No matter how much most of us would like them too, stocks can’t go straight up forever.

Social media has become a breeding ground for retail investor sentiment, and with it comes a fair share of emotional outbursts. When a stock price dips after a significant run-up, accusations of short selling and dark pool activity are common. That said, it’s crucial to consider a simpler explanation: a healthy pullback.

Imagine this: You buy a stock at $10, and within a month, it skyrockets to $20. Then the stock price dips to $18. Panic sets in, and social media chatter gets louder about potential causes.

Next thing you know, shares are at $14. It’s not the end of the world.

In fact, a pullback after a strong surge is a natural market phenomenon. Here are three reasons why pullbacks happen.

Profit-taking: Those who bought early at lower prices might see this as an opportunity to cash in some profits, leading to a temporary dip in share price.

Valuation Reset: Rapid price increases can sometimes outpace the company’s actual fundamentals. Wall Street generally prefers a slow-and-steady share appreciation as the company continues to strengthen.

Normal Market Fluctuation: The stock market doesn’t move in a straight line. Pullbacks are a normal part of the market cycle, and a healthy correction can actually be a good thing for a stock’s long-term health.

Note that none are anything nefarious. So, before you join the online chorus of conspiracy theories, take a deep breath and consider these facts:

Short sellers are a legitimate part of the market, providing liquidity and potentially identifying overvalued stocks. Their presence doesn’t automatically mean a stock is doomed.

Dark pools exist to facilitate large institutional trades without causing market disruptions. Suspect sometimes, but they’re not inherently negative.

Pullbacks create buying opportunities

GMGI: Case in Point

Golden Matrix Group (NASDAQ: GMGI) is a leading B2B and B2C gaming technology company utilizing proprietary technology and operating globally across 17 regulated markets. GMGI’s B2B division develops and licenses branded gaming platforms for its extensive list of clients. RKings, its B2C division, operates a high-volume eCommerce site enabling end users to enter paid-for competitions on its proprietary platform in authorized markets.

In Mexico, GMGI owns and operates MEXPLAY, a regulated online casino. The company’s global footprint expanded earlier this year with the acquisition of Meridianbet, a well-established B2B and B2C sports betting and gaming platform operating in regulated markets across Europe, Africa and Latin America.

The Meridianbet acquisition has been a catalyst for GMGI’s books and stock price. As detailed in a Form 8-K/A filed with the SEC, in fiscal year 2023, the combined entity achieved total pro forma sales of $137.17 millionand a gross margin of 57%. For the first quarter of 2024, total combined revenue was $36.69 million, with combined gross margin of 57.4%. Combined net income of for Q1 2024 was $2.06 million.

GMGI Chart Responds

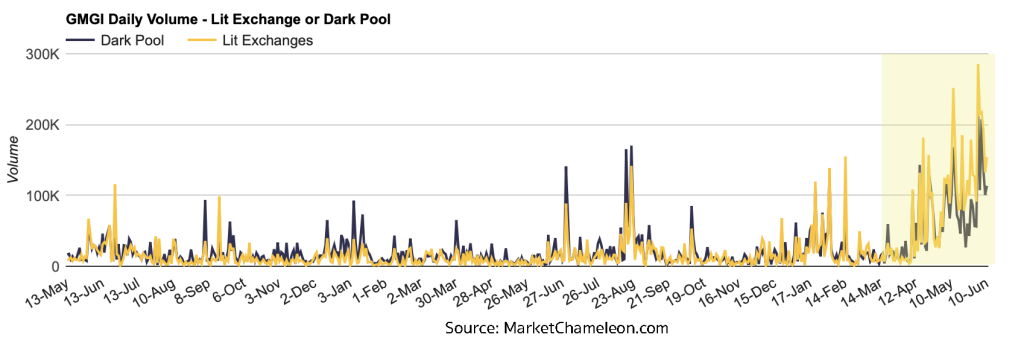

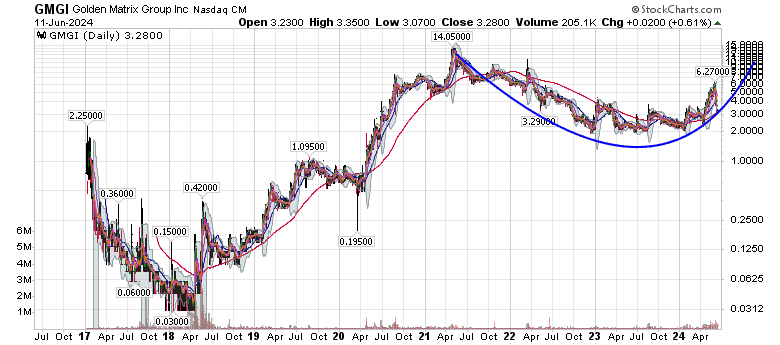

The positive developments were on full display in the GMGI chart as to the positive market response. Notice the pronounced surge in cumulative volume as shares bounced off $2.22 on April 15 to hit a 52-week high at $6.27 on May 31 (+182.4% in six weeks).

Not surprisingly, a sell-off ensued. But was it driven by something greater than natural trading? A look at GMGI dark pool trading on MarketChameleon.com shows no discernible jump in dark pool versus lit trading over the last couple months.

As it happens, dark pool trading is a playground for big money (e.g. hedge funds, institutions). Market Chameleon’s charts show that nearly all trading for GMGI is small and retail traders. This may soon change, as Golden Matrix Group was just added to the Russell 3000 on June 5, which could command the attention of a lot more funds that invest in the popular index.

Then, it must be shorts, right? No. Data on Fintel.io, which pulls its data from NASDAQ, shows GMGI as just 96,868 shares, or less than a day’s worth of trading, short.

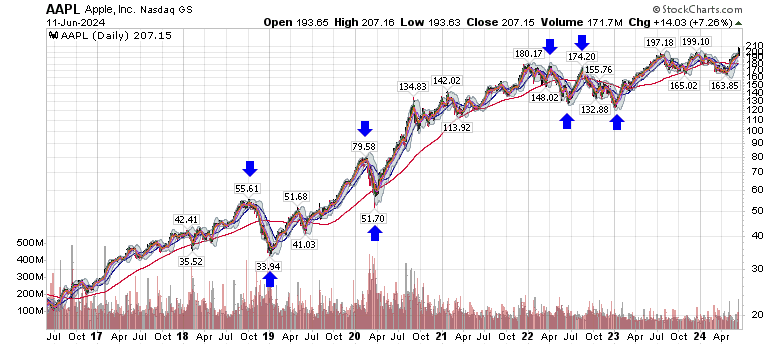

The short answer is that people took the chance to bank some profits as GMGI hit a multi-year high. It happens to every company. Even the mighty Apple (NASDAQ: AAPL) has been chopped substantially during its incredible value creation (and halved many times when you go back to its early years).

Savvy traders use moves up and down to review investment theses, asking if the company’s fundamentals still support the initial investment decision and if the pullback is a chance for dollar-cost averaging.

Focus on the long term: Don’t get caught up in short-term price fluctuations. If you believe in the company’s long-term prospects, a pullback can be a golden opportunity to buy at a discount.

For GMGI, a better question than what was the culprit in the pullback may be if the chart is forming a large cup and handle, a bullish continuation pattern. Technical traders surely noticed in the chart above that shares rebounded off a support level and the 200 day moving average. This is making a third new higher low if it holds.

A smooth climb from here to keep making higher lows and higher highs is what builds a strong chart and reflection of a stock worthy of being part of the Russell 3000.

Successful investing requires discipline and a clear head, not being swayed by noise. Analyze the situation rationally, and remember, sometimes a pullback is just a pullback.

