I know you’re familiar with this company — Tesla Inc. (Nasdaq: TSLA).

Many of you probably own it.

If you don’t, now is the time to get back in, as the company is poised to double in the next 12 months.

I’ll say this right off the bat: Tesla is not the same company as it was just five years ago.

Love him or hate him, Elon Musk’s technological powerhouse is most well-known for its strong hold on the electric vehicle (EV) market.

Even though EVs aren’t all the rage as they were a few years ago, U.S. sales still jumped 60% year-over-year (YoY), from 1 million in 2022 to 1.6 million in 2023.

EVs have sold slower than expected lately though. This has led to price cuts and smaller profit margins.

In recent months, Tesla knocked $2,000 off the prices of the Models X and S, reducing the starting price to $77,990 for a Model X and $72,990 for a Model S.

And in the overall EV market, according to Cox Automotive, the average transaction price for a new EV decreased by 9% in first-quarter (Q1) 2024 compared to Q1 2023.

Edmunds also predicts that the EV growth rate will slow through 2024, increasing to just 8% of the new vehicle market share from 6.9% last year and 5.2% in 2022.

But this won’t last much longer. And much of this is already priced into TSLA shares.

I believe EV adoption will accelerate in the next few years; especially as the cost of making EVs continues to fall, and the government continues to incentivize buyers with steep tax credits.

And there is no other automaker better positioned to capitalize on this trend than Tesla.

But that’s not the main reason I believe it’s time to buy its stock right now. You see…

Today, Tesla is so much more than an EV company.

It’s more than a tech company.

It’s a futuristic powerhouse.

It develops some of the most advanced intellectual properties we have today — with staying power.

Meaning, because of its success in the EV market, Tesla’s products and software have infiltrated several industries.

From 2000 to 2023, Tesla filed over 3,400 patents worldwide (and counting).

This includes energy storage and generation, manufacturing automation and autonomous vehicles.

These innovations represent the present and future of the auto industry, and even the overall tech market. (More on that in a moment.)

And okay, yes. I know Tesla’s gotten a lashing in the last few years … especially its share price.

A 75% TSLA collapse from its November 2021 high to its low in January 2023 is pretty jarring…

But I believe the worst is behind us.

While it might not be up in a straight line from here, I believe that if you pick up shares of Tesla now, you’ll look back on this moment in a few years and be very happy.

In fact, just a few years ago, my subscribers had the opportunity to turn Tesla into two big winners…

I first recommended the stock in August 2019, where readers saw a 552% gain after we sold half the position in July 2020.

Two months later in September, I believed the stock was overcrowded. We sold the remaining half of the position for a 919% gain.

Now, I don’t think we’ll see that in the next 12 months.

But this kind of return is likely throughout the rest of the decade — and potentially even more!

Why?

Because aside from its niche in the EV market…

Tesla has also developed not one, but two incredible feats of engineering.

They could not only change the way we drive … but also change our lives.

Tesla’s technology could also generate billions in future revenue for the company.

Tesla’s Full Self-Driving Capabilities

Autopilot, while a groundbreaking development for driver assistance, was just the foundation.

Tesla introduced Full Self-Driving in 2020.

FSD allows Tesla EVs to drive themselves nearly anywhere with minimal driver intervention.

But let’s be clear. FSD is not fully autonomous … yet.

You still need an alert human at the steering wheel while using FSD.

According to Tesla, aside from the standard Autopilot capabilities, FSD can:

Navigate on Autopilot: Actively guide your vehicle from a highway’s on-ramp to off-ramp. This includes suggesting lane changes, navigating interchanges, automatically engaging the turn signal and taking the correct exit.

Auto Lane Change: Assist in moving to an adjacent lane on the highway when engaging Autosteer.

Autopark: Help automatically parallel or perpendicular park your vehicle, with a single touch.

Summon: Move your vehicle in and out of a tight space using the mobile app or key.

Smart Summon: Your vehicle will navigate more complex environments and parking spaces, maneuvering around objects to come find you in a parking lot.

Autosteer on City Streets: Taking Autopilot to the next level.

Traffic and Stop Sign Control: Identify stop signs and traffic lights and automatically slow your vehicle to a stop on approach, with your active supervision.

Those are some major upgrades.

So now, here’s why I think FSD is a game-changer for Tesla.

The Debut of the Tesla Robotaxi!

That’s right. I’m talking about “car-to-door,” which means fully autonomous driving with no humans at the controls.

And the more people buy Tesla vehicles that use FSD and Autopilot (AKA: the mass adoption phase)…

The more it will set the stage for the company’s Robotaxi rollout.

As InsideEVs reported, at Tesla’s 2024 shareholder vote meeting on June 13, Musk said:

“Robotaxis could rocket the company to a market valuation between $5 trillion and $12 trillion.”

That’s why I want you to mark your calendars…

Because Musk says Tesla will reveal its Robotaxi on October 10, 2024.

This is one of those technologies where its economic impact is almost impossible to fathom.

Forecasts for the value of a Robotaxi fleet are all over the place.

UBS believes that this will be a $2 trillion opportunity by 2030.

It’s so big that Cathie Wood’s ARK Invest estimates that in 2029, the Robotaxi will account for nearly 90% of Tesla’s enterprise value and earnings.

And ARK has a $2,600 price target on TSLA!

But like I said, this isn’t the only breakthrough technology Tesla has in store…

You’ll have to tune in on October 10 to find out.

If you missed my special video presentation last week, click here to see it before October 10 arrives.

Debra Martin Chase brought us girlhood cult classics like The Princess Diaries and The Sisterhood of the Traveling Pants. But about 10 years ago, Chase, who now serves as CEO of Martin Chase Productions, almost gave up on the entertainment business.

“It was just a time in business where nobody was interested in making TV or movies about women, about women of color, about people of color. It just was not happening,” Chase said during a main stage interview at Fortune’s Most Powerful Women Summit in Laguna Niguel, Calif., on Tuesday. “I would go in and pitch stuff and people’s eyes would glaze over.”

That was a tough pill to swallow for Chase, who said she had committed her career in entertainment to bringing more diversity to the big screens. She wanted to have an impact on culture and industry.

“Then all of a sudden, I found myself just throwing stuff up against the wall,” Chase said. “It didn’t have meaning for me. And if it doesn’t have meaning for me, I can’t sell it.” At that point, she thought it was the universe’s way of telling her she’d had a good run in the entertainment business. At that point, she had been with Disney for 20 years, but the people who had invested in her personally were “long gone.”

At that point, she thought of exploring other options including film finance or law (she earned her J.D. from Harvard Law School). But a longtime friend convinced her to keep course—Vernon Jordan Jr., no less. Jordan was an American business executive and civil rights attorney who was a close adviser to President Bill Clinton and executive director of the National Urban League. He passed away at his home in Washington, D.C., in March 2021 at the age of 85. Chase had known him since she was 18 years old.

He was an “expert in life and knew me well,” Chase said. “He sat there and he listened to me as I poured my heart out, and he looked at me and he said, ‘You are too old to do anything else.’”

But Jordan also told Chase: “You have a great reputation, you have great relationships, you have great experience. You need to figure out how to make it work.” That served as a slap in the face for Chase—as she demonstrated literally on stage—and kept her on the film production path.

Sisterhood has been key in surviving the entertainment business

In addition to Jordan’s advice, Chase and her fellow panelists Pearlena Igbokwe, chairman of Universal Studio Group, and Nina Shaw, founding partner of entertainment law group Del Shaw Moonves Tanaka Finkelstein Lezcano Bobb & Dang, said there has been another key to success in Hollywood: sisterhood.

“Literally, these women have held me up, and I know we’ve helped each other,” Chase said.

From left:

Nina Shaw, Founding Partner, Del Shaw Moonves Tanaka Finkelstein Lezcano Bobb & Dang; Debra Martin Chase, Chief Executive Officer, Martin Chase Productions;

Pearlena Igbokwe, Chairman, Universal Studio Group

Kristy Walker/Fortune

And these three women have been supporting each other for a long time. Shaw first met Chase when she was a summer clerk and Chase was a paralegal—and the two of them were friends with Anita Hill, the renowned attorney who first entered the spotlight after giving her testimony in the 1991 Senate confirmation hearings for U.S. Supreme Court nominee Clarence Thomas, whom she accused of sexual harassment. Hill was also a summer clerk at the time.

“We were the three Black women,” Chase said, adding she had also met Igbokwe early on in her career—and now the two work together. Igbokwe currently oversees more than 100 projects across more than 25 platforms worldwide, bringing us hits like Law & Order and Hacks. “It’s the sisterhood.”

