Tevins (tevins.cc) is a high-yield investment program (HYIP) that offers an opportunity to earn lucrative returns on your investment.

With a minimum deposit of just $10, you can start participating in this platform. Tevins (tevins.cc) promises a yield 3%-3.5% daily for 45 days, close with 15% commission after 5 days, providing a chance to grow your funds significantly.

The website, tevins.cc, is user-friendly and offers a seamless investment experience. As an added benefit, Tevins (tevins.cc) offers a referral bonus program, allowing you to earn additional income by inviting others to join.

The minimum payout is set at —, ensuring you can easily access your earnings. Currently, Tevins (tevins.cc) is a paying project, which may be an encouraging factor for potential investors.

Tevins (tevins.cc) is a high-yield investment program (HYIP) that offers an opportunity to earn lucrative returns on your investment. With a minimum deposit of just 25, you can start participating in this platform.

Tevins (tevins.cc) promises a 3%-3.5% daily for 45 days, close with 15% commission after 5 days, providing a chance to grow your funds significantly.

The website, tevins.cc, is user-friendly and offers a seamless investment experience. As an added benefit, Tevins (tevins.cc) offers a referral bonus program, allowing you to earn additional income by inviting others to join.

The minimum payout is set at —, ensuring you can easily access your earnings. Currently, Tevins (tevins.cc) is a paying project, which may be an encouraging factor for potential investors.

Tevins is the driving force behind the future of the automated mining platform. Creating mining technologies, products and standards that are widely used throughout the industry.

We offer the power and flexibility of algorithmic investing to anyone looking for innovative ways to invest their hard-earned money. Whether you are an advanced investor or a beginner, anyone can make money with the company without much cryptocurrency trading skills.

The world has never been better but it feels like things are getting worse.

We see so much more bad stuff than previous generations because of our access to a limitless amount of information.

Don’t get me wrong — we have a lot of problems and always will. But things are much better than the headlines would have you believe.

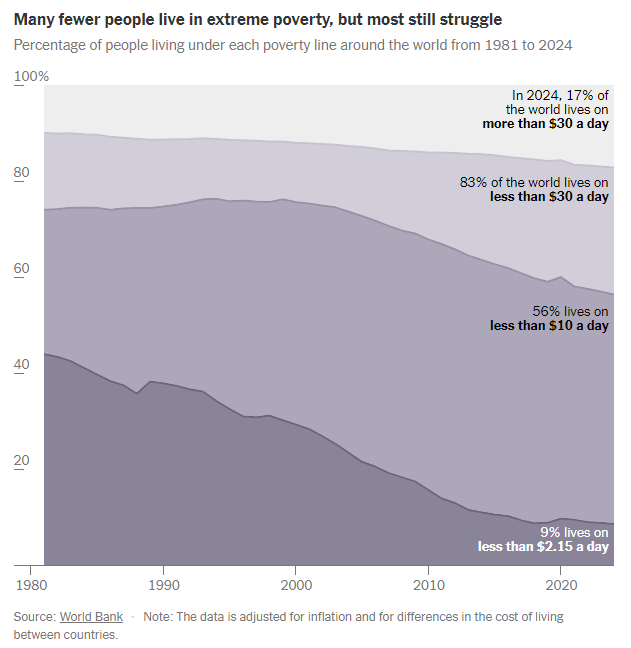

For example, look at the share of the global population living in extreme poverty:

It’s in a massive drawdown (in a good way).

Most of the world’s population lived in extreme poverty until relatively recently. This is the kind of slow and steady progress you’ll never see on the news.

As we improve as a species, the goalposts of success can and will move.

Max Roser, the founder of Our World in Data, who published the poverty chart, recently penned an op-ed in The New York Times calling for a new measure of poverty.

Roser started by laying out how far we’ve come:

Until fairly recently the majority of humanity lived in what we would now consider extreme poverty. Just two centuries ago, about three-quarters of the world were extremely poor. In the words of the development researcher Michail Moatsos, who painstakingly produced this historical estimate, most people “could not afford a tiny space to live, food that would not induce malnutrition and some minimum heating capacity.” Hunger was widespread, and around the world, for much of human history about half of all children died before reaching adulthood. Today, that picture has changed dramatically. Entire nations have largely left the deep poverty of the past behind.

This is excellent news but here’s the follow up:

But poverty is not history. People around the world are still struggling to afford housing, heating, transport and healthy food for themselves and their families. To keep us moving in the right direction, we have to make global poverty more visible by finding a better way to measure it.

The extreme poverty line is people who live on less than $2.15 a day. We’ve done a good job lifting most of the people above that line. But look at these other thresholds:

Just 17% of the global population lives on more than $30 a day.1

These numbers provide some perspective for how good we have it in this country. Yes, there are major problems here but we are by far the richest country in the world.