This content is provided by J Ramsdell Consulting (“JRC”), an investor relations consultancy firm specialized in social media management and corporate communications solutions for public and private companies globally. JRC is not a registered broker/dealer or financial advisor and encourages all readers to consult with a qualified professional advisor before making any investment decisions. JRC assumes no responsibility for the investment actions executed by the reader. All content is generated from publicly available information and believed to be accurate. However, the accuracy or completeness of the information is only as reliable as the sources they were obtained from. All materials created by JRC and released to the public via distribution services, social media, website, or any other means of transmission are not to be regarded as investment advice or a solicitation to buy or sell securities and are exclusively for informative purposes only. JRC has been compensated by GMGI for investor relations services, including occasionally creating and managing content, which inherently creates a conflict of interest in JRC’s ability to remain objective in communication regarding the client company. Furthermore, this article contains forward-looking statements, particularly as related to the business plans of the client company, within the meaning of Section 27A of the Securities Act of 1933 and Sections 21E of the Securities Exchange Act of 1934 and are subject to the safe harbor created by these sections.

A federal appeals panel has temporarily halted two permits needed to begin construction on a pipeline project in Tennessee that will supply a natural gas plant.

In a split 2-1 decision, the 6th U.S. Circuit Court of Appeals panel delivered a ruling Friday that, for now, prevents Tennessee Gas Pipeline Company LLC from starting to build its 32-mile (50-kilometer) pipeline through Dickson, Houston and Stewart counties.

The project would fuel the Tennessee Valley Authority’s combined-cycle natural gas facility at the site of the coal-fired Cumberland Fossil Plant that is being retired.

Tennessee Gas Pipeline Company could have begun construction as soon as Tuesday, according to the court records.

TVA, meanwhile, plans to mothball its two-unit coal plant in two stages — one, by the end of 2026, to be replaced the same year by the 1,450-megawatt natural gas plant; and the second, shuttered by the end of 2028, with options still open on its replacement.

“This pause is a crucial opportunity to rethink the risks of fossil fuel development and prioritize the health and environment of Cumberland and our region,” said Emily Sherwood, a Sierra Club senior campaign organizer, in a news release Monday.

TVA’s plans to open more natural gas plants have angered advocates who want a quick redirection away from fossil fuels and into solar and other renewables, as TVA plans to retire its entire coal fleet by the mid-2030s.

The case is set for oral arguments on Dec. 10. If additional appeals are filed and succeed, the timeline could be reset again.

“We do not agree with the court’s temporary stay and are evaluating our options to ensure this project can be constructed in a timely manner,” the pipeline firm’s parent company, Kinder Morgan, said in a statement Monday.

Spokespeople for the Tennessee Valley Authority and the Army Corps of Engineers declined to comment. Chad Kubis, a spokesperson for the state attorney general’s office, said officials there are evaluating their next steps.

The Southern Environmental Law Center and Appalachian Mountain Advocates, on behalf of Appalachian Voices and the Sierra Club, asked the appeals court in August 2023 to reconsider a water quality permit issued by the Tennessee Department of Environment and Conservation for the pipeline. In September, the groups requested an appellate review of another permit from the U.S. Army Corps of Engineers.

In the ruling, Judges Eric Clay and Karen Moore argued that the groups risk irreparable harm if pipeline construction begins before the judges decide their case. The company’s plans would cross scores of streams and wetlands, where construction could do long-lasting damage to waterways and wildlife, the plaintiffs contend.

Judge Amul R. Thapar, in dissent, contended the court lacks jurisdiction for the state agency claim, and that the plaintiffs haven’t shown they would suffer irreparable harm or that their case would likely succeed.

TVA’s plans for expanding its natural gas fleet have drawn additional lawsuits, including over the Federal Energy Regulatory Commission’s approval of the Cumberland pipeline.

Another lawsuit claims that TVA’s environmental review of the Cumberland plant was perfunctory, in violation of the law. A separate challenge contests the decision-making for a planned 1,500-megawatt natural gas facility with 4 megawatts of solar and 100 megawatts of battery storage at the Kingston Fossil Plant, the site of a massive 2008 coal ash spill. Late last month, a judge dismissed a different lawsuit that challenged TVA’s process to approve plans for gas turbines at a retired coal plant in New Johnsonville.

The groups suing over gas expansion plans note that TVA is off track to meet the Biden administration’s goal of eliminating carbon pollution from power plants by 2035 to try to limit the effects of climate change, even with a majority of the board appointed by President Joe Biden. Several of TVA’s proposals for new natural gas plants have prompted criticism from the U.S. Environmental Protection Agency, including a warning that its environmental review of the Kingston project doesn’t comply with federal law.

TVA CEO Jeff Lyash has said repeatedly that gas is needed because it can provide power regardless of whether the sun is shining or the wind is blowing. He added that it will improve on emissions from coal and provide the flexibility needed to add 10,000 megawatts of solar to its overall system by 2035. TVA has a goal of 80% reduction in carbon emissions by 2035 over 2005 levels and net-zero emissions by 2050.

TVA provides power to 10 million people across seven Southern states.

If you’re thinking about moving to Maryland, bustling cities like Baltimore or Frederick might come to mind. However, this state has much more to offer. From quaint downtowns to festivals that bring the community together, Maryland’s small towns are perfect for anyone looking to experience what life is like in its quieter corners. In this Redfin article, we’ll discuss 11 charming small towns in Maryland, each with their own unique character and plenty of reasons to call home.

1. Easton, MD

Median Sale Price: $400,000 Homes for sale in Easton | Apartments for rent in Easton

Easton, located on Maryland’s Eastern Shore, is known for its history, arts scene, and scenic charm. Every November, the town hosts the Waterfowl Festival. An event that celebrates the region’s hunting and conservation heritage with art exhibits, dog trials, and delicious local food. Easton is also home to the Avalon Theatre, a restored venue that has national and local performers for concerts and events throughout the year. With the Tred Avon River nearby, locals enjoy kayaking, sailing, or simply relaxing by the water on sunny afternoons.

2. Elkton, MD

Median Sale Price: $342,000 Homes for sale in Elkton | Apartments for rent in Elkton

Elkton has a unique history as the “Marriage Capital” during the early 20th century. This is because couples would travel here to get married without waiting periods. Today, the town honors that legacy with historical sites like the Elkton Municipal Building, which once served as the popular wedding venue. The nearby Elk River offers plenty of outdoor fun, with locals enjoying boating, fishing, and waterfront picnics at Elk Neck State Park.

3. Chestertown, MD

Median Sale Price: $412,000 Homes for sale in Chestertown | Apartments for rent in Chestertown

Chestertown, sitting along the Chester River, is a picturesque town with a strong colonial past. Every Memorial Day weekend, the town comes alive with the Chestertown Tea Party Festival. This festival includes a reenactment of its colonial protest against British taxation, complete with a parade, boat race, and craft market. Strolling through the historic district, visitors can explore well-preserved 18th-century homes, quaint shops, and several art galleries. The Chester River is a favorite among locals for sailing, paddleboarding, sunset cruises, and of course, fishing.

4. La Plata, MD

Median Sale Price: $420,500 Homes for sale in La Plata | Apartments for rent in La Plata

La Plata is a quiet town in Southern Maryland. Each April, locals come together for the Celebrate La Plata festival, enjoying live entertainment, crafts, and a glimpse into the town’s past. The town’s heritage is on display at the La Plata Train Station Museum, where you can learn about its history as a key rail stop. La Plata is also known for scenic trails and parks, such as Tilghman Lake, where people spend weekends hiking, fishing, and picnicking.

5. Denton, MD

Median Sale Price: $344,000 Homes for sale in Denton | Apartments for rent in Denton

Denton is located along the Choptank River on Maryland’s Eastern Shore. The town hosts the annual Caroline Summerfest, a lively event featuring live music, street performers, and fireworks. Nature enthusiasts enjoy kayaking along the Choptank or exploring Martinak State Park, a serene spot for camping, hiking, and fishing. Downtown Denton features a variety of locally owned shops and cafes, like the Market Street Public House, known for its friendly atmosphere and pub fare.