Chase also discovered other renowned writers, producers and actors including Shonda Rhimes, Anne Hathaway, Blake Lively, and Jesse Williams. Shaw credits Chase with introducing her to musician John Legend, who is now her client. Legend’s producing partner had contacted Chase one night in search of a lawyer and Shaw happened to be in the car with Chase that night. The two of them headed to Legend’s house that night and signed him, which led to other major connections for Shaw—including Quinta Brunson, creator of the hit TV show Abbott Elementary.

While these three women are dominating the entertainment industry, none of their paths were linear—or easy.

“I say to people I was a 30-year overnight sensation,” Igbokwe said. “When I got this job as chairman, [people said] ‘she came out of nowhere. For some people, that was the perception. For me, it was steadily working in the business.”

In Europe, shareholder approval and pre-emption rights have traditionally fulfilled an important role in protecting shareholders in listed corporations against excessive dilution in share issuances. However, these protections also make it costlier and slower to raise capital through share issuances. That is why countries generally allow shareholders to authorize the board of directors to issue shares without shareholder approval and without pre-emption rights – within certain limits. The protection offered by pre-emption rights and shareholder approval therefore depends on the extent to which shareholders are willing to approve authorizations to issue shares and disapply pre-emption rights.

In a paper recently published in the Journal of Corporate Law Studies, I provide new empirical evidence on the flexibility of such authorizations in practice in French and Belgian listed corporations. Proxy advisors and (associations of) asset managers have adopted guidelines on the maximum size for authorizations – typically 50% of legal capital for authorizations to issue shares with pre-emption rights, and 10% of legal capital for authorizations to issue shares without pre-emption rights (although Glass Lewis is more flexible for Belgium, with thresholds of 100% and 20%, respectively).

However, my evidence shows that these guidelines are often not followed in Belgium and France. Outside the BEL 20, Belgian corporations almost never respect the 50% limit recommended by ISS. In addition, for authorizations to disapply pre-emption rights, 55% of Belgian corporations do not observe the 20% limit (recommended by Glass Lewis) and 69% do not observe the 10% limit (recommended by ISS). Even in the BEL 20, 47% of corporations do not observe the 10% limit and 27% do not observe the 20% limit.

The guidelines of institutional investors seem to be respected more often than in Belgium. For example, in the CAC 40, the largest index in France, there are no corporations that do not respect the 50% limit for general authorizations and only 4 corporations that do not respect the 10% limit for authorizations to disapply pre-emption rights. Outside the CAC 40, compliance with the guidelines is less common: 28% of corporations do not respect the 50% limit and 67% of corporations do not respect the 10% limit.

These empirical findings stand in stark contrast with the situation in the UK, where previous research has found that the Pre-emption Guidelines and Share Capital Management Guidelines (which impose similar restrictions on authorizations) are widely observed by UK corporations.

I also provide empirical evidence through a multiple regression model that authorizations are generally more flexible in corporations with high levels of insider ownership, corporations with a smaller market capitalization, and Belgian corporations. I offer several potential explanations for these differences.

First, higher insider ownership generally makes it easier for insiders to control the vote in the general meeting and force through more flexible authorizations that benefit them. This does not necessarily mean that high levels of insider ownership are inefficient, as controlling shareholders may also have benefits.

Second, small corporations may have more flexible authorizations than large corporations because small corporations generally receive less attention from investors, activists, the media and research analysts. Alternatively, it may be that smaller corporations have higher capital needs, and therefore need more flexible authorizations.

Finally, the difference between Belgium and France could be explained by differences in the legal framework. Authorizations in Belgium are almost invariably given for the maximum period allowed by the law, five years. In France, the law imposes a shorter maximum duration on authorizations of 26 months. If shareholders can vote more often on authorizations, they have more opportunities to hold insiders accountable, which could explain the stricter authorizations in France. In addition, French law requires that shareholders vote on separate resolutions for authorizations for share issuances with pre-emption rights and authorizations for share issuances without pre-emption rights, while this is not the law or market practice in Belgium. Separate votes for pre-emptive and non-pre-emptive authorizations can ensure that shareholders are not coerced into voting for excessive authorizations for non-pre-emptive share issuances out of an unwillingness of voting against any form of authorization for the corporation, which would likely be inefficient. The lack of separate votes can explain why only 8 of 84 Belgian corporations have adopted stricter authorizations for non-pre-emptive share issuances than for pre-emptive share issuances.

The paper also analyzed whether authorizations to issue shares could be used as a takeover defense. Here, a similar picture emerges: despite the fact that the guidelines of proxy advisors and asset managers generally oppose takeover defenses, more than 40% of Belgian corporations and 28% of French corporations have an authorization to issue shares that can be used as a takeover defense. Again, such takeover defenses are more common in corporations with high levels of insider ownership and corporations with a smaller market capitalization. Institutional ownership is also significantly negatively associated with the likelihood of adopting an authorization that can be used as a takeover defense. The difference between Belgium and France is no longer statistically significant, however. A possible explanation is that the default rule in Belgium is that authorizations to issue shares cannot be used as a takeover defense, while the default rule is the opposite in France. This difference in the default rule may be enough to counterbalance the general trend of more flexible authorizations in Belgium than in France.

The empirical analysis in the paper was not designed to test whether the currently adopted authorizations are too flexible or too strict. Nevertheless, I do believe that the differences in the legal framework identified between Belgium and France could inspire policy proposals that give shareholders a larger say in the flexibility of authorizations to issue shares and disapply pre-emption rights. For example, the legal rule in France that requires a shareholder vote every two years and a separate shareholder vote on the authorization to disapply pre-emption rights could also be introduced in Belgium. It is possible that such reforms will not be effective in reducing the size of authorizations, either because shareholders believe the current flexible authorizations are efficient, or because a controlling shareholder makes it impossible for other shareholders to have an impact on the shareholder vote anyway. Even in that case, these policy proposals would be relatively harmless, as the costs of implementing them are limited: management may need to spend some extra effort in convincing shareholders that the authorization is justified, but the authorization can simply be approved during the annual general meeting that would have to be organized anyway. In addition, corporations would retain the possibility to adopt more flexible authorizations if this is efficient, provided that they can convince a sufficient number of shareholders of this.

That is why I argue that these low-cost proposals can help to empower shareholders to decide how the balance between flexibility and accountability should be struck with regards to authorizations to issue shares.

Tom Vos

Visiting professor at the Jean-Pierre Blumberg Chair University of Antwerp; Attorney at Linklaters LLP; Voluntary Scientific collaborator at the KU Leuven

Author: Tom Vos

Tom Vos is an assistant professor at the Department of Private Law of Maastricht University. In his research, he focusses on corporate law, corporate governance, law and economics, and empirical studies. In addition to that, Tom is a visiting professor (10%) at the Jean-Pierre Blumberg Chair at the University of Antwerp, where he teaches a course on international corporate governance. Finally, Tom is a (part-time) Associate at the Corporate and Finance Practice at Linklaters Belgium, where he advises clients on corporate governance and securities laws.

View all posts by Tom Vos

Fintech is booming in Australia! The sector is now worth around $45billion AUS (over $30billion USD) – a 17900 per cent rise from 2015’s value ($250billion AUS/$168million USD) according to FintechAustralia. But what subsectors are leading the way and can the country keep up its growth?

First, let’s take a step back and look at the financial landscape in Australia more generally. Despite its market stalling in H1’24, Australia’s economy still remains a major player globally with a gross domestic product (GDP) per capita of over $65,000 according to the WorldBank.

According to the KPMG Fintech Landscape 2023, the ecosystem is very diverse in Australia with over 830 independent fintechs headquartered in the region.

The fintech landscape

The Australian state of New South Wales, home to the country’s capital, has the largest percentage of fintech companies (60 per cent). This is followed by Victoria (24 per cent) and Queensland (12 per cent).

The country is also home to various unicorns. These include cross-border payments Airwallex, buy now pay later (BNPL) Afterpay and challenger bank Judo Capital.

The payments subsector is the largest in Australia. It has a 20 per cent share of all fintechs in the country with over 160 firms. Lending and wealthtech take second and third place respectively. Lending represents 17 per cent of the market (140 fintechs), while wealthtech represents 10 per cent.

Open banking is another notable subsector in Australia. The majority of the APAC region’s adoption of the technology has been market-driven – however, in Australia, regulations have driven its development. This was evident in July 2019, when Australia launched its open banking regime, based on consumer data right (CDR) legislation. The regime’s aim was to give customers more control over their data and easier access to products and services they required.