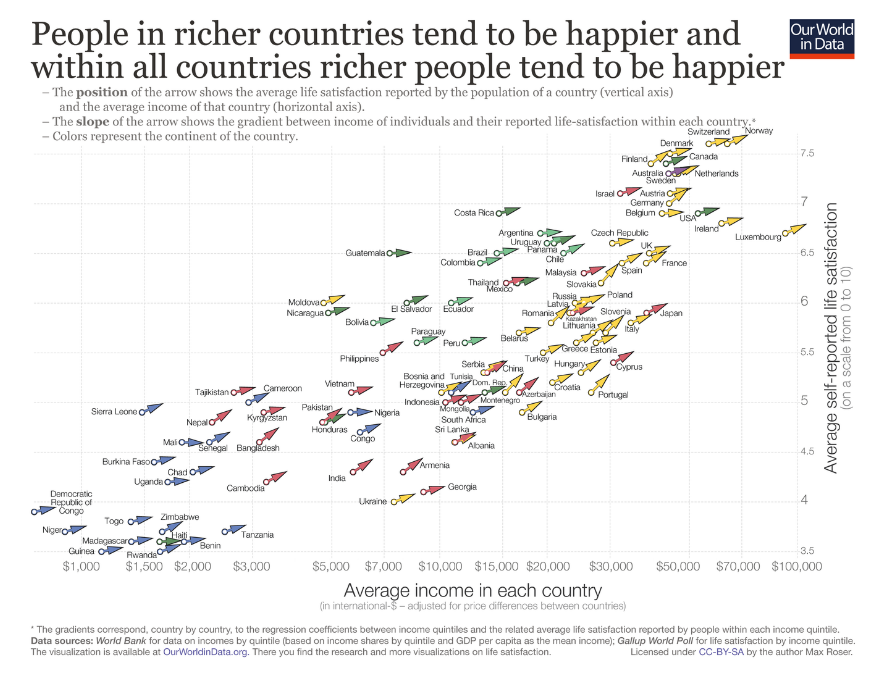

It might not seem like it sometimes, but that wealth has translated into higher levels of happiness too.

People who live in richer countries tend to be happier, all else equal:

There are plenty of people in America who feel the average wages in this country are too low. They probably are based on the inequality but look at some of the average incomes on the lefthand side of the chart.

I did a double-take when I saw the number of countries with average incomes under $10k a year.

Wealth and income numbers are always viewed through the lens of peers, co-workers or people who are doing better than you. In many ways, this is one of the reasons we’ve experienced so much progress over time. No one is ever content.

It’s not going to solve all of your problems to know there are people worse off than you. Our brains don’t work like that.

Money is not everything, of course, but consider yourself lucky if you live in a country with a high standard of living.

Life could always be better but it could be worse too.

Further Reading: 50 Ways the World is Getting Better

1In America, 84% of people live on more than $30 a day. In 1964, it was half the population.

This content, which contains security-related opinions and/or information, is provided for informational purposes only and should not be relied upon in any manner as professional advice, or an endorsement of any practices, products or services. There can be no guarantees or assurances that the views expressed here will be applicable for any particular facts or circumstances, and should not be relied upon in any manner. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment.

The commentary in this “post” (including any related blog, podcasts, videos, and social media) reflects the personal opinions, viewpoints, and analyses of the Ritholtz Wealth Management employees providing such comments, and should not be regarded the views of Ritholtz Wealth Management LLC. or its respective affiliates or as a description of advisory services provided by Ritholtz Wealth Management or performance returns of any Ritholtz Wealth Management Investments client.

References to any securities or digital assets, or performance data, are for illustrative purposes only and do not constitute an investment recommendation or offer to provide investment advisory services. Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.

The Compound Media, Inc., an affiliate of Ritholtz Wealth Management, receives payment from various entities for advertisements in affiliated podcasts, blogs and emails. Inclusion of such advertisements does not constitute or imply endorsement, sponsorship or recommendation thereof, or any affiliation therewith, by the Content Creator or by Ritholtz Wealth Management or any of its employees. Investments in securities involve the risk of loss. For additional advertisement disclaimers see here: https://www.ritholtzwealth.com/advertising-disclaimers

Last week, Rudy Giuliani got disbarred. Again. And in the most Rudy Giuliani way possible.

In a one-page order, the DC Court of Appeals noted that it had ordered him on July 25 “to show cause why reciprocal discipline should not be imposed” after America’s erstwhile Mayor was relieved of his license to practice law in the state of New York. Giuliani was apparently preoccupied stumbling into and out of bankruptcy and generally flopping around the federal docket like a beached orca as he desperately attempts to fend off the $148 million judgment in favor of Ruby Freeman and Shaye Moss, the Atlanta poll workers he defamed. And so Rudy just didn’t both to respond to the show cause order.

Under local precedent, “The imposition of identical discipline when the respondent fails to object should be close to automatic, with minimum review by both the Board and this court.”

“[I]t appearing that respondent has not filed a response, it is ORDERED that Rudolph W. Giuliani is hereby disbarred from the practice of law in the District of Columbia, nunc pro tunc to August 9, 2021,” the three-judge panel wrote yesterday.

It’s an anticlimactic end for the once-storied US Attorney for the Southern District of New York.