6. Leonardtown, MD

Median Sale Price: $430,000 Homes for sale in Leonardtown | Apartments for rent in Leonardtown

As the county seat of St. Mary’s County, Leonardtown’s square is a hub for community events. Popular events including the annual Earth Day celebration and Taste of St. Mary’s food festival. Leonardtown Wharf Park is a favorite among locals with scenic waterfront views and opportunities for kayaking or paddleboarding on Breton Bay. The town also has a great arts scene, with galleries and studios showcasing local talent, especially during First Fridays, when shops and restaurants stay open late.

7. Princess Anne, MD

Median Sale Price: $235,000 Homes for sale in Princess Anne | Apartments for rent in Princess Anne

Princess Anne’s downtown district is home to beautifully preserved 18th- and 19th-century buildings, including the iconic Teackle Mansion, which offers tours and seasonal events. Each year, locals celebrate their heritage with events like the Somerset County Fair, showcasing local agriculture and crafts. Residents enjoy relaxing at the Janes Island State Park, a short drive away, where fishing, boating, and camping are favorite pastimes.

8. Berlin, MD

Median Sale Price: $351,000 Homes for sale in Berlin | Apartments for rent in Berlin

Berlin, located just minutes from Ocean City, is a small town with a reputation for unique events and artistic flair. Named “America’s Coolest Small Town” in 2014, Berlin lives up to its title with a lively downtown filled with art galleries, boutique shops, and locally loved eateries like the Blacksmith Bar & Restaurant. Additionally, movie buffs will appreciate that Berlin served as the filming location for the films Runaway Bride and Tuck Everlasting.

9. Pocomoke City, MD

Median Sale Price: $235,000 Homes for sale in Pocomoke City | Apartments for rent in Pocomoke City

Known as the “Friendliest Town on the Eastern Shore,” Pocomoke City is known for its welcoming atmosphere. Visitors love the Delmarva Discovery Museum, where exhibits highlight the ecology and history of the region, along with interactive aquariums featuring local wildlife. Pocomoke River State Park offers plenty of outdoor fun, with scenic trails, kayaking, and fishing opportunities. The downtown area is home to the Mar-Va Theater, a beautifully restored art deco venue that hosts live performances and community events.

10. Manchester, MD

Median Sale Price: $517,500 Homes for sale in Manchester | Apartments for rent in Manchester

Manchester is located in the northern part of Carroll County. The town celebrates its German heritage every summer with the Manchester Volunteer Fire Department Carnival, featuring rides, live music, and homemade food. Manchester is also known for its scenic countryside, with rolling hills and family-owned farms adding to the landscape. With a tight-knit community and proximity to both Baltimore and Gettysburg, Manchester has the perfect balance of rural living and easy access to urban amenities.

11. Hampstead, MD

Median Sale Price: $407,500 Homes for sale in Hampstead | Apartments for rent in Hampstead

One of the Hampstead’s most beloved events is the Hampstead Day Festival, held every spring, featuring local vendors, food trucks, and live music. History buffs can explore the Hampstead Train Station, a small museum showcasing the town’s railroad past. Residents enjoy outdoor activities at Panther Park, with walking trails, sports fields, and playgrounds perfect for group outings.

Methodology: The median home sale price and average monthly rental data is from the Redfin Data Center.

I have spent the last week reading “Shoe Dog”, Phil Knight’s memoir of how a runner on the Oregon University track team built one of the great shoe companies in the world, in Nike. In addition to its entertainment value, and it is a fun book to read, I read it for two storylines. The first is the time, effort and grit that it took to build a business, in a world where risk capital was more difficult to access than it has been in this century, and in a business where scaling up posed significant challenges. The second is the building of a brand name, with a mix of happy accidents (from the naming of the company to the creation of the swoosh as the company’s symbol to its choice of slogan), good timing and great merchandising all playing a role in creating one of the great brand names in apparel and footwear. The latter assessment led a more general consideration of what constitutes a brand name, what makes a brand name valuable and what causes brand name values to deplete and disappear. Of course, since my attention was drawn to Nike in the first place, because of a change at the top the company and talk of brand name malaise, I tried my hand at valuing Nike in 2024, along the way.

Brand Name – What is it?

The broadest definition of a brand name is that it is recognized (by employees, consumers and the market) and remembered, either because of familiarity (because of brand name longevity) or association (with advertising or a celebrity). That definition, though, is not particularly useful since remembering or recognizing a brand, by itself, tells you nothing about its value. After all, almost everyone has heard or recognizes AT&T as a brand/corporate name, but as someone who is a cell service and internet customer of AT&T, I can assure you that neither of those choices were driven by brand name. The essence of brand name value is that the recognition or remembrance of a brand name changes how people behave in its presence. With customers, brand name recognition can manifest itself in buying choices (affecting revenues and revenue growth) or willingness to pay a higher price (higher profit margins). With capital providers, it may allow for lower funding costs, with equity investors pricing equity higher and lenders accepting lower interest rates and/or fewer lending covenants. For the moment, this may seem abstract and subjective, but in the next section, we will flesh out brand name effects on operating metrics and value more explicitly.

Corporate, Product and Personal Brand Names

Brand names can attach to entire companies, to particular products or brands, or even to personnel and people. With a company like Coca Cola, it is the corporate brand name that has the most power, but the soft drink beverages marketed by the company (Coca Cola, Fanta, Sprite, Dasani etc.) each have their own brand names. With companies like Unilever, the corporate brand name takes a back seat to the brands names of the dozens of products controlled by the company, which include Dove (soap), Axe (deodorant), Hellman’s (mayonnaise) and Close-up (toothpaste), just to name a few. There are clearly cases of people with significant brand name value, in sports (Ohtani in baseball, Messi in soccer, Kohli in cricket) and entertainment (Taylor Swift, Beyonce), with a spill over to the entities that attach themselves to these people. In fact, a critical component of Nike’s brand name was put in place in 1984, when the company signed on Michael Jordan, in his rookie season as a basketball player, and reaped benefits as he became the sport’s biggest star over the next decade.

Brand names and other Competitive Advantages

One reason that brand name discussions often lose their focus is that companies are quick to bundle a host of competitive advantages, each of which may be valuable, in the brand name grouping. The table below, where I have loosely borrowed from Morningstar and Michael Porter is one way to think about both the types and sustainability of competitive advantages:

Companies like Walmart and Aramco have significant competitive advantages, but I don’t think brand name is on the top five list. Walmart’s strengths come from immense economies of scale and bargaining power with suppliers, and Aramco’s value derives from massive oil reserves, with far lower costs of extraction, than any of its competitors. Google and Facebook control the advertising business, because they have huge networking benefits, i.e., they become more attractive destinations for advertisers as they get bigger, explaining why they were so quick to change their corporate names, and why it has had so little effect on value. The pharmaceutical companies have some brand name value, but a bigger portion of their value added comes from the protection against competition they get from owning patents. While this may seem like splitting hairs, since all competitive advantages find their way into the bottom line (higher earnings or lower risk), a company that mistakes where its competitive advantages come from risks losing those advantages.

Brand Name Value

At the risk of drawing backlash from marketing experts and brand name consultants, I will start with my “narrow” definition of brand name. In arriving at this definition, I will fall back on a structure where I connect the value of a business to key drivers, and look at how brand name will affect these drivers:

Put simply, brand name value can show up in almost every input, with a more recognizable (and respected) brand name leading to more sales (higher revenues and revenue growth), more pricing power (higher margins), and perhaps even less reinvestment and less risk (lower costs of capital and failure risk). That said, the strongest impact of brand name is on pricing power, with brand name in its purest form allowing it’s owner to charge a higher price for a product or service than a competitor could charge for an identical offering. To illustrate, I walked over to my neighborhood pharmacy, and compared the prices of an over-the-counter pain killer (acetaminophen), in its branded form (Tylenol) and its generic version (CVS) :

The ingredients, in case you are wondering, are exactly the same, leading to the interesting question, more psychological than financial, of why anyone would pay an extra $2.50 for a product with no differentiating features. If you are wondering how this plays out at the business level, the operating margins of pharmaceutical companies that own the “brand names” are significantly higher than the brand names of companies that make just the generic substitutes.