There were other milestones in 2019 too. For example, major banks celebrated application programming interfaces (APIs) and eligible product data, such as rates, fees, and terms and conditions. A year later, individual account holders and sole traders could share data relating to their retail banking products.

In 2021, data sharing was further improved as customers could share information business lending, trust accounts, overdrafts, asset finance, lines of credit and foreign currency accounts. Additionally, major banks allowed for data sharing for non-individuals, secondary users and business partnerships.

Recent news

Australia was not able to escape the declines in fintech funding experienced across the world. In terms of deal activity, it saw a 61.9 per cent decline from 42 deals in Q2’23 to 16 in QR’24. From a funding point of view, there was also a drop as the country raised $475million in Q2’24 which was 73.5 per cent lower than Q2’23 ($1.8billion).

According to Fintech Australia’s fourth edition of its Australian Open Banking Ecosystem Map and Report, which was supported by Mastercard, and in partnership with FinTech NZ, Payments NZ and Open Finance ANZ, the country saw a 165 per cent increase in consumer data right (CDR) participants. Other findings revealed that nearly all consumer bank accounts (99.74 per cent) are now connected to the open banking ecosystem, positioning Australia for further adoption of open banking technologies.

Last month, the Australian government proposed the introduction of a Scams Prevention Framework (SPF), implementing new mandatory scam obligations across all sectors. The Bill, which would insert the SPF into the ‘Competition and Consumer Act 2010,’ is expected to be introduced to the federal parliament next month.

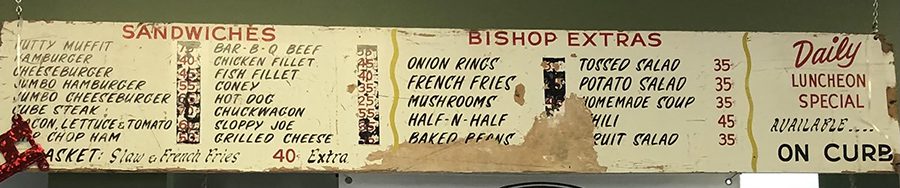

For many customers who come into Bishop’s Restaurant, located at 1638 Columbus Rd., Wooster, it feels a lot more like sitting down to eat at a family member’s house than at a restaurant.

A lot of the longtime diners are practically family to owner Denise Dorsey. She started with Bishop’s at age 16 in 1980 as a drive-in car hop when she was a student at Norwayne High School.

Bishop’s was originally located off of Cleveland Rd, at the location where College Hills Honda now calls home. It was founded in late 1959.

Bishop’s was moved in 2002 to a location south of Orrville on the busy intersection of U.S. route 30 and Wadsworth Rd, across from Riceland Golf Course. The Orrville location closed in 2011 due largely to disrepair of the building, which was connected to the Gold Star Inn, and was recently demolished.

Dorsey loved being part of the Bishop’s business so much that she took over as owner in 2009. After the 2011 closing, she gave Bishop’s a third act – starting in 2013 – at its current location.

“We offer in-person service here, you’re not going to place your order into a machine,” Dorsey said proudly. “We have a lot of customers who’ve been with us at all three locations and we’re always happy to add new ones.

“We have a relaxed dining room atmosphere and the patio will be opening soon. And we still have the car-hop service.”

Bishop’s famous Nutty Muffit, a delicious burger with cole slaw and chopped-up nuts, and onion rings are legendary in Wayne County and well beyond.

Dorsey also bakes fresh pies daily and offers the “secret” deep frying batter mix for to-go cooking, such as homemade beer-battered fish.

There are lots of other meal choices, including healthy salads.

Of course, Dorsey couldn’t do it without her restaurant staff, which includes her son, Zach Dorsey.

“Zach has been a huge part of operating this location,” Denise said. “He takes care of our maintenance and technical issues. He peels and slices the majority of the onions that we use. I really appreciate everyone who’s worked here.”

An original, oversized menu board is behind the front counter. It lists the Nutty Muffit for .75 cents, a hot dog for .25 cents and tossed salad for .35 cents.

Of course, prices have gone up over the years, but the tradition and small-town flavors remain largely unchanged.

“If it isn’t broken, don’t fix it,” said Dorsey, of keeping many of the longtime menu items and cooking techniques. “Of course, we’ve also modernized since moving to our current location and updated some of our methods.

“We have a great staff here and really appreciate our customers. They’ve even stuck with us through the COVID-19 pandemic, when we had to go to only car-hop and carry out for a while. We’re glad that most of our customers are dining in with us again – we take special precautions for cleaning and sanitation. We’re looking forward to a fun spring and summer.”

Updated on September 20th, 2024 by Bob Ciura Data updated daily

Dividends are the most common method that a company can use to return capital to shareholders. Dividend growth investors often place significant emphasis on dividend yields and dividend growth as a result.

Naturally, dividend growth investors are attracted to high-quality stocks such as the Dividend Aristocrats, an exclusive group of stocks in the S&P 500 Index with 25+ consecutive years of dividend increases.

However, there are additional ways for companies to create value for shareholders.

In addition to dividends, share repurchases are also an important part of a healthy capital return program. Debt reduction should also be welcomed by investors.

Related: Learn more about share repurchases in the video below.

There is a single financial metric that incorporates each of these factors (dividend payments, share repurchases, and debt reduction). It is called shareholder yield – and stocks with high shareholder yields can make fantastic long-term investments.

With that in mind, the High Shareholder Yield Stocks List that you can download below contains 349 stocks with positive shareholder yields, meaning that they offer a dividend, buybacks, and/or debt reduction of some kind.

The spreadsheet list was derived from the Cambria Shareholder Yield ETF.

Keep reading this article to learn more about the merits of investing in stocks with above-average shareholder yields.

What Is Shareholder Yield?

To invest in the stocks with the highest shareholder yields, you have to find them first. The High Shareholder Yield Stocks List helps identify stocks with high shareholder yields.

Shareholder yield measure how much money a company is returning to its shareholder through dividend payments, share repurchases, and debt reduction.

It is expressed as a percent, and can be interpreted as the answer to the following question: ‘How much money will be returned to me through dividend payments, share repurchases, and debt reduction if I buy $100 of company stock?’

Mathematically, shareholder yield is defined as follows:

Alternatively, shareholder yield can be calculated using company-wide metrics (instead of per-share metrics).

The common sense interpretation of shareholder-yield is the percent of your invested money that is devoted to activities that are quantitatively shareholder-friendly (dividend payments, share repurchases, and debt reductions).

How To Use The High Shareholder Yield List To Find Dividend Investment Ideas

Having an Excel document full of stocks that have high shareholder yields can be very useful.

However, the true power of such a document can only be unlocked when its user has a rudimentary knowledge of how to use Microsoft Excel.

With that in mind, this section will provide a tutorial of how to implement two additional screens (in addition to the screen for high shareholder yields) to the High Shareholder Yield Spreadsheet List.

The first screen that will be implemented is a screen for stocks that are trading at a trailing price-to-earnings ratio less than 16.

Step 1: Download the High Shareholder Yield Spreadsheet List at the link above.

Step 2: Click on the filter icon at the top of the ‘PE Ratio’ column, as shown below.

Step 3: Change the filter setting to ‘Less Than’ and input ’16’ into the field beside it.

This will filter for stocks with high shareholder yields and forward price-to-earnings ratios below 16.

The next filter that will be implemented is for stocks with market capitalizations above $10 billion (which are called large capitalization – or ‘large cap’ – stocks).

Step 1: Download the High Shareholder Yield Spreadsheet List at the link above.

Step 2: Click on the filter icon at the top of the ‘Market Cap’ column, as shown below.

Step 3: Change the filter setting to ‘Greater Than’ and input 10000 into the next field. Since the market capitalization column is measured in millions of dollars, this will filter for stocks with market capitalizations higher than $10 billion (which represent the ‘large cap’ universe of stocks).

The remaining stocks in this Excel sheet are those with high shareholder yields and market capitalizations of $10 billion or higher.

Now that you have an understanding of how to use the High Shareholder Yield Stocks List, the remainder of this article will explain how to calculate & interpret shareholder yield and will also explain some of the benefits of investing in securities with high shareholder yields.

Why Invest In Stocks With High Shareholder Yields?

There are a number of benefits to investing in stocks with high shareholder yields.