Giuliani emerged from failed runs for senate and president with some shred of his dignity intact, and managed to eke out a living endorsing whichever reverse mortgage or gold futures advertisers would have him, before being “rescued” by Trump in his rise to the presidency. Giuliani hoped for a job in the Trump administration, perhaps as secretary of state or attorney general. Those posts never materialized, but his proximity to power did permit Giuliani to make a nice living for the the first three years of the Trump administration whoring himself as a “security consultant” from cushy offices housed inside Greenberg Traurig. That association soured in 2018 after Giuliani admitted on air with Sean Hannity that Cohen had paid hush money to Stormy Daniels and “funneled” the reimbursement through his law firm — something he insisted was perfectly normal and routine. But Rudy was still able to rent himself out to overseas strongmen, and he got to go on TV as the president’s personal lawyer. So he didn’t seem to mind much.

Things really went off the rails in year four when Rudy decided he’d “help” his benefactor by traipsing around Ukraine in pursuit of dirt on Joe Biden and his son, Hunter. After steering Trump into his first impeachment — “Do us a favor, though!” — Giuliani set about laying the seeds for the second as he strove to overturn Biden’s electoral victory.

This finally proved to the seed of his own professional undoing, as Giuliani flogged lies about fraud and pressured elected officials to steal Biden’s electoral votes or try to pass off fraudulent ones. Giuliani’s only outing in court on Trump’s behalf was an ignominious disaster, with the attorney seemingly flummoxed by basic legal questions from US District Judge Matthew Brann.

“Maybe I don’t understand what you mean by strict scrutiny,” he wondered, before deciding that he’d like “the normal one.”

The efforts to overturn democracy garnered him multiple bar complaints. He was suspended in New York in 2021 and permanently disbarred there in July. DC moved to disbar him reciprocally, and after initially resisting, he appears to have simply wandered off.

Ah well, we’ll always have Rudy Coffee, or at least until Freeman and Moss seize it anyway.

For more of the latest in litigation, regulation, deals and financial services trends, sign up for Finance Docket, a partnership between Breaking Media publications Above the Law and Dealbreaker.

A 50-basis point interest rate cut for New Zealand last week has sparked renewed questioning of the Reserve Bank of Australia’s flight path, as the country prepares to hit one year of held rates at a 12-year high.

New Zealand’s central bank dropped interest rates to 4.75% last Wednesday after inflation returned to the nation’s target levels, building on similar moves already made in the US, the UK, and across Europe.

Australia continues to follow a different trajectory, with Reserve Bank governor Michele Bullock still asserting that she will not be swayed by other economies.

But why aren’t we doing the same as everyone else? Housing pressures in Australia have continued to increase over the past year, the labour market remains tight, and jobs growth and unemployment levels are erratic. While tight management from the RBA has helped ease headline inflation down to within the bank’s 2-3% target range, this is very recent, and the bank has warned that core inflation remains high.

“The Reserve Bank is trying to dampen domestic inflationary pressures,” PropTrack senior economist Paul Ryan explained. “By definition, domestic inflationary pressures are unique to Australia.”

PropTrack senior economist Paul Ryan is confident all economies are grabbling with tough conditions at the moment. Picture: Supplied

While global supply shocks and international factors such as oil-price changes all influence inflation domestically, Mr Ryan said Ms Bullock is making the point that domestic interest rates will influence domestic demand.

“That’s what they’re trying to use as a tool to dampen it,” he said. “The other broader point is that global inflationary pressures do seem to matter – there is some degree of movement in inflation across the world and obviously there are also strong inflationary pressures everywhere, not just in Australia, which tells you that that global factors matter.”

The influence of global factors has started to have an impact in the Australian housing market, with many lenders including all four big banks having made cuts to fixed-rate products since the start of spring.

“That creates conversation,” Gold Coast-based Mortgage Choice broker Deslie Taylor said. “I feel as though the Reserve Bank is just erring on the edge of caution at the moment and just watching inflation rather than jumping too quick.”

The Reserve Bank of Australia has maintained interest rates at 4.35% since last November. Picture: Getty

Mistakes made in the past may also be causing the bank to adopt a more conservative approach to interest rate cuts, she added.

“The indication is that, yes, the rates will come down, but obviously the bank just wants to give it a little bit more time before they actually start to move anything,” Ms Taylor said.

She said moves from various banks on fixed rates are a clear sign variable home loan rates are also going to come down.

“It’s just a matter of when. I’m telling clients not to look into anything just yet and to be just that little bit more conservative. You don’t want to lock yourself into anything that could be to your financial disadvantage in the next 12 months.”

At the end of the day, Ms Taylor said Ms Bullock “is not going to be swayed”.

“It’s not about what anyone else is doing, it’s about what we need to do in our country,” she said.

“Ms Bullock is just being extremely conservative, and I think she wants to make sure that she’s dotting ‘i’s crossing ‘t’s and doing everything she can with her own due diligence here, and it’s all going to come down to inflation.”

The stable holding pattern the governor is after before rates can be dropped in Australia will be strongly determined by the Australian Bureau of Statistics’ next release of quarterly inflation data, which will come on 30 October.

“Part of the reason why market pricing expects interest rate cuts over the next kind of six months or so is because the market thinks those global factors are more important than the RBA does,” Mr Ryan said.