The Tylenol example also serves to illustrate when it is easiest to value brand name, i.e., when it is the only competitive advantage, and when it will become difficult to do, i.e., when it has many competitive advantages. It is for that reason that valuing brand name is easier to do at a beverage or cereal company, such as Coca Cola or Kellogg’s, where there is little to differentiate across products other than brand name, and you can attribute the higher margins almost entirely to brand name. It is at the basis for my valuation of Coca Cola’s brand name in the picture below, where I value the company with its current operating margin:

Note that while the company comes in as slightly overvalued, it is still given a value of $281.15 billion, with much of that value coming from its pre-tax operating margin of 29.73%. We estimate the value of Coca Cola’s brand name in two steps, first comparing to a weighted average margin off 16.75% for soft-drink beverage companies, where many of the largest companies are themselves branded (Pepsi, Dr. Pepper etc.), albeit with less pricing power than Coca Coal and then comparing to the median operating margin of 6.92%, skewed towards smaller and generic beverage companies listed globally: This is undoubtedly simplistic, since it assumes that the brand name value shows up entirely in the margin, and it likely understates the value of Coca Cola’s brand name. That said, valuing Coca Cola at the median beverage company margin yields a value of $51 billion, suggesting that 82% of the company’s intrinsic value comes from its brand name. Comparing to other beverage company and valuing at the weighted average operating margin still yields a differential brand value of $131.4 billion for Coca Cola, indicating that having a premium brand name has significant value.

Brand names become more difficult to isolate and value, when a company has multiple competitive advantages, since the higher margins or growth or returns on capital will reflect the composite effect of all of the advantages. With companies like Apple, where brand name is a factor, as is a proprietary operating system, a superior styling and a unique app ecosystem, the higher margin can be attributed to a multitude of factors, making it more difficult, perhaps even impossible, to isolate the brand name value. When valuing Birkenstock, at the time of its IPO, I wrestled with this problem, and with the help of a series of assumptions along the way, did find a way to break the value of the four intangibles that I saw in the company: a world-recognized brand name, a quality management team, free celebrity advertising and the buzz created by Margot Robbie wearing pink Birkenstock in the Barbie movie.

The pricing premium effect of brand name also becomes an effective device to strip companies that hold on to the delusion that their brand name values have value, long after they have lost their shine. If a company has margins that trail that of other companies in its industry grouping, it has lost brand name bragging rights (and value), and it is time to either accept that reality or rebrand to acquire pricing power again. Applying this test, you will find that nine out of ten companies that claim to have brand values have really nothing to show for that claim.

Nike, in my view, falls somewhere between the two extremes. It is not as pure a brand play as Coca Cola, since athletic footwear, in particular, has physical differentiation that may lead some to prefer one brand over another. At the same time, it is not as complex as Apple, insofar as even a Nike aficionado can find a relatively close substitute in another brand. To measure how Nike’s brand name has played out in its operating metrics, we compared the company’s operating margins to the weighted operating margin of the two businesses (two thirds footwear and one third apparel) that Nike has operated in for much of the last two decades:

Other than 2023, Nike has consistently earned a higher operating margin (1.5% to 3% higher) than the rest of the industry, and since much of this industry is composed of brand name companies, it would suggest that Nike has a premium brand name, not surprisingly. If you are a Nike-pessimist, though, the drop off in the margin differential in the last five years is troubling, but almost all of that drop can be attributed to the company’s troubles in 2023. Clearly, the company is taking the decline seriously, bringing back a Nike employee of long standing in Elliott Hill to replace John Donahoe, who cut his teeth in tech companies (ServiceNow, eBay and PayPal).

I valued Nike, using its compounded annual growth rate and average operating margin over three period – 2014-2108, 2019-2023 and just the last twelve months:

You can see why Nike acted swiftly to change its CEO, since its value will dip substantially, if its growth stays down and margins do not bounce back. At the $71 stock price that the stock was trading at, just six weeks ago, the investing odds would have been in your favor, but the bounce back in the stock price to $88, after the new CEO hire, suggests that the market is pricing in the expectation that the company will bounce back to higher growth and better margins.

Brand Name Creation

Brand name does add value, if it gives the company that owns it pricing power, but how does a company end up with a valuable brand name? There are facile answers and they include longevity, with long-lived companies having more recognizable brand names, and advertising, where more spending is assumed to result in a more valuable brand name. To see why I attach the “facile” prefix to these answers, consider again the example of AT&T, a company that has been around for more than a century and remains one of the ten largest spenders on advertising in the United States. None of that spending has translated into a significant brand name value, thought there may other benefits that the company accrues.

I am sure that someone who immerses themselves in in this topic, perhaps in marketing and advertising, may be able to provide a deeper answer, but here is what I see as ingredients that go into developing a valuable brand name:

Attachment to an emotional factor/need: As marketing has recognized through the ages, the key to a powerful brand name is a tie to a human emotion. Rational or not, consumers may reach for a branded product, because they associate the product with freedom, reliability, happiness, patriotism or aspiration, if that association exists in their minds. The challenge, of course, is to find an emotion that attaches well to your product, either because of its history or its make-up, but the association, once made, can be powerful and long-lasting.

Celebrity connection: Earlier, we talked about personal brand names, and argued that Nike benefited from its association with Michael Jordan, in building its brand name. In fact, Apple (in its streaming service) and Major League Soccer benefited mightily from Lionel Messi playing Inter Miami, with the former adding hundreds of thousands of subscribers to it soccer streaming service, and the latter increasing attendance in stadiums around the country. Here again, there are perils, since attaching a brand name to a person also exposes the company to the failings and foibles of that person, as Nike found out in its associations with both Tiger Woods and Colin Kaepernick.

Fortuitous events/ choices: There is a third factor that is not covered in most brand name management classes, and for good reason, and that is the effect of luck. In an alternate universe, Phil Knight might have stayed with Dimension Six, his initial choice for the company name, picked a different symbol than the swoosh (for which Nike paid $35 to the designer) and even a different slogan ( than the “Just do it” picked by the advertising team), and the end result could have been very different.

Advertising: While there may be little or no link between overall advertising spending and brand name, it is undeniable that there are ads that catch people’s attention and alter perceptions of a product. I was an Apple user already in 1984, when it ran its famous 1984 ad during the Super Bowl, setting itself apart from the PC makers, and while that ad yielded little monetary benefit to Apple in the immediate aftermath, it contributed to creating the brand name that now allows the company to charge $1600 for a new smart phone. Nike has had its share of iconic commercials, and I still remember this Nike ad, with Michael Jordan, from 1997, showing how long the shelf life can be for a great ad.

If asked to advice a company that was intent on creating a brand name, my suggestion would be to start with a product or service that is differentiated from the competition, and to give the brand name time to build around that differentiation. That may require sacrifices on scaling up (accepting less growth to preserve the product differential), a higher cost structure (if it is a quality difference) and perhaps even more reinvestment, but trade offs are inherent to almost everything of value in business. If the expected costs of building a brand name exceed its benefits, though, it may be worth asking whether brand name is the competitive advantage that the company should be aspiring for, since there are other competitive advantages that can add as much or much more value in the business the company operates in.

Brand Name Destruction

The benefit of building a strong brand name is that it remains one of the most sustainable competitive advantages in business, with the advantages often lasting decades. However, even brand names eventually lose their luster, but the reasons they do so vary:

Aging brand/consumer base: In my posts and book on corporate life cycle, I talk about how and why companies age, and how aging is inevitable. The same can be said of brand names, since even the most highly regarded brand names eventually age, and no matter how much managers try to resurrect them, they never recover their mojo. When valuing Kraft Heinz in 2015, when the most venerable name in value investing (Warren Buffett) teamed up with one of the shrewdest players in private equity (3G Capital) to buy the company because it was under valued, I wondered whether the reason the market was turning down on the company was because the portion of the population that were drawn to the company’s products (fifty seven types of ketchup, all of which taste bad, and cheese that stays liquid through a nuclear winter) to be tasty was getting smaller and older. In hindsight, it is clear that Kraft Heinz will not reclaim its former glory, because its products and customer base have aged.