The first and perhaps most obvious benefit to investing in high shareholder yield stocks is the knowledge that the company’s management has its shareholders’ best interests at heart.

A high shareholder yield indicates that dividend payments, share repurchases, and debt reductions are a top priority for management.

In other words, high shareholder yields are correlated with a corporate culture that emphasizes shareholder well-being.

The second and more important benefit to investing in stocks with high shareholder yields is that they have a proven record of delivering outsized total returns over meaningful periods of time.

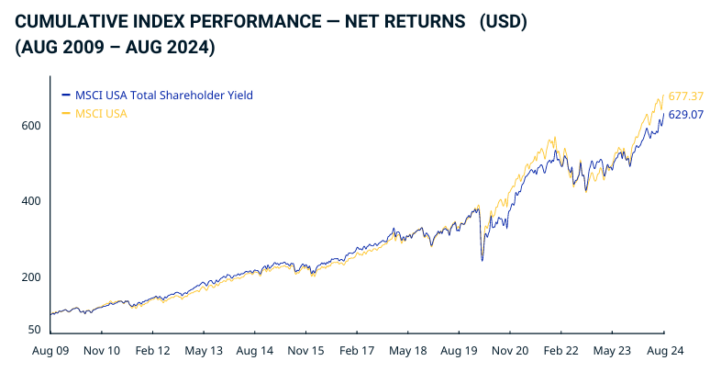

This can be seen by looking at stock market indices that focus on stocks with high shareholder yields.

For instance, the image below compares the returns of the MSCI USA Total Shareholder Yield Index to a broader universe of domestic stocks – the MSCI USA Index.

Source: MSCI USA Total Shareholder Yield Fact Sheet

Since inception, the MSCI USA Total Shareholder Yield Index has outperformed the broader index, delivering annualized returns of 7.88% per year compared with 7.25% for the MSCI USA Index.

Why is this especially impressive?

Well, it is because the past 5 years have witnessed a robust bull market and a corresponding increase in asset prices.

A significant component of shareholder yield is share repurchases. Share repurchases occur when a company buys back its stock for cancellation, increasing the part ownership of each continuing shareholders.

Importantly, share repurchases are significantly more effective during bear markets than during bull markets because the same dollar value of share repurchases can buy back a larger amount of company stock.

This common-sense characteristic of high shareholder yield stocks – that they should outperform during recessions – is an admirable trait and should be appreciated by investors who incorporate shareholder yield into their investment strategy.

But it is also impressive that these stocks have also outperformed in the past 5 years.

Top 5 Shareholder Yield Stocks Now

This section will rank the top 5 shareholder yield stocks from the spreadsheet that are covered in the Sure Analysis Research Database.

The following 5 shareholder yield stocks are ranked by 5-year annual expected returns, from lowest to highest.

Estee Lauder is one of the world’s largest cosmetics and beauty care companies. It competes primarily in the upscale and prestige portion of the market. Sales break down as follows: Skin care makes up 52% of sales, makeup constitutes 28%, fragrance is another 16%, and hair care is the other 4%.

The leading brands include the namesake Estee Lauder along with Clinique, Aveda, M.A.C., and Origins among others. Estee Lauder is a truly international firm, operating in more than 150 countries. Revenues are split almost equally in thirds between the Asia-Pacific, Europe Middle East & Africa, and the Americas segments.

The company reported its Q4 and full-year 2024 results on August 19th, 2024. Earnings-per-share of 64 cents declined from $1.08 for the same period of last year, but topped expectations. Revenues of $3.9 billion increased 7% year-over-year, marking a healthy reversal from the company’s recent sales declines.

Click here to download our most recent Sure Analysis report on EL (preview of page 1 of 3 shown below):

Shareholder Yield Stock #4: Perrigo Company (PRGO)

5-year annual expected returns: 18.3%

Perrigo is headquartered in Ireland. It operates in the healthcare sector as a manufacturer of over-the-counter consumer products.

Its Consumer Self-Care Americas segment is comprised of the U.S., Mexico and Canada consumer healthcare businesses. The Consumer Self-Care International segment includes branded consumer healthcare business primarily in Europe, but also Australia and Israel. The company generates ~$4.7 billion in annual revenue.

On August 2nd, 2024, Perrigo announced second quarter earnings results for the period ending June 30th, 2024. For the quarter, revenue decreased 10.7% to $1.1 billion, which was $60 million less than expected. Adjusted earnings-per-share of $0.53 compared unfavorably to $0.63 in the prior year, but this was $0.07 above estimates.

Organic revenue decreased 9.1% for the period. Consumer Self-Care Americas’ organic sales were down 15.1% due to weaker infant formula results and a product prioritization. Outside of Women’s Health and Healthy Lifestyle, all product categories were lower from the prior year.

Click here to download our most recent Sure Analysis report on PRGO (preview of page 1 of 3 shown below):

Shareholder Yield Stock #3: Alphabet Inc. (GOOG) (GOOGL)

5-year annual expected returns: 19.4%

Alphabet is a holding company. With a market capitalization that exceeds $2 trillion, Alphabet is a technology conglomerate that operates several businesses such as Google search, Android, Chrome, YouTube, Nest, Gmail, Maps, and many more. Alphabet is a leader in many of the areas of technology that it operates.

Alphabet has a market cap above $2 trillion, making it a mega-cap stock.

There are two classes of Alphabet stock, Class A shares, which has voting rights, and Class C shares, that do not have voting rights. This report will reference the Class A shares. On July 23rd, 2024, Alphabet declared its second ever quarterly dividend of $0.20 per share.

Also on July 23rd, 2024, Alphabet announced second quarter results for the period ending June 30th, 2024. As had been the case for several quarters, the company delivered better than expected results.

Revenue improved 13.6% to $84.7 billion for the period, topping analysts’ estimates by $450 million. Adjusted earnings-per-share of $1.89 compared very favorably to $1.44 in the prior year and was $0.04 more than expected.

Click here to download our most recent Sure Analysis report on GOOGL (preview of page 1 of 3 shown below):

Shareholder Yield Stock #2: Baxter International (BAX)

5-year annual expected returns: 22.5%

Baxter International develops and sells a variety of healthcare products, including biological products, medical devices, and connected care services devices used to monitor patients. Its products are used in hospitals, kidney dialysis centers, nursing homes, doctors’ offices, and patients at home under physician supervision.

On August 6th, 2024, Baxter International reported second quarter earnings results for the period ending June 30th, 2024. For the quarter, revenue grew 2.8% to $3.81 billion, which was $60 million above estimates. Adjusted earnings-per share of $0.68 compared favorably to $0.55 in the prior year and was $0.02 better than expected.

Starting with Q3 2023, the company now has four reportable business segments. All of the businesses within the company showed year-over-year growth on a constant currency basis. Excluding the impact of currency exchange, Kidney Care revenue was higher by 3% to $1.1 billion.

Medical Products & Therapies grew 5% to $1.32 billion, Healthcare Systems & Technologies was up 1% to $748 million, and Pharmaceuticals increased 9% to $602 million. The adjusted gross margin expanded 80 basis points to 41.2%.

Click here to download our most recent Sure Analysis report on BAX (preview of page 1 of 3 shown below):

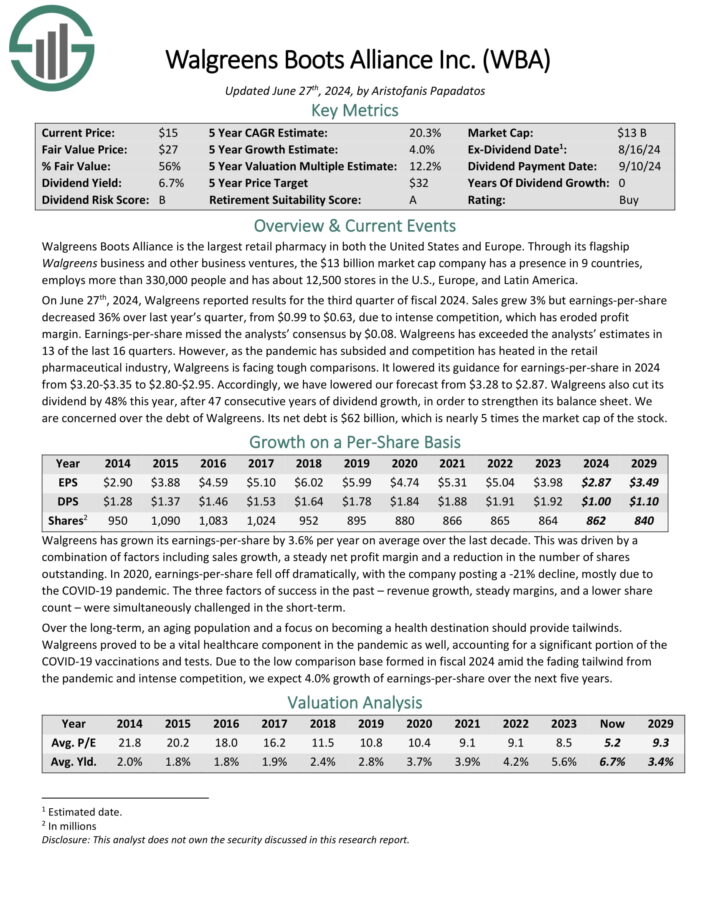

Walgreens Boots Alliance is the largest retail pharmacy in both the United States and Europe. Through its flagship Walgreens business and other business ventures, the $13 billion market cap company has a presence in 9 countries, employs more than 330,000 people and has about 12,500 stores in the U.S., Europe, and Latin America.