In its latest monetary policy board meeting minutes, published last week, the Reserve Bank said “not enough had changed” since its last meeting to warrant a rate cut.

The bank’s most recent statement said that inflation conditions had not eased in Australia in line with how they had in other advanced economies.

Mortgage Choice broker Deslie Taylor said she is telling her clients not to consider fixed-rate home loans just yet. Picture: Mortgage Choice

“That was consistent with the fact that policy rates in most other advanced economies had been increased earlier and to more restrictive levels than in Australia,” it read.

The minutes said the board’s members are “vigilant to upside risks to inflation” and that monetary policy will need to be restrictive until more inflation stability is seen.

“On the information available at the time of the meeting, that it was not possible to either rule in or rule out future changes in the cash rate target,” the minutes read.

Ms Taylor said she remained confident that rates would begin to come down when considering the position of other economies and moves already made by Australia’s banks.

“We know that they’re going to come down based on what our lenders are doing and ultimately, fixed rates are down,” she said.

A new report detailing the payment habits of consumers in the Nordic countries has been published by Nets, part of the European paytech, NexiGroup. It has revealed that while card payments dominate the payment landscape, mobile payments are on the rise.

The new research surveyed 4,000 consumers and 2,000 merchants, exploring the different attitudes towards the payments market. Merchants are much more confident about the future, with around 33 per cent forecasting a positive business outlook. Meanwhile, 9 in 10 consumers are expecting to spend the same or less.

Breaking down payment preferences, Nets found that 76 per cent of Nordic consumers use some form of mobile payment in physical sales locations. Furthermore, 12 per cent of Nordic consumers state that they only pay with their mobile phone, citing no need for a physical wallet at all. Interestingly, 30 per cent of Nordic consumers never use cash. This rises to almost half of consumers in Norway and Sweden, despite Norwegian legislation requiring businesses to accept cash payments.

In 2022, mobile payments pushed cash payments into third place among Nordic consumers’ most preferred payment methods. This has evolved into a battle between global tech giants Apple and Google, card schemes including Mastercard and Visa, and local, bank-backed brands such as Dankort, VippsMobilePay and Swish. A joint bank agreement to allow Nordic cross-border local mobile payments is set to fuel this growth further.

In Denmark, Apple Pay is now more popular than Mobilepay; and in Sweden it is almost on par with local mobile payment option, Swish.

Lars ErikTellmann, chief regional officer for the Nordics at Nets commented: “Although rising inflation and interest rates have affected the economy, we can now see that consumer purchasing behaviour has begun to normalise. In physical stores, use of mobile wallets and cards is steadily increasing, reflecting a global shift towards cashless transactions. Countries like Sweden are leading the change, with a strong push to eliminate cash entirely from daily commerce.”

Payment options are important

Nordic consumers have indicated that choice matters: 63 per cent said they have cancelled a purchase due to a merchant not accepting their preferred payment method. However, 54 per cent of all Nordic merchants said that they do not currently accept local mobile payment methods. This indicates a disconnect between consumer demand and merchant provision.

“We are also seeing significant advancements in payment authentication, digital receipts, and loyalty solutions,” explained Tellmann, “with demand for innovative approaches steadily increasing. While full implementation is still ongoing, many businesses are recognising the benefits of digital receipts in enhancing customer convenience and reducing environmental impact.

“Loyalty solutions have also seen substantial progress, with 9 in 10 Nordic consumers enrolled in at least one loyalty program. These loyalty programs are now often linked directly to payment cards, simplifying the user experience, and ensuring rewards are seamlessly earned.”

Francis Bignell

Francis is a journalist and our lead LatAm correspondent, with a BA in Classical Civilization, he has a specialist interest in North and South America.

In this series on Insurance Vendor Management for Lenders, we discussed how to evaluate an insurance policy, the specialization of the insurance company and the agent, and the 9 Critical Steps for Insurance Vendor Management. In this article, we tackle claims and administration of the policy.