Benign neglect: Brand names may provide sustainable competitive advantages, but only if they are cared for and maintained. There are legendary brand names that have been neglected, treated as cash cows with no new investment or sprucing up needed, and have faded in value. Quaker Oats, a longstanding mainstay of the US cereal business, not only allowed itself to pushed to the sidelines by aggressive cereal companies, but failed to take advantage of the rise in demand for oatmeal as a heart-healthy substitute.

Cultural changes: There are products and services that have lost their allure over time, because the cultural mores or social norms of the consumers have changed. If you binge watch Mad Men, the television series about advertising in the 1960s, you should not be surprised to see ads for products and services that you would now view in a very different light.

Changing tastes: There are some businesses, where the demand for products is transient and fad-driven, and new brands replace old ones, as tastes shift. This has generally been the case with apparel retail in the United States, with the Gap’s reign at the top lasting about a decade, with newer and cooler retail brands like Abercrombie and Fitch and Tommy Hilfiger replacing them, and then were themselves being displaced by H&M and Uniqlo.

Toxic connections: A brand name that is built up over time can sometimes very quickly fall back to earth, if the company or its personnel bring toxic connections. Abercrombie and Fitch, for instance, which became a hot destination for the young in the first decade of this century, found its brand name devastated by accusations of racism and sexism in its ranks.

Brand overreach: There are cases where a company with a valuable brand name may dilute or even destroy that brand name by overreaching, and putting it on products that cut agains the brand name narrative. A good argument can be made that Disney, usually masterful at managing its brands, diluted the value of both its Avengers and Star Wars franchises by rushing headlong into the streaming business, with new series.

While all of these forces can cause a once valuable brand name to lose its value, it is worth noting that there are companies that have redeemed brand name value, sometimes by remaking the product or service, sometimes by repackaging it and sometimes by repositioning it. Crocs, whose brand name soared in the 2000s, but crashed by the end of the decade, repackaged itself around celebrity endorsements to become a successful brand again. Lego, a venerable brand name in the toy business, sold off its theme parks, and refocused attention on its core product, while redirecting its offerings to adults. In general, though, reincarnating a brand becomes easier for niche brands than for mass market ones, for product brands than for company brands, and for younger brands than for older ones.

I believe that 2023 was a wake up call for Nike, as it awoke multiple disruptions. First, in the post-COVID years, Nike moved from store sales to digital sales, with Nike Digital, accounting for almost 43% of revenues in 2022. While that shift does reflect a change in consumer preferences towards shopping online, there is a question of whether bypassing shoe stores, which over the decades have contributed to the Nike brand, by highlighting their most iconic shoes, has undercut the brand. Second, while the footwear business has been more resistant to fads than the apparel business, Nike;’s mass market strategy of being all things to all people is exposing it to disruption. The company is losing market share, especially among younger customers, to newcomers in the space like On and Hoka, and among runners (Nike’s original core market) to older companies like New Balance that have rediscovered their mojo. Third, in an age where celebrities come with problems, and politics divides us on even the most trivial of issues, Nike’s celebrity-driven advertising campaigns may hurt more than help the company. In short, Nike’s new CEO has his work cut out for him!

We recently had an exciting discussion with Abhishek Gupta, Chief Marketing Officer, Edelweiss Life Insurance, on customer-centric evolution in life insurance in this digital age. As the chief brand champion, Abhishek manages the reputation of the company by promoting its diverse and innovative range of product offerings and services.

Watch Video

Leveraging the power of storytelling and creativity, Abhishek aspires to deliver inclusive and strategic communications that can make the brand stand out as a new-age life insurer. Helming a team of ambitious and creative minds, Abhishek has been harnessing the company’s product innovations and superior customer experience to set advertising benchmarks in the industry. He also leads the Customer Experience strategies for the company and strives to build a differentiated brand experience that can foster customer trust and advocacy.

Abhishek has been with the Edelweiss Group for 8+ years. With experience spanning 24 years, he has worked with brands across several sectors over the years – The Mobile Store, Walmart India (Bharti Retail), Spencer Retail, ICICI Bank and Shopper’s Stop.

An engineer with a post-graduation degree in marketing, Abhishek has been recognized as one of the ‘25 Most Outstanding Marketing Professional of India at World Brand Congress 2014’, ‘Most Influential Marketing Leaders 2017’, and ‘Global Marketing Leaders 2019’ at World Marketing Congress, ‘CMO Transformation Award’ at the Pitch CMO Awards 2023 and ‘Financial Express Visionary Leader Recognition’ at Modern BFSI Summit 2023.

The main insights from the discussion are given below:

Customer-Centric Evolution: Reimagining Life Insurance in a Digital Era

1. What would be your assessment of the current state of the life insurance industry? And your take on the emerging trends or shifts in consumer behaviour?

Life insurance is a fundamental financial instrument, forming the base of your savings and investment pyramid. Once you protect yourself, you can start building and growing your wealth. Life insurance ensures you’re prepared for unforeseen events, especially if the primary earner is absent.

Unfortunately, many Indians don’t see life insurance this way. Insurance is often viewed negatively, with decisions delayed and mistrust prevalent. These factors have turned life insurance from a pull product into a push product.

It’s unusual for someone to proactively seek life insurance. People typically only consider it under two specific circumstances:

The most common scenario for buying life insurance is when approached by an advisor, such as an agent, bank relationship manager, acquaintance, broker, or financial planner

The second scenario involves a trigger event, like marriage, having children, or witnessing a friend or family member’s loss. These events highlight the need for income continuity

On the supply side, the Indian life insurance industry is dominated by LIC, a government-owned company. Despite the privatization of the industry in 2000, LIC maintains a significant market share. The market is highly polarized, with LIC and a few private insurers controlling the majority of the business. This competitiveness, coupled with consumer reluctance and the importance of distributors, makes life insurance a heavily pushed product.

India faces a significant protection gap due to underinsurance rather than low penetration. People often buy insurance without realizing that it needs to be adjusted for rising income and changing life circumstances. As income increases, insurance coverage should be upgraded to maintain adequate income replacement. Many people have only 50-60% of the coverage they actually need, leaving them underinsured.

Coming to consumer behaviour shifts in insurance, it typically remains stable unless a major event, like COVID-19, occurs. Such events can dramatically shift consumer attitudes and behaviours.

COVID-19 significantly altered consumer behavior in 7 key ways: 1. Family became paramount 2. Self-reliance increased 3. Saving and investing habits improved 4. Appreciation for non-material things grew 5. Social responsibility increased 6. A sense of vulnerability emerged 7. Health became a priority

While these shifts were notable during COVID, pre-pandemic behaviors have gradually returned. Many consumers have returned to pre-pandemic habits.

2. How has marketing changed in the last decade? What has changed and what has remained the same?

Regarding the evolution of marketing, traditional approaches focused on broad-based campaigns with uncertain effectiveness. Digital marketing has introduced measurability and immediate results, but it’s essential to remember that brand building is a long-term process.

Effective marketing requires a balance between immediate results and long-term brand building. A focus on short-term metrics has led to a decline in memorable campaigns and an overemphasis on attribution models that ignore the overall customer journey.

To address this, marketers should prioritize long-term brand building and develop comprehensive measurement or frameworks that include awareness and consideration.

In terms of customer experience, significant progress has been made in moving from product-centric to experience-centric approaches. By focusing on delivering a consistent and delightful customer experience across all touchpoints, organizations can build strong brands and foster customer loyalty.

3. How critical is personalization in the life insurance industry? How do you do it while adhering to privacy regulations?