On June 27th, 2024, Walgreens reported results for the third quarter of fiscal 2024. Sales grew 3% but earnings-per share decreased 36% over last year’s quarter, from $0.99 to $0.63, due to intense competition, which has eroded profit margin.

Source: Investor Presentation

Earnings-per-share missed the analysts’ consensus by $0.08. Walgreens has exceeded the analysts’ estimates in 13 of the last 16 quarters.

However, as the pandemic has subsided and competition has heated in the retail pharmaceutical industry, Walgreens is facing tough comparisons. It lowered its guidance for earnings-per-share in 2024 from $3.20-$3.35 to $2.80-$2.95. Accordingly, we have lowered our forecast from $3.28 to $2.87.

Click here to download our most recent Sure Analysis report on WBA (preview of page 1 of 3 shown below):

Other Sources of Compelling Investment Ideas

Stocks with high shareholder yields often make fantastic investment opportunities.

However, they are not the only signs that a company’s management has the best interest of its shareholders at heart. Moreover, shareholder yields are only one (there are many others) of the quantitative signals that a stock may deliver market-beating performance over time.

One of our preferred signals for the shareholder-friendliness and future prospects of a company is a long dividend history. A lengthy history of steadily increasing dividend payments is indicative of a durable competitive advantage and a recession-proof business model.

With that in mind, the following databases of stocks contain stocks with very long dividend or corporate histories, ripe for selection for dividend growth investors.

Investors can also look to the dividend portfolios of successful, institutional investors for high-quality dividend investment ideas.

Large portfolio managers with $100 million or more of assets under management must disclose their holdings in quarterly 13F filings with the U.S. Securities & Exchange Commission.

Sure Dividend has analyzed the equity portfolios of the following high-profile investors in detail:

Thanks for reading this article. Please send any feedback, corrections, or questions to support@suredividend.com.

The unabridged Market’s Compass Emerging Markets Country ETF Study will be published next Monday but last week’s explosive positive price action in the iShares MSCI Emerging Markets ETF or EEM, and a number of EM Country ETFs is noteworthy prompting me to publish this brief interim report. Paid subscribers are familiar with my Objective Technical Rankings, what follows is an explanation for those who are not.

The Excel spreadsheet below indicates the weekly change in the Technical Ranking (“TR”) of each individual ETF. The technical ranking or scoring system is an entirely quantitative approach that utilizes multiple technical considerations that include but are not limited to trend, momentum, measurements of accumulation/distribution and relative strength. If an individual ETFs technical condition improves the Technical Ranking TR rises and conversely if the technical condition continues to deteriorate the TR falls. The TR of each individual ETF ranges from 0 to 50. The primary take away from this spread sheet should be the trend of the individual TRs either the continued improvement or deterioration, as well as a change in direction. Secondarily, a very low ranking can signal an oversold condition and conversely a continued very high number can be viewed as an overbought condition, but with due warning, over sold conditions can continue at apace and overbought securities that have exhibited extraordinary momentum can easily become more overbought. A sustained trend change needs to unfold in the TR for it to be actionable. The TR of each individual EM ETF in each of the three geographic regions can also reveal comparative relative strength or weakness of the technical condition of the select ETFs in the same region.

Last week The Total EM Technical Ranking or TEMTR rose by +16.69% to 737.5 from 632 the week before marking the fourth week of gains in the TEMTR. The Total Lat/AM EM Ranking rose the most of the three geographic regions by rising 37.7% to 140.5 from 102 two weeks ago. In second place was the Total EMEA EM Technical Ranking which rose 13.4% to 220 from 194. The Total Asia-Pacific EM Ranking rose 12.2% to 377 from 336.

The Total ETF Ranking (“TER”) Indicator is a total of all 20 ETF rankings and can be looked at as a confirmation/divergence indicator as well as an overbought oversold indicator. As a confirmation/divergence tool: If the broader market as measured by the iShares MSCI Emerging Markets Index ETF (EEM) continues to rally without a commensurate move or higher move in the TER the continued rally in the EEM Index becomes increasingly in jeopardy. Conversely, if the EEM continues to print lower lows and there is little change or a building improvement in the TER a positive divergence is registered. This is, in a fashion, is like a traditional A/D Line. As an overbought/oversold indicator: The closer the TER gets to the 1000 level (all 20 ETFs having a TR of 50) “things can’t get much better technically” and a growing number individual ETFs have become “stretched” the more of a chance of a pullback in the EEM. On the flip side the closer to an extreme low “things can’t get much worse technically” and a growing number of ETFs are “washed out technically”, a measurable low is close to being in place and an oversold rally will likely follow. The 13-week exponential moving average, in red, smooths the volatile TER readings and analytically is a better indicator of trend.

After months of non-confirmation of new recovery price highs in the EEM, last week the Total ETF Ranking registered the highest reading since January 2021 and in doing so, marked an unquestionable confirmation of last week’s recovery high from the 2022 lows. What follows is a second Weekly Chart and the technical comments that I made on social media yesterday…

The iShares MSCI Emerging Markets Index Fund or EEM caught a swift kick higher last week! That was thanks in part (see insert) to a sharp rally in the SPDR S&P Emerging Asia/Pacific ETF (GMF) members and in particular Chinese equities (well we all know what that was about) and a turn in the Lat/Am ETFs. Nonetheless the EEM overtook resistance at the 50% Internal Line (violet dashed line) of the Standard Pitchfork (violet P1 through P3) which had capped rally attempts twice before and closed the week just below resistance at the Upper Parallel of the Pitchfork (solid violet line). The EEM may have to retrace a portion of last week’s impulsive 3rd wave rally and even though it is currently overbought it appears that it is on its way to higher price levels and potentially resistance at the $50 level.

To receive the three unabridged ETF Studies that include the Market’s Compass U.S. Index and Sector Study, The Developed Market’s Country ETF Study, and the Emerging Markets Country ETF Study that track the technical condition of over 70 different ETFs and are published every Monday and the Market’s Compass Crypto Sweet Sixteen Study which is published every Sunday, become a paid subscriber at…

The charts are courtesy of Optuma whose charting software enables anyone to visualize any data including my Objective Technical Rankings.

For readers who are unfamiliar with the technical terms or tools referred to in the comments on the technical condition of the EEM can avail themselves of a brief tutorial titled, Tools of Technical Analysis or the Three-Part Pitchfork Papers that is posted on The Markets Compass website…

Listen here or on the go via Apple Podcasts and Spotify

Most investors look at REITs for yield, as bond-like, says Alex Pettee, who discusses the nuances and axioms of investing in the public and private side of real estate investment trusts with Brad Thomas and David Auerbach (1:50). Rates up, REITs down; ignore day-to-day movements (3:30). REIT valuations, property sectors and rate sensitivities (11:30). Common vs preferred shares (14:20). Bullish housing case intact? (16:00) Hurricane effects on real estate (21:00). 3 REITs worth looking at (24:10). This was originally published as a webinar on October 10.

Subscribe to iREIT + HOYA Capital

Transcript

Daniel Snyder: Hey everyone. Daniel Snyder here from Seeking Alpha. We’re going to go ahead and jump into this full hour with a powerhouse panel as you see here today.

We have David, we have Alex, we have Brad Thomas, all joining us from iREIT and Hoya Capital here on Seeking Alpha. I’ll go ahead and hand it off to you, David.

David Auerbach: I’m going to tee it up where, we’ll let Alex briefly give his background. Brad could share a couple of seconds of his background. We’re going to basically start top down, work our way through, go macro to micro.