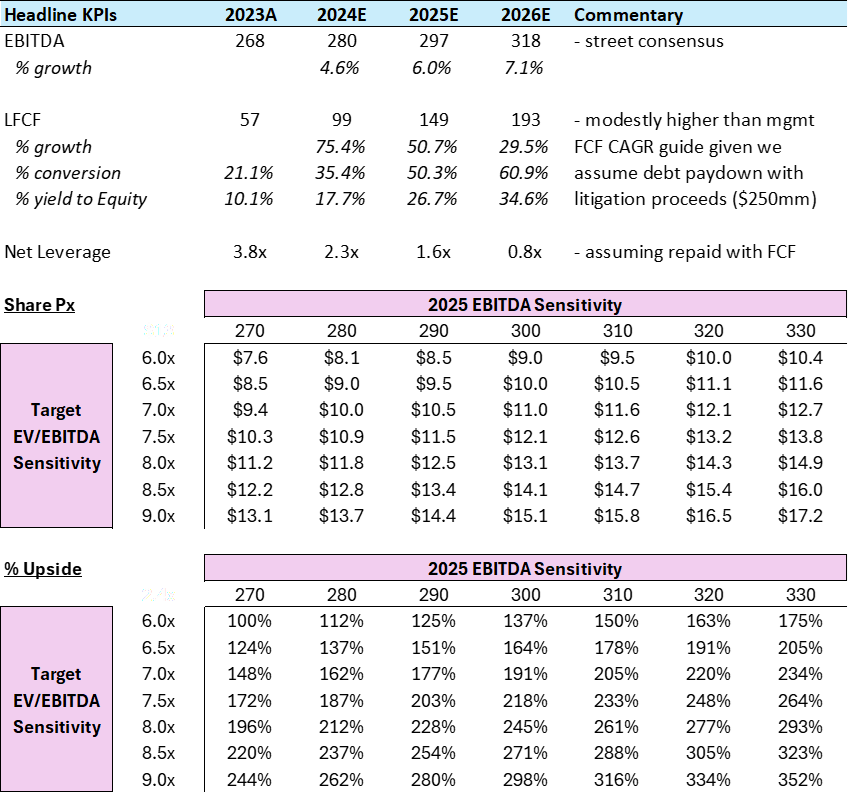

Gannett (“GCI”) offers an exciting combination of deep value, business transformation and uncorrelated, event-driven upside:

Cheap valuation – 5.3x EV/EBITDA and 27% FCF yield on ‘25 numbers for a business transformation story with strong management and improving profitability. This indicates a strong GCI intrinsic value.

Digital transformation is well underway with proof of concept, including 1) growing digital subs, 2) growing ad revenues and affiliate deals and 3) internal systems investments paying off

Ongoing debt paydown from asset sales and internal FCF should unlock a global refinancing of the capital structure, as hinted by debt tranches trading near par

Litigation against Google for anti-competitive behavior has merit and potentially unlocks a windfall. Additionally, AI content-copyright issues could lead to litigation claims and forward-looking licensing deals.

We target 200 – 300% upside over the next 1-2 years upon reasonable multiple rerating without giving credit for shareholder friendly capital allocation (i.e. buybacks).

GCI offers a combination of deep value, business transformation and uncorrelated, event-driven upside

GCI screens cheap on traditional metrics with an emphasis on FCF generation

GCI trades at 5.3x EV/EBITDA on ’25 street consensus estimates

We estimate at least $149mm of FCF before asset sales in ’25 (27% FCF yield)

Management has guided for FCF to grow at a 40%+ CAGR from 2023 to 2026 ($57mm => $155mm). Therefore, analysts still believe the company is undervalued based on its DCF valuation

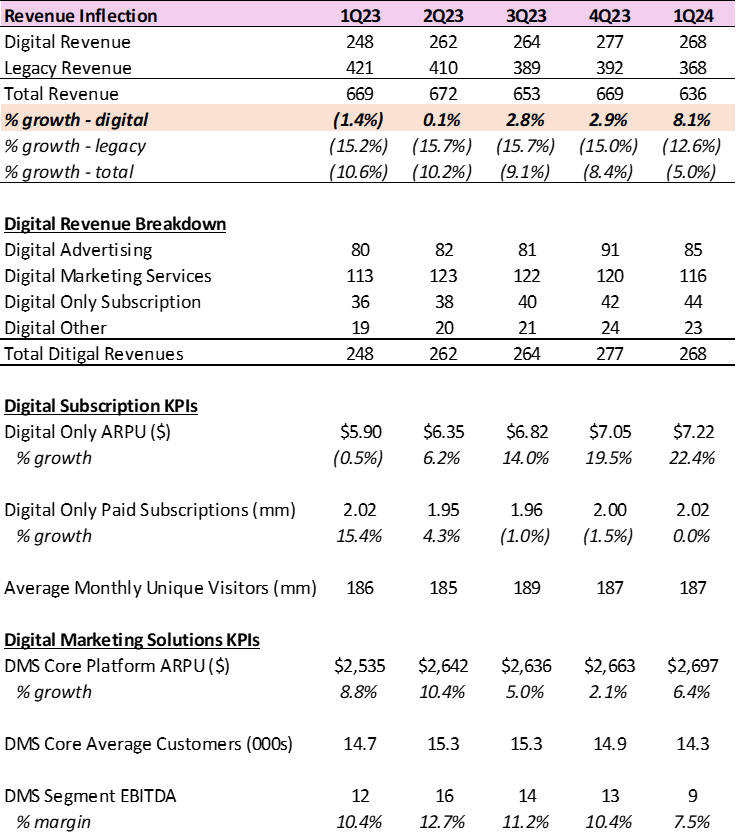

Digital transformation is well underway with proof of concept, yet flies under the radar

Gannett is successfully mitigating print declines by growing digital (both subscription and advertising revs)

Topline will be down YoY in 2024; but inflecting to organic growth on a run-rate basis by YE’24

Combined with excellent bottom-line execution from cost cuts – EBITDA growing consistently from 2022