Personalization is essential for building customer relationships, but it can be challenging in low-touch industries like insurance.

Insurance companies often create opportunities for interaction, such as policy anniversary dates and festivals, to personalize communications. Data enrichment is crucial for effective personalization. While traditional data collection methods provide some information, companies need to continuously update customer data to reflect life stage changes.

Face-to-face interactions are invaluable for building trust and understanding customer needs, especially in the context of insurance. Digital sales in the insurance industry are still relatively limited, with intermediaries playing a crucial role in most transactions.

Personalization is essential for intermediaries as they represent multiple insurers. Companies often create personalized solutions for intermediaries, who can then offer them to customers. Data enrichment is key to providing personalized customer experiences. We created a tool like “You Unlimited” that can help advisors recommend products based on individual needs and financial capabilities.

By offering tailored solutions at different life stages, insurers can build stronger relationships with customers and increase sales.

4. What is your framework to understand the big shift towards AI in the industry? Any ethical considerations you have keeping in mind the nature of the product?

AI has broad applications in the insurance industry, beyond marketing. In particular, AI can help with:

Customer retention: Identifying at-risk customers and targeting retention efforts accordingly

Fraud detection: Analyzing data to identify suspicious claims

Advisor management: Identifying top-performing advisors and investing in their development

Content creation and vernacularization

While image generation is still under development, AI has been effective in generating content in multiple Indian languages.

5. What are the key priorities for Edelweiss and Life Insurance companies in general in terms of innovation and customer engagement?

Distribution is crucial for the success of the insurance industry, yet it often receives insufficient attention.

Companies should focus on improving the distributor experience, as distributors are key to reaching customers. There is a significant opportunity to educate customers about insurance and offer innovative solutions. However, challenger brands face the challenge of competing with established players and must invest in education and customer acquisition.

By Bijoy K.B | Associate Director – Marketing at Lemnisk

It’s not exactly groundbreaking news to say kids are expensive. According to data collected by the U.S. Department of Agriculture in 2015, the average annual cost of having a child nowadays is $14,000. That’s almost another minimum wage salary worth of costs to your household expenses.

Being smart about financial planning can make taking on the costs of raising a child easier while giving your family the opportunity to save for the things you really want in life. Of course, not every parent sits down and makes a detailed financial plan once they find out they are having a baby. It’s not unusual to let months — even years — pass before truly getting serious about their money concerns and goals. Whether you are planning for a child in the future or already have a growing family, there’s no better time than the present to start thinking about financial planning.

Creating a Family Budget

A budget provides structure to your overall financial plan. Without a fixed budget, you are vulnerable to the pitfalls of overspending. To build a family budget that actually works, separate your fixed spending from your discretionary spending. Subtract your fixed spending from your total household income and you have a good round number to work with for all the optional things your household needs.

Other things you should have in mind when it comes to creating a budget are your future financial goals. Do you want to move into a bigger house? Have a college fund ready and waiting for your kid once they graduate? Figure out how much you will need to reach these goals and put aside enough money from your discretionary fund that you will reach that goal in a reasonable amount of time.

Invest in Life Insurance

Once you have a child, life insurance isn’t optional anymore. Life insurance can make sure your child is protected and provided for if a worst-case scenario occurs and you are not there to care for them yourself. The monthly cost of life insurance varies by the overall value of the policy as well as case-by-case details. Things such as age, health, gender, hobbies and smoking habits can all have an impact on your life insurance premiums.

When looking at life insurance, understand the different types of policies:

Term life insurance only covers a certain amount of time, generally 10, 20, or 30 years. These plans are more affordable in the short-term, but they can leave your child vulnerable if expired before time of death. Term life insurance can be renewed for another term or even converted to permanent coverage after it has been expired.

Permanent life insurance has no expiration date. It is a good option for people who will have another financially depend on them throughout their lifetime. These policies are more costly than term life insurance, but they can be especially helpful for people with large estates. Permanent life insurance is a way to invest in your family’s future financial security after your death without having to subjugate their inheritance to estate taxes.

One major benefit to life insurance policies is that they hold a cash value. People can sell their life insurance at some point in the future as way to free up all the cash they invested in their policies over the years. Many people choose to do this with life insurance plans once they hit retirement. They buy their life insurance as a way to ensure security for their kids. As the children grow and build lives that warrant their own life insurance, the policy doesn’t really make sense as the parent reaches retirement. They can then sell a life insurance policy and use the cash to help fund their retirement plans or pad their nest egg.

Pre-Paying the Tough Stuff

If tragedy strikes and you are no longer there to be with your family, those you left behind will probably be too shell-shocked to want to deal with funeral arrangements. Planning and pre-paying for your funeral isn’t a pleasant thing, but it can make a world of difference for your loved ones should this tough situation unfortunately occur.

Pre-paid memorials are often arranged with a particular funeral home. Planning should cover everything from the particulars of a service to how you will cover the average $8,500 it costs to have a funeral. There are a few different ways you can choose to pay. A joint bank account with the funds available gives a partner access to the money when it’s needed. Of course, it also leaves the money vulnerable to being spent on something other than a memorial service. Totten Trusts, or a payable on death bank account, don’t provide the funds until the holder of the trust is dead. Selling life insurance or establishing a joint account with the funeral home are also options to consider when it comes to pre-paying for your memorial.

Being a parent is a huge financial burden, that’s why it is so important to establish a financial plan that keeps your money safe. A household budget can provide the framework for your financial plan. Knowing how much you can afford for discretionary expenses based on your total income minus fixed expenses can help you control your impulse buys and overspending. Once you have kids, life insurance is no longer optional. Weigh the pros and cons of term life insurance versus permanent life insurance when looking at plans for yourself. Finally, prepaying your funeral service doesn’t’ just help your family cover a massive expense, it can save them a lot of stress should tragedy strike.

Sara Bailey is a mother of two who lost someone close to her. She knows from experience how important it is for parents to have a strong financial plan. Click on her url The Widow to learn more.

Is college worth it? The answer depends on how much you spend. That’s it. If you spend too much on college, it’s not worth it because your lifetime earnings will never recoup the cost you spent so early in life.

While the thought of incurring student loan debt makes many prospective students reconsider pursuing post-secondary education, the impact of a degree can still outpace the pain of loan debt on future financial well-being as long as the amount is minimized.

A college degree can represent a sound investment in your future earnings. The financial return over a lifetime can make an undergraduate education a good investment – but only if you don’t spend too much for it. Yes, college graduates, on average, earn 84% more over their lifetimes compared to just high school graduates.

But what if your career earnings are only $400,000 more than if you didn’t go to college, and you spent $100,000 in total on college? Making that extra $300,000 over 40 years of working was a really poor use of that original $100,000. That $100,000 would have grown to over $1,000,000 over that same 40 years if you never spent it on education…

But on the flip side, if you only spend $20,000 in total on college, and earn an extra $400,000 over your lifetime, now, that investment is worthwhile. You basically have doubled your future potential earnings ($20,000 would only grow to $200,000 normally – but your education grew it to $400,000).

So, how do you know if college is worth it? Here’s how to dive in and see.

The Value Of College

Why do people go to college? There are a lot of ideals – learning, networking, building lifelong relationships. But the truth is – college costs money. And most students are going to college because they are trying to learn skills that will allow them to earn more money after graduation.

Wait? That sounds like an investment. Because it is!

Students are paying money up front, to see a return on investment after graduation. It’s also part of the student loan crisis today. Too many students borrowed money for this investment, and the return on the investment is not what they expected (thus making it hard to repay the student loans they took out).

What does the data show about the value of college?

Well, one of the most commonly cited pieces of data showcasing the value of college comes from the Social Security Administration.

“Men with bachelor’s degrees earn approximately $900,000 more in median lifetime earnings than high school graduates. Women with bachelor’s degrees earn $630,000 more. Men with graduate degrees earn $1.5 million more in median lifetime earnings than high school graduates. Women with graduate degrees earn $1.1 million more.”