So, Alex, with that, why don’t you give the folks here a quick 30-second background? Brad, give them a 30-second background, and then, we’ll start jumping right into it.

Alex Pettee: I’ve been writing on Seeking Alpha since 2015 under Hoya Capital. We’ve been focused on REITs. So, we cover every U.S.-listed REIT. There’s about 160 equity REITs, 40 mortgage REITs.

And I think it’s always kind of helpful just to kind of start off with a kind of REIT universe, but we’ll first start with Brad.

Brad Thomas: I’ve been on Seeking Alpha since 2010. Most of you probably know my story, but I’ve been here almost 15 years. I’m at 14 going on 15 years. During that time, I’ve been fortunate to start coverage on many different REITs, many of which have become S&P 500 companies today. We’ve seen a number of M&A transactions. We’ve seen a lot of these small-caps turn into some mid-caps and some big-caps.

So, it’s been great to be on Seeking Alpha and cover the REIT sector. And, again, I’m honored to have Alex and Dave really combine with iREIT. And we’re excited about the opportunities and giving investors the best REIT research really on the planet.

AP: Most investors look to REITs for yield. I think that that’s something we’ve kind of learned over time is that most investors aren’t as interested as us in the on the ground property level trends. It’s an income vehicle and so, REITs have kind of assumed that role as a bond-like vehicle. That comes with pros and cons.

The one negative side of it is the theme of the REIT rate correlation that REITs are very bond-like. REITs are “rates up, REITs down” trend.

And so, we’ll hit on what individual REITs are more rate sensitive, more economically sensitive. We’ll look at sorting REITs by market cap tiers. There’s very wide differences in dividend yield and in balance sheets, in large-cap, mid-cap, small-cap REITs. And then, we’ll hit on some of the trends, like on the private side, how that relates to REITs on the public side.

REITs are really very interesting because it’s the only kind of dual market where there’s a public side and there’s a private side. There’s two different valuations of these assets of the REITs, of the properties held in a REIT structure and on the private side.

And so, that also creates a lot of interesting trends that drive the creation of new REITs through IPOs, through spin-offs, et cetera, or the acquisition of existing REITs.

As of month end, the average equity REIT pays a dividend yield of 3.71%. Average mortgage REIT is north of 10%. One interesting thing here is that this is, of course, the cap-weighted yield, and we’ll go through this in a little bit, but this chart here is the breakdown of yield by cap size.

And you’ll see that large-cap REITs pay that sub-4% yield, but as you go down that cap tier, mid-cap, small-cap, that you do start to see 5%, 6% yields plus.

Dave, how about, like, we’ll kind of kick it off with kind of a “rates up, REITs down” discussion.

DA: Because of that strong employment report that we had last Friday, the acceleration of more Fed rate cuts going to the back half of the year has softened somewhat, maybe 25 basis points going in the rest of the year.

I think another problem that we’re seeing here is that as of this moment right now, the 10-year treasury is at 4.065%. Rates are above 4% for the first time in August. And so, again, with people so interest rate sensitive, yield sensitive, REITs have underperformed this week since the Fed rate cut came out.

And this is my opinion. This does not represent the views of Alex or Brad. When you buy REITs, you got to use 25-, 50-year type of lenses. Ignore the day-to-day movement of what’s going on in the sector. Focus on the year-to-year big picture. And the reason being, REITs are not day-traded vehicles.

If you want to buy a day-traded vehicle, go out and buy one of the hotel REITs because it’s a one-night contract. Then if you want to step it up, then you go into apartments, which are basically six months to one year contracts.

But if you look at the relationship of typical landlord to tenant, it’s five-plus year type of relationships that are in place. So, you can’t focus on the day-to-day headlines when you’ve got to look at things in a very big picture. That’s just my take, Alex.

DS: Can I jump in real quick? Everybody is, of course, reading about the interest rate cutting cycle that we’re in now.

Do you each possibly have an idea of where we’re going? Like, how far down do they continue to cut within the end of next year? Do you follow the dot plot maybe, or how do you calculate when you’re looking forward?

AP: The rate cut expectations, of course, peaked, the Friday after the September rate cut. At that time, the market was pricing in, I believe, about over five cuts for the year. So that would imply the jumbo in September, it was implying a jumbo in November, and then one in December. That’s come back significantly.

We’ve removed, basically, a full jumbo cut from the rate cut expectations. From about 4.85, which was last week, to about four cuts implied by year-end now.

Really since the end of the great financial crisis, REITs have been extremely interest rate sensitive. So from about 2010 or 2011 through COVID, that REITs were essentially trading as bond vehicles. The closest comparison I’d say to REITs is a corporate bond, a kind of a mid-tier corporate bond.

And so that correlation broke down early pandemic, but then really since the start of the Fed’s rate hiking cycle that “rates down, REITs up” or inverse has been a very strong correlation.

A very interesting trend here is that, so REITs were the single worst-performing equity sector from the start of the Fed’s rate hiking cycle, that was March 16, 2022. We’re the worst through this July.

As soon as we got that early pivot, the REIT sector was the best-performing equity sector from July through about last week, and then REITs have since underperformed. The accumulated underperformance peaked in June of this year at 45 percentage points.

Now that’s hugely historic. REITs have historically, on a 10, 15, 20, 25-year basis, basically matched S&P on an annual basis. So to get 45 percentage points of underperformance, that’s very significant.

REITs have outperformed by about 10% to 12%, from July until late September, but now, it’s back to about a 35%, 36% cumulative underperformance gap that REITs have versus S&P since the start of the Fed rate hiking cycle.

So, I think that it’s been a very, very tough couple years for REITs, the rate headwinds have been very strong. And I think the expectation is that same negative force is now positive.

And so it’s still very much at the mercy of the Fed, of market interest rates. I think that the easier path now is lower interest rates, and so that’s huge for the REIT sector.

DS: Thank you for that, Alex. And, Brad, I would love to hear from you because, I mean, you’re the legend, you’ve graciously given us so much time over the years doing all these webinars here on Seeking Alpha.

You had your start in the commercial space, right? You know the commercial side of it. We can go into all the different industries within the sector, but when I hear about interest rates being cut, and you think about, okay, well, they can refinance, and there’s been issues in the commercial space, is there any light at the end of the tunnel for them, if unemployment reports come in okay, job numbers are okay, people continue to spend, GDP continues to grow?

What if we don’t get all these cuts that the market is anticipating?

BT: Sure. Well, again, I think it goes back to not only just REITs, but any stock that would cover a publicly-traded company is we look at the cost of capital as a really big important metric to look for.

And within the REIT sector — again, I was a private developer for 25 years. I’m actually getting back into that business now as well on the private side. And the most of the private developers can’t compete with especially a lot of these big names.

We always talk about Realty Income, which is big popular name on Seeking Alpha, ticker symbol (O), or some of these bigger companies, Mid-America Apartments, ticker (MAA), both A-rated balance sheets.

So, we look at the cost of capital and how these publicly-traded companies have much better access to debt. And I think that’s what we’re really continuing to see.

Again, I’m seeing it now 14, 15 years here on Seeking Alpha, and I think we’ll continue to see a lot of these stronger companies, these blue-chip names, continue to grow their earnings and grow their dividends.

Through all of this, through COVID, even through great recession, we saw a number of these companies that were able to continue increasing dividend. So, I think now with this current setup that I think Alex just outlined, and great job, Alex, with that, I think we’ll continue to see maybe the rate cuts have softened a bit.

But even if they continue to soften, I mean, we’re still seeing those investment spreads. Again, those are the cap rates, minus the cost of capital, those margins continuing to sustain and grow. And so, I think that’s really important.

And the great thing about REITs, and I know we’re going to get into it here in this webinar talking about some sectors that we like, some sectors we don’t like, but the great thing about REITs today, again, as I’ve been on Seeking Alpha now 15 years, is now you have a much broader way to build portfolios and manage your risk. Certain sectors are going to grow quicker than other sectors.

Cell towers, data centers, none of that existed when I was a developer. There’s no way for the individual investor to have access to a data center or cell tower or cannabis REIT or a casino. So, now, there’s so many other opportunities to diversify and really define your risk tolerance levels and build these portfolios.

And again, the game is all about cost to capital and scale. I’ve written about this time and time on Seeking Alpha, but we really like those companies that are able to continue to grow their businesses, see those small-cap companies, we’re going to touch on some of those in a minute, turn to large-cap companies.