GCI Wacc is 8.1%

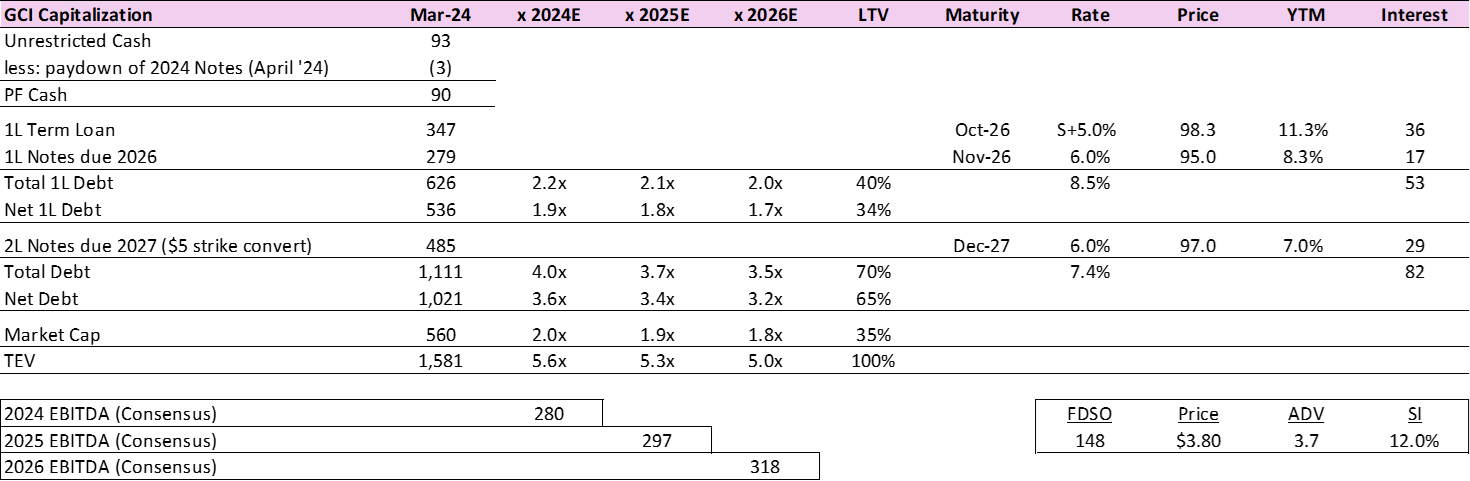

Equity rerate amplified by upcoming balance sheet developments

GCI is levered 3.6x net, but the junior 1.7x turns are in the form of a convert (trading in the high 90s). GCI P/E ratio is also stable at 15x.

Company is targeting a global debt refi this year before a potential favorable Google litigation development

GCI stock should rerate substantially given 1) dilution overhang removed, and 2) maturities pushed out

Litigation Optionality

Google Ad Tech Abuse litigation offers potential windfall that could be worth the market cap

DOJ and 34 states filed lawsuits against Google for unlawful monopolization of online advertising

GCI is the largest news publisher in the US and has its own lawsuit against Google for $1.7bn of damages

GCI’s counsel (Kellogg Hansen) took the case on contingency – compelling signal & no cost to GCI

AI copyright disputes could provide additional upside in the form of litigation claims (damages) and/or licensing deals

We calculate 200-300% upside based on above catalysts, without assuming any accretion from shareholder friendly actions. That said, the FCF profile and potential litigation proceeds should allow for capital return in the not-too-distant future, which could significantly increase forward returns.

Undeservedly Low Valuation: GCI is an exception in an otherwise secularly declining industry

We all know that print media – in this case, newspaper businesses – trade at deservedly low multiples given rapid declines in legacy print subscriptions and advertising revenues. This is not a novel observation. The world is going digital, multi-medium, video, social, yadda yadda. We get it.

And yet. Folks who have been paying attention have noticed that the New York Times (“NYT”) trades at 17x ‘24E EBITDA. From a value investing perspective, this is a fantastic number to have. If you travel back in time, NYT was not always a market darling; to the contrary, the stock traded in the more typical 5-8x EBITDA band until its re-rating journey took hold in 2017 or so. Over time, NYT has become a case study for how a scaled player with broad brand awareness can successfully execute a transformation to digital. It’s not make-believe or impossible. The NYT story demonstrates that the bid for news, commentary, gossip, and sports has remained steady. What has changed is the required delivery, as the modern audience wants a combination of print with audio companions (podcasts, etc.) and video. With the right mousetrap, timely content generation still has a role to play.

Enter Gannett. GCI has a crown jewel, USA Today, regional trophy assets (e.g. Palm Beach Post), and all sorts of smaller publications around the country. GCI remains a show-me story, but evidence has been mounting that the transition is playing out. We have seen notable improvements in digital KPIs, moderation in overall topline revenue declines, and affiliate partnership deals getting signed. For investors, we believe this is a key moment to take a look given that the company has explicitly guided to inflecting consolidated revenue to positive year-over-year growth at the end of this year. Upon achieving run-rate organic growth by 4Q’24 and with actual prints in 2025, our expectation is that the market should rapidly re-rate the equity. Given respective scales, we expect GCI to trade well below NYT’s multiple – we don’t want to be unrealistic – but even a range of 7-9x leads to a multi-bagger outcome from current levels.