That’s a great data point – but it omits a key factor. How much did that person pay for that degree?

It sounds amazing to suddenly earn $900,000 more over your lifetime (which is approximately 45 years of working after college graduation). But what if you paid $900,000 for that degree? Is it worth it? Of course not.

And that’s the crux of the issue – what’s the value of the increased lifetime earnings in today’s dollars?

The Net Present Value Of Lifetime Earnings

This is where it gets eye opening. It can also be a little messy since we have to make some estimates – such as the rate of return/inflation. We also have to realize that not everyone is equal, not all careers are equal, etc.

But it’s good to have some data points. Let’s calculate the net present value of both $900,000 and $630,000 over 45 years (that means you graduate college at 22 and work until you’re 67). We will use a 5% return rate for our calculation.

Net Present Value For Men ($900,000): $100,167

Net Present Value For Women ($630,000): $70,117

With this incredibly rudimentary calculation, we can see pretty easily the value of college. For a man, if you spend $100,000 on your college education, you’ll break even over your entire lifetime. If you’re a woman, that number is $70,000. If you spend less, you start having a positive ROI, if you spend more than that, you have a negative ROI.

Here’s where it gets a bit scary though. What if we used a more reasonable 8% return rate? The value of college diminishes significantly.

Net Present Value For Men ($900,000): $28,195

Net Present Value For Women ($630,000): $19,373

The truth is, the value of college likely lies somewhere between these two calculations. But you can see it really starts to become NOT WORTH IT if you spend too much money.

So, how can you personally factor this into your college decision?

Calculating Your College ROI

The key to deciding if college is worth it is simply to calculate your Return on Investment (ROI). Specifically, we’re going to look at how much you should borrower to pay for college.

If you can pay cash for your degree, it doesn’t matter if it’s worth it because you’re buying a luxury you can afford (yes, I know education shouldn’t be viewed as a luxury – but the paying cash for it can be). It’s only if you’re going into student loan debt that it really matters.

It’s like buying a car to get to work. The goal is to work so you can earn money, and you need a car to get there. You can buy a really cheap old car – it gets you from your house to work. Or you can buy a brand new Mercedes. They both serve the same function – but one is much cheaper and has a better ROI. But if you have so much money and the price tag doesn’t matter, buy whatever car you want. But most Americans aren’t in that situation – so we have to think critically about the costs and return on investment.

So, the name of the game is to only borrow as much as makes financial sense. And that amount is: never borrow more than your expected 1st year post-graduate salary.

“Never borrow more student loan debt than you expect to earn in your first year post-graduation.”

So, if you plan on becoming an engineer and expect to earn $60,000 per year, don’t borrow more than $60,000 in student loan debt. If you want to be a teacher and only expect to earn $38,000 per year, don’t borrow more than $38,000.

It’s a very easy rule to understand, but it can be hard to follow.

There is also a lot more research today to understand the ROI. For example, the Foundation for Research on Equal Opportunity recently released a bunch of data calculated the ROI on 30,000 bachelor’s degrees from different schools and programs. You can see the real answer to was college worth it.

Related: Where To Apply To College (Finding Financial And Academic Fit)

How To Understand What You Will Earn After Graduation

This can be a tough one – but it’s where you have to start. What do you want to do after graduation, and how much will you earn?

When you’re 17 or 18 years old, it can be impossible to know. But you can get a ballpark (and you should, especially depending on what field you want to go into). Remember, only 27% of graduates have jobs related to their major in college, but that’s a good baseline of where to start.

Once you have a ballpark, you can build a buffer around that. Want to go into education? See what low end teacher make in your state. Marketing? See what marketing jobs are available? Want to be a doctor? Well, I hope you’ve spoken to some doctors.

If you don’t know where to find salaries, look at sites like Glassdoor and Indeed. Both sites have salaries and company reviews – which can be helpful to understand a bit more about big companies in the industry you want to get into.

Reduce Tuition Costs

Research in state school tuition as well as other lower cost programs. While the benefit of an Ivy League education could pay off in networking and career opportunities, it does not make sense to overspend for those benefits. Find well-ranked, lower tuition options.

You could also opt for a hybrid of starting at a community college (which is free in 30 states), and then transferring to a state school after you knock out your general education requirements.

Seek financial aid and scholarships. There is money available to students of all abilities and financial backgrounds. With a little bit of leg work, it is possible to reduce ballooned school tuition to a minimal cash investment. Don’t rule out working for a university, often employee benefits include free tuition in addition to comfortable salaries.

Choose to live at home or rent a low cost apartment off campus. Reducing or eliminating room and board expenses can help limit the amount of student loans.

Related: The Ultimate College Budget Guide

Accelerate Your Studies

Take AP courses in high school, or test out of entry level courses with options like the CLEP. Pick a major and stick to the core studies to prevent spending valuable tuition money on extraneous classes. Opt to take lower cost general education credit hours at a community college. Get ahead of your investment by graduating early and on time. Extending your stay in school only increases debt and postpones your ROI.

In my case, I took as many AP courses as possible, and took the AP exam each spring. As a result, I was able to start college with sophomore standing due to the amount of credits I received for my AP classes, and I was able to graduate early (even though I changed my major). AP courses were the key to graduating early and saving a bit on college costs.

Work Through College

Don’t be afraid to go out and work during school. Beyond the fact that you get paid and you can use this money to offset the costs of your college education, working gives you amazing skills that you can transfer to any job after college.

For many college students, working in retail or in a restaurant is a flexible way to find a job while still being able to balance your school schedule.

Conclusion – Is College Worth It?

Is college worth it? Maybe.

Like any investment, you won’t know until after you make it and start to realize the returns. But you can protect yourself by spending as little as possible up-front.

For example, mitigating the amount of student loan debt you carry with you into adult life creates a better foundation to make future investments and grow personal wealth.

While there are many pathways to success, an undergraduate degree is still a good option for those looking to earn a solid living and live in financial comfort. The return on the investment depends on students managing money wisely, making strong career choices, and backing up their diplomas with discipline and work ethic.

While incurring loan debt sets students behind non-degreed workers for the first few years of employment the earnings potential of those with college degrees far outpaces those without. However, it only makes sense if you don’t spend a lot of money on that undergraduate degree.

What do you think? Is college worth the investment?

Welcome to this week’s publication of the Market’s Compass Developed Markets Country (DMC) ETF Study #505. It highlights the technical changes of the 21 DM Country ETFs that I track on a weekly basis and publish every third week* There are three ETF Studies that include the Market’s Compass US Index and Sector (USIS) ETF Study, the Developed Markets Cou…

Michael Wiggins De Oliveira is an inflection investor. This means buying into cheap companies at the moment when their narrative is changing and the business is on a path toward becoming significantly more profitable over the next year.

With a focus on tech and “the Great Energy Transition (including uranium)”, Michael runs a concentrated portfolio with approximately 15 to 20 stocks and an average holding period of 18 months.

Through his 10+ years analyzing countless companies, Michael has accumulated outstanding professional experience in tech and energy and a following of over 40K on Seeking Alpha.

Michael is the leader of the investing group

Deep Value Returns

Features of the group include: Insights through his concentrated portfolio of value stocks, timely updates on stock picks, a weekly webinar for live advice, and “hand-holding” as-needed for new and experienced investors alike. Deep Value Returns also has an active, vibrant, and kind community easily accessible via chat.

Learn more

Seeking FCF is an associate of Michael Wiggins De Oliveira

Analyst’s Disclosure:I/we have a beneficial long position in the shares of UEC either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Think of public housing, and a familiar picture comes to mind: hulking, run-down brick tenement buildings, graffiti-strewn malfunctioning elevators, crime, drugs, and all the social ills that go with it. Unsurprisingly, previous governments sought to move away from public housing as a solution for low-income residents. However, the affordability crisis has placed housing firmly back in the spotlight, and public or social housing, as it is now being termed, is once again being touted as a solution.

