon in any manner. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment.

The commentary in this “post” (including any related blog, podcasts, videos, and social media) reflects the personal opinions, viewpoints, and analyses of the Ritholtz Wealth Management employees providing such comments, and should not be regarded the views of Ritholtz Wealth Management LLC. or its respective affiliates or as a description of advisory services provided by Ritholtz Wealth Management or performance returns of any Ritholtz Wealth Management Investments client.

References to any securities or digital assets, or performance data, are for illustrative purposes only and do not constitute an investment recommendation or offer to provide investment advisory services. Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.

The Compound Media, Inc., an affiliate of Ritholtz Wealth Management, receives payment from various entities for advertisements in affiliated podcasts, blogs and emails. Inclusion of such advertisements does not constitute or imply endorsement, sponsorship or recommendation thereof, or any affiliation therewith, by the Content Creator or by Ritholtz Wealth Management or any of its employees. Investments in securities involve the risk of loss. For additional advertisement disclaimers see here: https://www.ritholtzwealth.com/advertising-disclaimers

Disney World (DIS) is feeling the wrath of its fans who are sick of high prices.

A highly anticipated dining spot, The Cake Bake Shop Bakery, which is set to open at Disney’s Boardwalk at Disney World’s Epcot park sometime this fall, is going viral for its “shockingly offensive” menu prices.

Don’t miss the move: Subscribe to TheStreet’s free daily newsletter

For example, the least expensive slice of cake at the shop is $22. A single scoop of ice cream costs $8, while a lemon bar costs a whopping $16. If guests want to wash all of that food down with a refreshing Coca-Cola, they will have to cough up an extra $8.

The bakery menu displayed outside of The Cake Bake Shop Bakery by Gwendolyn Rogers at Disney's Boardwalk. pic.twitter.com/lnmTCI7ex9

The sharp criticism from fans comes during a time when consumers are falling into debt to afford a Disney trip. According to a recent survey by LendingTree, 65% of consumers who recently went on a Disney trip revealed that in-park food and beverages cost “significantly more” than they budgeted for.

Disney tickets are becoming more expensive

Food at Disney World isn’t the only thing that is increasing in price at Disney’s theme parks. Tickets to Disneyland were also recently subject to a significant price hike. For example, 1-Day tickets to Disneyland increased by up to $12, depending on the ticket.

Also, a 4-day ticket at the park is now $29 more than the previous price, and a 5-day ticket increased by $31.

Disneyland’s Magic Key Passes faced the highest price increase, rising by between $100 and $125, depending on the type of pass.

More Disney:

Disney World shuts down classic ride amidst controversy

Disney flags startling shift in consumer behavior at theme parks

Disney+ and Hulu subscriptions are getting more expensive

Higher prices at Disney’s theme parks come after the entertainment giant revealed in its second-quarter earnings report for 2024 that it is battling higher costs from inflation and is currently facing a “moderation of consumer demand” at its U.S. parks.

In the report, Disney revealed that while its revenue at its U.S. theme parks rose by 3% year-over-year, its operating income (how much a company makes after expenses) in the sector shrunk by 6%.

“While we are actively monitoring attendance and guest spending and aggressively managing our cost base, we expect Q4 Experiences segment operating income to decline by mid-single digits versus the prior year,“ said Disney in the report.

Related: Veteran fund manager sees world of pain coming for stocks

By Andrew Paulson, CSLP, Lead Student Loan Consultant and Co-Founder of our partner site StudentLoanAdvice.com

By Andrew Paulson, CSLP, Lead Student Loan Consultant and Co-Founder of our partner site StudentLoanAdvice.com

&w=696&resize=696,0&ssl=1 "US elections: Musk’s million gift cements role as a top Trump donor | World News")

"Elon musk, musk, Elon, Tesla")