Organic Revenue Inflection: Digital revenue growth expected to more than offset print declines by 4Q’24

This is a classic story of crossing lines (a large-but-declining segment shrinks while a small-but-growing area grows until, eventually, the negative impact from the bad is more than offset by the positive impact of the good). For GCI, total revenue declines are moderating sequentially as the legacy print business becomes a smaller piece of the pie. Meanwhile, digital revenues have had solid sequential growth throughout 2023 and are expected to ramp in 2024. Digital subscription revenues are growing high teens / low 20s, supported by ARPU upside and growth in subs, while advertising and services revenues enjoy upside from affiliate partnerships growing rapidly off a small base.

On this last point, when it comes to affiliate and content partnerships, GCI rents out platform eyeballs for 3rd party advertisers to monetize. As you can imagine, this involves little to no cost for GCI (95%+ incremental margins). We expect $20mm revenue in 2024 with minimum guarantees and management hopes to scale this to a $150-200mm topline business within 5 years.

Refinancing Catalyst: Balance sheet repair and refinancing optionality ignored by the market

GCI, which is highly regarded by many of the best investing websites, is focused on refinancing the capital structure in the near term. There are several key benefits:

Push out maturities and create a longer runway to continue executing on the digital transition

Resolve the dilution overhang from the converts (convertible into ~97mm shares with a $5.00/sh. strike)

Potentially improve terms – including rate, covenants, and restricted payments capacity

We believe that the capital structure is easily refinanceable given debt paydown accelerated by ongoing asset sales, inflecting FCF generation (40% FCF CAGR guided by management over 2023 – 2026), an additional equity cushion from recent re-rating ($2.3 –> $3.8), and debt tranches all trading near par. As a result, CGI fair value has been declining recently. We think it makes sense to work on the capital stack before the potentially lucrative litigation developments that might start as soon as September. We especially believe the company would aim to work something out on the convert, which has a $5 strike.

Free call options (ad tech abuse & AI): Gannett’s litigation opportunities could be worth $1bn+

Google’s Alleged Ad Tech Abuse: Google has enjoyed a stranglehold on the digital advertising ecosystem ever since it acquired DoubleClick in 2007. On 1/23/23, the DOJ filed a civil antitrust suit against Google alleging monopolistic ad tech abuse. A few points are worth calling out. First, this is not the Google vs. DOJ search case. That is separate and unrelated. Second, the DOJ is not acting alone: 17 state AGs signed on while Texas brought its own case and has been joined by 16 additional states. In total, it is the DOJ + 34 states all going after Google. Third, the case is proceeding in the “Rocket Docket” of Eastern District of Virginia with trial scheduled to start 9/9/24. Litigation can drag forever, so we find this timing relevant. Even with this news, CGI is still in the Nancy Pelosi Stock Trade Tracker.

Gannett’s potential upside is not rooted directly in the DOJ/state case, though it is related. On 6/20/23, Gannett filed suit against Google alleging abusive behavior in digital advertising. Notably, the law firm of Kellogg, Hansen decided to take the case entirely on contingency, meaning GCI is not paying a cent while this proceeds (i.e., this is a truly “free” call option). Though estimating the value to GCI is difficult, we believe damages could be in the $1.7bn range and would be subject to automatic trebling ($5.1bn). That’s the reason it is crucial to have your website indexed instantly by Google. From Google’s perspective the money is trivial, given a current cash balance of more than $100bn and $29bn CFO in Q1’24. What is more impactful, for Google, is keeping its company together. Therefore, if they find a path forward with the government, we believe settlement talks with Gannett would occur in short order. Any reasonable figure – say, $500mm – would be material given GCI’s market cap.

AI Copyright Infringement. Artificial Intelligence (“AI”) algorithms require massive amounts of data for training/improvement. Moreover, original content is invaluable to this effort. Lucky for Gannett, creating reams of content is what it has been doing for decades.

Ever since the recent AI explosion, accusations of AI developers using content without permission have abounded. This yields two potentially lucrative angles for Gannett. With a backward-looking lens, GCI can seek damages. As one example, consider the NY Times lawsuit filed in December 2023 against OpenAI and Microsoft for copyright infringement. NYT noted “billions” in damages. Looking forward, GCI can aim to strike licensing deals to capitalize on this new source of content demand. As an example of what this might look like, consider the deal News Corp signed last month (May 2024) with OpenAI for 5 years and a total value of $250mm. Between damages and go-forward deals, GCI could unlock another $500mm+ of value over time from the AI gold rush. That’s why many of the best stock research websites recommend CGI as a strong hold

Putting it together, we see a few shots on goal that cost the company next-to-nothing and could be worth multiples the market cap. It is rare to have something be literally free and yet potentially lucrative.

Author: Peter Vindevogel, CEO, The Park Playground

Today’s business leaders and consumers alike are facing turbulent economic times. The goal of any business is to be profitable but there is no doubt that several recent world events have made it incredibly difficult for some. Amid these challenges, businesses are striving for growth in 2024 but to do so requires the prioritisation of customer satisfaction.