I think the setup is really attractive right now. Obviously, sentiment, as Alex just said, the last few years have really been brutal, but, again, we’re starting to see that rally.

And I think, we’ll still continue to have REITs rally, especially, again, those companies that have those wide moat advantages.

DS: David, Alex, maybe you want to start talking us through some of these sectors that we were planning to talk about today?

AP: Some REIT property sectors and even in those property sectors, the individual REITs, there’s a very wide range of rate sensitivity, of economic sensitivity.

What the investor should expect at the property sector level, of what they’re investing in. Is this REIT extremely rate sensitive? Is this a bond-like vehicle, or is this more of an equity stock-like vehicle?

And then also to what degree that these REITs are good inflation hedges. That typically corresponds with rates, but there are some REITs that are not particularly rate sensitive, but are good hedge vehicles.

So, healthcare REITs, very rate sensitive. Storage REITs, very rate sensitive, very bond-like. Where on the other side of it, you have mall REITs, billboards, these are not rate sensitive. And so, I think that from a portfolio management standpoint, what we basically try to do is try to balance these trends, so we’re not making a direct call on interest rates that are not entirely bond-like.

That leads to an interesting discussion on REIT valuations. And so, obviously, what we’ve seen at this REIT rebound since early July, for the first time since about mid-2021, that REITs are now trading at NAV premiums. And this is important from that kind of first point that I talked about in this dual market structure, right?

There’s a private real estate industry, and there’s a public real estate industry. And a lot of the flow between new REIT creations and REITs being acquired is driven by this NAV premium. So, what NAV basically is, it’s: are the real estate assets held by these REITs more valuable in the REIT structure or less valuable in the REIT structure?

When they’re more valuable at the REIT sector level that the flow is into public REITs, that there’s new REITs being created, there’s private entities that are launching REITs. And when this is a NAV discount that the flow is out, that there’s more acquisitions, because you can basically buy the same private property in a REIT structure for cheaper than going out.

And so, yes, what we’ve seen the last couple of years is this net outflow of REITs being taken private. In 2021, there was about 215 REITs. There’s now about 195.

So one interesting factor with REITs is that the valuations play a meaningful role in how REITs actually operate, that the stock price actually matters from an operational standpoint.

And it all ties back to the cost of capital issue, and that REITs actually perform their best when capital is relatively cheaper. So when REITs are trading at discounts, you really don’t get much activity. It’s hard to grow externally.

DS: Some REITs have common versus preferred shares. So the question is, how do you approach which asset class you would kind of choose for any individual REIT?

AP: So we also track all of the REIT preferreds, 174 individual REIT preferred stocks. The average yield on these is about 7.9%, right? So there is a significant yield premium on the REIT preferreds.

BT: Not every REIT, of course, has preferreds. I’ll recommend, and I don’t know about some of those on the team, but I like to have a small percentage of those, kind of as Alex pointed out, as yield enhancers. I like around 10%, 20%, but, again, everybody has got their own risk tolerance level.

And a lot of these companies do have issued preferred, but not all, and there are some really attractive preferreds as well. So, anyway, hopefully, that answers that question.

And there’s actually a couple preferred REIT ETFs that all they do is just invest in REIT preferreds, and that may be another angle as well.

AP: Since 2019, the REIT common has outperformed the REIT preferreds. It definitely is kind of a different type of vehicle. It’s certainly much more yield focused.

Essentially, all of the REIT preferreds are cumulative, and so it’s very rare to kind of have major distribution issues. There have been a handful of cases where the preferred dividend cut as part of a acquisition, right? So, that’d be Cedar (CDR.PR.B) and the Wheeler (WHLR) situation.

But the vast majority of REIT preferreds stayed current on their distribution throughout COVID, and all except, I believe, the Wheeler and the Cedar are now current on their preferreds.

DS: So, I want to go ahead and steer the ship a little to a different industry. Brad, you mentioned cell towers and there’s industrials and data centers and all these other ones, but I think the one that always comes to the top of mind when people talk about real estate is they think about their home.

They think about the consumer. They think about how interest rates are affecting the consumer. So, in the mortgage industry, could you give us a lay of the land and maybe what you’re looking at housing when it comes to maybe even private equity companies are going in there and kind of adjusting some values and things like that, what are we seeing within mortgage, multifamily, and that sort of area?

AP: Yeah, I think that housing theme has always been kind of our major focus. I think that was kind of, like, when we started publishing here in late 2010s, housing was what we saw as the most compelling kind of macro real estate theme.

What was driving this was post great financial crisis, this essentially near shutdown of new construction. So, you saw historically low levels of new construction starting in about 2010, and that kind of built up this significant housing shortage. And I think, in 2018, 2019, that term “housing shortage” was not used often, right? It wasn’t in the daily conversation as it is now.

What we are basically forecasting is that this underbuilding was basically coming in front of this big wave, right? So, I guess, it’s Gen Z or the largest age cohort today is that 30- to 36-year-old age cohort. And so, back in 2018, 2019, we kind of saw this as being the significant catalyst, right? There were this clash of high demand and historically low supply.

And, of course, what we didn’t forecast when we’re making these calls in 2018, 2019 was how COVID would kind of accelerate these trends. And instead of playing out over 10, 15 years, it basically played out in a six month to 18 month time period where you had all this housing demand clashing with this historically low housing supply.

I think that bullish housing case is still intact. And I think that what goes on the housing side, also on the commercial side, it’s all about the supply side is really, I think, where really the area to kind of focus on, right?

The supply takes years and years to kind of build, and in many cases in some property sectors that there’s structural constraints to new supply. On the single family side, of course, there’s zoning, et cetera, that creates these barriers to new supply growth.

And so, those are, I think, if you look at the outperforming commercial sectors you’ll find that the supply theme is really the overriding trend and that the serial outperformers tend to be those not with necessarily high demand, but it’s that supply constraints.

And it’s kind of functioning in that Goldilocks zone where it’s not robust enough that the prices get bid up, that there’s a lot of new construction. But it’s the kind of sectors that are under the radar, so aren’t getting huge supply growth, but can outperform just kind of based on that — those structural trends.

DS: Brad, I wanted to see, do you have a thought about this whole mortgage and, specifically, I mean, the people out there obviously trying to still buy homes. There’s not enough, as he’s mentioned with the supply. I mean, do you see any light at the end of the tunnel here? Is that what keeps the wheel going?

BT: I think, again, there’s a couple angles here. One, and great job, again, Alex, on the mortgage REIT side, again cover residential and commercial mortgages. And the residential REIT side is certainly an interesting sector.

It’s one that – and I’ve wrote about this quite a bit. I’m not a huge fan of residential mortgage REITs. They’re a lot higher levered than equity REITs, and they’re really not suitable – for the large part, they’re not suitable for many retirees, which is a big part of our following, our base.

Not to say you shouldn’t invest in residential mortgage REITs. There’s some really interesting preferreds, which are much safer than the common of the mortgage, set aside.

Now, on the commercial side, I do like that space. I like it for a couple of reasons. One is, it gives us, as a research team, a lot more insight into commercial real estate. I have regular discussions with CEOs and family office investors about commercial real estate.

One of the CEOs that I interview frequently, in fact, maybe this week, I hope, is Brian Harris, who’s the CEO of Ladder Capital (LADR). They’re a specialty mortgage REIT. Brian’s got deep, deep, deep experience in commercial mortgage REITs, and that really has helped us and our team develop strategies around the equity side, because we like to see where is the pain and where are the opportunities, and it’s good to hear from these bankers who really know that space pretty well.

So, I like the mortgage space, but specifically, for me, I like commercial mortgage REITs.

Now, on the equity side, there’s a lot of ways to play it. As I said, we’ve got an evolution of property sectors now, not just apartments. We like apartments and, specifically, I like Sunbelt markets.

Now, that being said, we got another hurricane. My prayers go out to all of you. We just went through a major, major one here in South Carolina, still going to recover, it’s going to take weeks and months.

And there are REITs that own apartments right here in my backyard. Mid-America, for example, 10 communities in the Greenville, Spartanburg, South Carolina market. Now, those appear to be fine, as far as I can tell. We didn’t get hit terribly bad.

But the point I’m trying to make here is, multifamily, not just multifamily REITs, Daniel, but we have the manufactured housing REITs. And, again, I’m worried about some of those portfolios down in Florida.

I mean, Florida is going to get some pretty severe property damage, but there’s a sector that I really like. It’s driven obviously by the aging silver tsunami, like we like to refer to it. So, that’s another angle to play housing, affordable housing. And those are just ground leases, by the way, essentially for the large part. So, that’s one other angle.