If only it were that simple.

The Urgent Need for Affordable Housing

With homelessness on the rise and both the working and middle classes feeling the effects of elevated home prices—homes are unaffordable in 80% of U.S. counties—high interest rates and escalating rents, there’s little doubt about the need for affordable housing. Even both presidential candidates have offered solutions.

“This is hitting first-time home buyers that can’t get into the housing market.This is hitting middle-class renters who are spending more than 50% of their income on rent,” Brian McCabe, Associate Professor of Sociology at Georgetown, told Time. “It’s not that there’s never been an affordability crisis before, but it’s now an affordability crisis that’s hitting a much broader set of Americans.”

The Different Sides of Public Housing

Not all public housing consists of crime-ridden, poorly maintained tenements. It’s back in the spotlight because of innovative and attractive developments such as The Laureate in Montgomery County, Maryland, which has transformed notions of what the term can mean. In most settings, the Laureate would be termed a luxury apartment building with its raft of amenities and attractive, modern construction.

Montgomery County has been an innovator in public housing initiatives. It instigated a landmark law that requires developers to set aside about 15 percent of the units in new projects for households making less than two-thirds of the area’s median income—now $152,100 for a family of four. For-profit developers built the Laureate, but the controlling owner is a government agency, the Montgomery County Housing Opportunities Commission. H.O.C. has a 70% stake, so the Laureate can set aside 30% of its 268 units for affordable housing.

It’s a far cry from the first self-contained and largest cooperative housing development ever built, Co-op City in the Bronx. Few can dispute the bold intentions and even bolder scale of the 15,000-unit development, completed in 1973 and often referred to as a “city within a city.” Democratic lawmakers Alexandria Ocasio-Cortez and Tina Smith cited Co-op City as an example of how public housing can work. However, that development has a history of poor management, corruption, and squalid conditions, which led to an emergency repair bill of $500 million in 2003. Co-op City, while laudable for its intentions, is hardly the shining star to encourage further investment in public housing.

But neither is The Laureate as attractive as it is. That’s because the Laureate is geared toward the middle class and is located in a wealthy county. Residents who earn around $50,000/year can expect to pay $1,700 for a one-bedroom apartment, compared with a market rent of around $2,200. Other residents might expect to pay half the advertised rate depending on their income. Montgomery County was able to kick in $100 million, using its ownership position to become a benevolent investor that trades profits for lower rents.

“The private sector is focused on return on investment,” Chelsea Andrews, H.O.C.’s executive director, told the New York Times. “Our return is public good.”

Developers Are Rejecting Government Funding

Unfortunately, that’s not a position that many financially stressed counties can adopt. Public housing is usually financed by the Department of Housing and Urban Development and operated by one of the nation’s roughly 3,300 public housing agencies, which are locked in a steady decline.

That’s partly why private developers are rejecting government money for affordable housing. Mismanagement and red tape in the public sector have a history of bloating construction expenses and other costs for developers. It’s why—despite the commitment of tens of billions of dollars from Californian State and local government, some developers such as S.D.S. Capital Group, which recently completed a 49-unit apartment building in South Los Angeles, has self-financed the project. S.D.S. told theWall Street Journal that it cost them $291,000 per unit to build instead of the roughly $600,000 that the city of Los Angeles has averaged for similar apartments.

A recent report commissioned by the city of San Jose found that affordable housing projects that received tax credits cost an average of around $939,000 a unit to build there last year. The average affordable unit in the Bay Area costs $817,000 to build, according to a study by the Bay Area Housing Finance Authority and the affordable housing finance company, Enterprise.

Rather than using government cash, S.D.S., an investment firm, raised a $190 million fund to build an estimated 2,000 units for formerly homeless people in the city with mental health and other medical needs. The speed of private, self-funded construction has proved to be a big savings compared to the governmental bureaucracy that hampers similar projects.

“We believe there’s a different way than using government money, which really becomes slow and arduous and increases cost,” Deborah La Franchi, chief executive of S.D.S., told the Wall Street Journal.

“You’re cutting out millions of dollars just in soft costs,” David Grunwald, an executive at R.M.G. Housing, which is developing the S.D.S. fund’s projects, said of private financing.

Why Section 8 Has Faltered

Unlike many landlords, S.D.S.’s model is unique in that it accepts government vouchers—Section 8—to house residents. The Los Angeles City Housing Authority says there are over 1000 unused tenant vouchers at any one time, which provides a captive market for S.D.S. buildings.

Activists have found that the rejection of Section 8 vouchers by brokers looking to rent apartments is a nationwide issue. A watchdog group, Housing Rights Initiative, filed a lawsuit in New York in 2022, citing—after a sting operation—the discriminatory practices of landlords and real estate agents when turning away prospective tenants who rely on subsidies to pay rent. It is illegal in New York City for landlords to refuse to accept applications from tenants who depend on them.

“Housing discrimination is not an isolated incident,” Aaron Carr, the executive director of the Housing Rights Initiative, told the New York Times. “It is a part of an industrywide problem.”

When Bill Clinton encouraged the movement away from public housing construction with the Faircloth Amendment in 1998, the hope was that private landlords in mixed-income buildings would take up the slack. Henry Cisneros, Bill Clinton’s H.U.D. Secretary developed a plan that consolidated grant programs and shifted the emphasis to housing vouchers over traditional public housing subsidies.

According to a H.U.D. report, HOPE VI, a H.U.D. program aimed to redevelop “severely distressed” public housing projects, demolished 98,592 public housing units and replaced them with 97,389 mixed-income units between 1993 and 2010. It was widely considered a move out of a Republican playbook and received no blowback. However, gentrification and the demand for housing from non-voucher renters have pushed Section 8 tenants further into the margins of low-income housing in dicey neighborhoods. Many tenants feel that rejecting Section 8 is a mask for racial discrimination. Some landlords and renters conversely feel Section 8 tenants can disrupt their buildings and neighborhoods.

Insurance: The Silent Killer

As if public/affordable housing wasn’t facing enough issues, soaring insurance costs have made things unsustainable for developers, landlords, and management companies. It’s not just in areas of extreme weather but nationwide where costs have quadrupled along with deductibles.

Unlike market-rate apartment developers, multifamily projects financed by subsidies and tax credits cannot pass on those higher insurance costs to tenants since they are limited by government guidelines as to how much rent they can collect. As a result, developers and housing authorities have appealed to state lawmakers for assistance or have decided to abandon affordable housing completely. According to aNational Leased Housing Association survey, nearly one-third of affordable housing providers reported increases of at least 25 percent.

“In 2020, I would have said this is cyclical; the pendulum has always been swinging,” Denise Muha, the organization’s executive director since 1988, told the New York Times. “But this is totally different. I don’t see this really curing itself anytime soon.”

Final Thoughts

Affordable housing in America is an oxymoron in this day and age. The red tape, bureaucracy, and social issues that come with providing it have made it a minefield for developers and investors. While public housing developers such as S.D.S. have largely circumvented the problem by taking matters into their own hands and bypassing the government, there is still the issue of management and upkeep. The lessons learned from Co-op City City is that despite a city’s best intentions, when the management of a project cannot run efficiently and ethically and without the finances it needs, things will deteriorate quickly.

Public housing advocates worldwide often point to Vienna, which, with its huge apartment complexes known as Gemeindebauten, has made Austria’s capital one of the world’s most livable cities. Why they have succeeded so spectacularly in Austria but not so in the U.S. is, however, a far longer discussion.

Get the Best Loan Today

Find trusted, investor-friendly lenders who specialize in your strategy.

Ready to succeed in real estate investing? Create a free BiggerPockets account to learn about investment strategies; ask questions and get answers from our community of +2 million members; connect with investor-friendly agents; and so much more.

Note By BiggerPockets: These are opinions written by the author and do not necessarily represent the opinions of BiggerPockets.

")