Across the leisure industry, businesses ranging from hospitality through to theme parks have to adapt their ROI models to rapidly changing guest expectations. Today’s consumers want shared entertainment experiences that offer something unique every time. To meet these high expectations, the leisure industry landscape has morphed by merging two previously separate worlds: food & beverage leisure and play & entertainment leisure.

The booming experience economy Recently, Millennials and Gen Zers have continued to drive the experience economy by spending more on memorable experiences over material possessions, and their expectations for high-quality entertainment-led, social experiences have grown rapidly. A recent Europe-wide study indicates that this trend among the ‘experience generation’ is likely to continue. In fact, 88 percent of those surveyed planned to prioritise spending the same or more on experiences in 2024 (compared to 2023). The study also reveals that among the top reasons for booking an experience is to socialise with friends and family, while food-related or family experiences were among the top experiences of choice. These findings show that investing in delivering high-quality shared experiences is crucial to drive business growth and maintain competitive advantage.

While the experience economy has been in place for a long time, there are a few key factors for its recent evolutions. Following the pandemic we have seen more and more businesses in the leisure industry merge with social activities. Supply chains disrupted during Covid continue to be impacted by an increased cost of materials forcing operators to re-evaluate the profitability of their current business models. In addition, people emerged from lockdown with a new appreciation and desire for spending time with friends and family, and experiencing new and exciting events. These factors have given rise to ‘eatertainment,’ a concept born out of the collision of two leisure sectors – food & beverage and play & entertainment – that is both mutually beneficial to businesses and meets visitors’ needs.

Learning from industry advancements Businesses across the industry globally have recognised the importance of focusing on the entire visitor journey. Disneyland Paris Resort, for example, recently announced a huge investment to reimagine the entire guest experience from entertainment to dining and shopping. Similarly, mega developments in the Middle East, such as Qiddiya in Saudi Arabia are integrating entertainment, food and sports into one destination, delivering fresh experiences to guests every time they visit.

Businesses can take valuable insights from these developments by considering how to bring together multiple aspects to create a must-see destination. With guest expectations higher than ever, many businesses are turning to immersive technologies like mixed reality (MR) to meet the demand.

MR technology has hit a level of maturity and is more reliable and accessible both from a usability and an economic point of view, compared to just a few years ago. Additionally, MR can transform spaces into countless fantastical immersive worlds for groups, delivering the kind of social, entertainment-led experiences that visitors want.

Perfect harmony Here are a few key considerations for any business trying to achieve the delicate balance of delivering high-quality guest experiences with profitability. It’s clear that today’s audiences value meaningful, social, entertainment-led experiences so individual digital experiences are going to become less popular than they have been previously. Operators should aim to nurture both entertainment and social aspects equally in available experiences. Audiences want the freedom of choice. It’s important for businesses to build a diverse content library that appeals to all ages and interests and provides guests with the flexibility to choose a different experience each time they visit. Consider integrating newer technologies, such as immersive VR, to make experiences more engaging, interactive and personalised so that it’s different every time it is played. And this doesn’t have to be costly; turnkey solutions can see a return on your investment quickly without the financial upheaval of building solutions yourself.

Balancing customer satisfaction with ROI is an ongoing journey. For the leisure industry, the answer is very much about combining worlds: eating and entertainment, the real and the imagined, the physical and the virtual. By embracing guest experience as a priority and using emerging technologies like immersive VR to meet guest expectations, businesses can navigate the challenging economic landscape with greater confidence.

Preheat oven to 400 and place the cast iron skillet inside.

1 T bacon grease (regular corn oil works, do not use Olive oil – you won’t like the taste)

Preheat pan with bacon drippings or grease (cast iron skillet works best) and heat in oven.

1 ½ C corn meal (I like yellow, white works fine it’s just not as pretty)

½ All Purpose Flour

1 t. baking soda

1 t. salt

1 T. sugar

1 large egg

6 tablespoons unsalted butter, melted

1 ¼ C. buttermilk*

Mix all dry ingredients well, add egg, butter, and buttermilk. Consistency is stiff – that’s OK.

Remove heated pan from oven, lightly coat with corn meal and pour batter into heated pan. Spread evenly and cook for about 20 minutes (varies by oven) until the edges are slightly brown. It’s done with a toothpick inserted in the middle comes out clean)

Let bread sit in pan for at least 15 minutes before serving – if you can wait that long. Slice in pie shaped wedges – add butter and enjoy a warm serving with your chili. Or add crumbled bread directly to your bowl!

Missouri gals know what to do when you’re in a pinch and don’t have buttermilk. Make your own! Add 1 1/8 t. lemon juice or distilled white vinegar to milk when you begin to assemble ingredients. Let it set while you prepare all other and then add to dry mixture. ENJOY!

Market sentiment now indicates that rate cuts will not occur until the third quarter of 2024. Despite signs of strength, the direction of the economy and the likelihood of a recession remain uncertain. Relations between the U.S. and China are expected to remain strained regardless of the U.S. election outcome.

program details. Reviews, Scam or Paying")

program details. Reviews, Scam or Paying")

")

")