You have skilled nursing, is another angle, and senior housing is another angle. So, there’s many ways to play kind of the housing environment. And for me, I really still like the Sunbelt multifamily in Mid-America, Camden Property Trust (CPT). I just wrote on Camden, I believe, yesterday. So, I think those are the kind of angles whether you’re going to be a renter or an owner.

The residential mortgage space, yes, there’s certainly some opportunities, but I’ll lean a little safer. And historically, those companies don’t pay out growing dividends. There is a very volatile dividend environment for the residential mortgage REITs, which is why I’ve kind of shifted from that.

And then, of course, Alex mentioned home builders. I mean, his firm has done a lot of work on the home builder space. They’ve got this ETF called (HOMZ), which invests in the broader housing sector. But these home builders, I mean, Toll Brothers (TOL), Pulte (PHM), I just wrote on those builders yesterday.

Anyway, there are a lot of ways to play it, but I think in the REIT space, again, that’s the opportunity for REITs, because you can really design or customize your portfolio based on your risk tolerance.

But I do think Alex is right, that supply is certainly what you need to watch for, and I think that’s how you’re going to make your money in the residential or the mortgage space.

DS: Thank you so much, Brad. Now, a quick question for you. I know we have three stocks that we’re going to cover here in just a second. We’ll kind of do a little bit of a rapid fire with those.

But there was a question that came through, because we’ve been talking about preferreds. You just mentioned ETFs. Somebody asked, is there an ETF that really just holds those preferred shares that comes to your mind that you really like to keep an eye on?

BT: (PFF) or (PFFA), and Alex, you and I may be thinking the same thing, but those are the two tickers I like.

AP: Yeah.

DS: All right. So, let’s go ahead and dive into these three stocks. Let’s start talking about we’ve been talking about a bunch of different industries and sectors, and these kind of go over three different industries as well, I believe. Brad, this is your article, that I kind of pulled from the iREIT and Hoya service. So, maybe you want to kick us off with the first name?

BT: Talking about small caps. So, I think there’s a great opportunity. Again, we were just talking about rate cuts and even in these small caps, I think, we’ll get more of a boost with these rate cuts.

And so, I’ll just pick the first one, Alpine Net Lease (PINE). Alpine launched by way of another REIT, called — it used to be called Consolidated-Tomoka. I can’t pronounce it. Now they call themselves CTO Realty. They’re also based down in Florida, in Orlando or Daytona Beach. They spun-off their net lease properties.

CTO spun off their net lease properties into another REIT called Alpine Net Lease, and the ticker symbol is PINE. It’s one of the smaller net lease REITs. Many of you know, I love net lease REITs, and I love net lease real estate. I used to build a lot of it.

And it’s just the most boring property sector it is. 15-year long-term leases, modest rent bumps, but it’s a very stable and predictable and reliable property sector. Alpine fits right into that box. They have these long-term net lease properties that are much smaller. Again, they’re a small cap company.

I’ve looked for the company to be acquired. I think it could be potentially a takeover target. I think there’s value. CTO owns a percentage. I can’t remember exactly, but a percentage is of Alpine. So, I think there’s certainly an opportunity for CTO. They’re externally managed as well. So, Alpine is managed by CTO.

I think there’s an opportunity for Alpine to get acquired by a company like Realty Income or maybe Agree Realty, ticker (ADC), or even a private company like Blackstone (BX).

Again, small portfolio, but I think the value there could be unlocked potentially for CTO, the external manager, because they could reinvest that capital at much higher yields than they’ve got within their Alpine portfolio. So I like that name a lot.

DA: Too small for Realty Income. They’re not going to be the buyer. My opinion.

BT: I would say, they’ve obviously, Spirit and VEREIT were two bigger acquisitions by Realty Income, and certainly that hasn’t moved the needle. I think the market has really missed the opportunities.

But, look, Realty Income is the aggregator. Since we’re on that subject, I mean, Realty Income is the aggregator of choice. They’re going to continue to grow that business model, and obviously, they’re entering Europe.

But I would say, Dave, you may be right, but I would say also never say never. I think, they’re still buying smaller portfolios, but given the composition of that Alpine portfolio, you’re probably right. It’s probably more about a private buyer for that portfolio than Agree.

I’ve talked to Joey, the CEO of Agree, quite a bit. I agree with you on that Dave as well. I think Joey probably has no interest in M&A and he hasn’t done a whole lot of M&A. But I do believe Realty Income will continue to be active.

And look, who knows? I mean, they have the ability to do a reverse merger in National Retail Properties, or (NNN) REIT. So, Realty Income has got certainly something nobody else has, which is the ability to transact these very large multibillion-dollar transactions.

DS: Yeah, it seems like they continue to get bigger and bigger every month.

DA: Hey, Daniel, before we can go ahead real quick, I have over 50 questions that we’ve gotten in this conversation today. I’ve taken every single question that’s come in the chat. I’m compiling a list for everybody that’s on this. We are going to answer every single one of these questions.

DS: I think you just earned yourself about 20 more emails right there.

All right, so this next one kind of surprised me. I never really thought about it, but the U.S. Post Office in that angle, what’s this next name, Brad?

BT: Postal Realty (PSTL). Postal is an interesting company. Again, they own one tenant in their portfolio, which is U.S. Postal Service. Look, I don’t know about you, but I think, I still go to the mailbox every day and I don’t pay as many bills through the post office, but I do believe the post office is sustainable.

I think the post office could be utilized better and we should have maybe hunting and fishing licenses at post offices and could increase their business activities. However, that’s a very stable business model, in my opinion.

I don’t think the government is going to let the post office go away anytime soon. I think it’s a bipartisan pick, by the way. And so, I like the post office. I think this is a really interesting category and Dave, there’s another one that actually ties perfectly into something Dave and I’ve been talking about another government pure play kind of government play, but postal is definitely one that we like.

The company has the ability to continue to grow their business model. Having that relationship with the U.S. Postal Service is certainly a competitive advantage. I used to own a few post offices myself, and again, they’re very reliable tenants and typically they don’t close many of these locations. So, I think that’s a great business model. Again, you’re looking at kind of a government-like entity.

So, Dave, I think you had another one. I don’t know if you want to talk about it here, just really quickly on your other government pick.

DA: Yeah, my pick that I seem to like, and I’ve mentioned it at frequent Seeking Alpha events is Easterly Government Properties. The ticker is (DEA). It is not your typical office REIT as it does focus on government agencies, the FBI, your TSA local field offices, Department of Veterans Affairs, et cetera. What’s the word I’m looking for, it has no impact on what’s going on with the election.

If you think about whoever is running, whoever is the President, they are not going to be closing FBI field offices as an example, or TSA is going away anytime soon. So, I mean, I hate to say it, but it’s just a very boring, slow and steady long-term lease type of company that’s very different than every other office REIT that’s out there.

DS: Brad, let’s go with this third one. Why don’t you walk us through it?

BT: The last one is actually, I think, turned into a fairly popular name here on Seeking Alpha, and it’s the cannabis space, and it’s not (IIPR). IIPR is Innovative Industrial Properties.

Interesting fact, that’s the only cannabis REIT listed on the New York Stock Exchange. They were able to get in before the window closed. Got that listing. But you’re not going to see, at least in the short term, any New York Stock Exchange listed cannabis REITs, in my opinion.

NewLake Capital Properties, (OTCQX:NLCP), what they’ve been able to do is go over the counter. The management is talking about other ways to list, but that’s one risk you’re going to take over the counter. Again, they’re smaller cap name. But I like the company a lot, or we like the company a lot. We’ve interviewed the management team quite a bit. They’re certainly experienced.

I got to know this company through one of the Board members. In fact, the Chairman of the Board is Gordon DuGan. Gordon was formerly the CEO of W.P. Carey (WPC), and that’s where I got to know Gordon. He’s got a lot of experience in the net lease space, being at W.P. Carey for as long as he was, and now being involved with NewLake Capital Properties.

So, that company, we believe, has got a really good business model, very low levered company, and we think a pretty sustainable dividend.

Obviously, the cannabis sector is extremely volatile and there’s still fact that there’s no federalization in the space. So, it’s all kind of state by state. We’re seeing a growing number of states still adopt cannabis legislation. Maybe South Carolina at some point will get it, which is probably one of the most conservative states we have here.

But I like NewLake Capital Properties. I think really good management team, really solid fundamentals. Again, there’s risk. It’s over the counter and it’s a cannabis play.